The U.S. Department of Energy (DOE), the U.S. Department of Treasury, and the Internal Revenue Service (IRS) has announced $4bn in tax credits for over 100 projects across 35 states, which will accelerate a domestic clean energy supply chain and reduce greenhouse gas emissions at industrial facilities.

Clean energy projects selected for tax credits under the Qualifying Advanced Energy Project Tax Credit (48C), funded by President Biden’s Inflation Reduction Act, include large, medium, and small businesses and state and local governments.

All projects must meet prevailing wage and apprenticeship requirements to receive a 30% investment tax credit.

Investments in traditional energy communities will power a clean energy supply chain

Of the $4bn tax credits, $1.5bn supports projects in historic energy communities.

These projects will create good-paying jobs, lower energy costs, and support the climate, clean energy supply chain, and energy security goals of the Biden-Harris Administration’s Investing in America agenda.

“From direct grants to historic tax credits, the President’s Investing in America agenda is making the nation an irresistible place to invest in clean energy manufacturing,” said US Secretary of Energy Jennifer Granholm.

“The President’s agenda places direct emphasis on communities that have traditionally powered our nation for generations, helping ensure those communities reap the economic benefits of the clean energy transition and continue to play a leading role in building up the next wave of energy sources.”

DOE is partnering with the Treasury and the IRS to implement the Qualifying Advanced Energy Project Tax Credit (48C), which is funded by the President’s Inflation Reduction Act.

Established by the American Recovery and Reinvestment Act of 2009, the 48C Program was expanded with a $10bn investment under the Inflation Reduction Act of 2022.

At least $4bn of the total $10bn will be allocated for projects in designated 48C energy communities – communities with closed coal mines or coal plants.

48C Round 1 allocations and application overview

The DOE received approximately 250 full applications from projects requesting a total of $13.5bn in tax credits for the clean energy supply chain.

The size and scope of projects varied greatly, with applicants requesting tax credits ranging from under $1m to over $100m. They included:

Clean energy manufacturing and recycling: Selected from applications requesting support for the buildout of US manufacturing capabilities critical for clean energy deployment and span clean hydrogen, grid, electric vehicles, and nuclear power

Critical materials recycling, processing, and refining: Selected projects are investing in multiple electrical steel applications, lithium-ion battery recycling, and rare earth projects, all critical areas for maintaining a secure, reliable energy system and advancing the clean energy transition

Industrial decarbonisation: Selected projects would implement decarbnorthation measures across diverse sectors, including chemicals, food and beverage, pulp and paper, biofuels, glass, ceramics, iron and steel, automotive manufacturing, and building materials. Low-carbon fuels, feedstocks, and energy sources are well-represented as a solution for decarbonisation across these projects

The 48C programme will help to catalyse the nation’s equitable transition to a clean, secure, affordable, and resilient energy supply chain, reduce industrial greenhouse gas emissions, and create high-quality jobs across the country.

For selected projects to receive the tax credit, information will need to be submitted to the 48C portal within two years to certify the project. Within an additional two years following project certification, the project must be placed in service.

The Environmental Protection Agency (EPA) has officially announced the final vehicle emission standards for the US, which will cut over seven billion tonnes of carbon emissions.

The new vehicle emission standards are for passenger cars, light-duty trucks, and medium-duty vehicles for model years 2027-2032 and beyond.

These standards, aimed at curbing carbon emissions, are projected to significantly impact society, with nearly $100bn in annual net benefits, including substantial public health benefits and reduced fuel costs for drivers.

The EPA’s final standards build upon the significant pollution reduction goals outlined in the proposed rule while accelerating the adoption of cleaner vehicle technologies.

This move comes as sales of clean vehicles, including plug-in hybrids and fully electric vehicles, reached record highs in the previous year.

EPA Administrator Michael Regan and President Biden’s National Climate Advisor Ali Zaidi will announce these standards at an event in Washington, emphasising their alignment with President Biden’s climate and economic agenda.

Regan highlighted the significance of the new vehicle emission standards: “With transportation as the largest source of US climate emissions, these strongest-ever pollution standards for cars solidify America’s leadership in building a clean transportation future and creating good-paying American jobs, all while advancing President Biden’s historic climate agenda.

“The standards will slash over seven billion tonnes of climate pollution, improve air quality in overburdened communities, and give drivers more clean vehicle choices while saving them money.

“Under President Biden’s leadership, this Administration is pairing strong standards with historic investments to revitalise domestic manufacturing, strengthen domestic supply chains and create good-paying jobs.”

These standards maintain a technology-neutral and performance-based approach, leveraging advancements in clean car technologies to further reduce climate pollution and emissions contributing to smog and soot formation.

Environmental and health implications

The final standards are anticipated to generate substantial societal benefits, with annual net benefits estimated at $99bn.

They are projected to prevent over 7.2 billion tons of CO2 emissions through 2055, a figure equivalent to four times the emissions of the entire transportation sector in 2021.

Additionally, these standards will reduce fine particulate matter and ozone, potentially preventing up to 2,500 premature deaths in 2055, as well as reducing various respiratory and cardiovascular illnesses.

Manufacturers will have flexibility in meeting the performance-based standards through a mix of technologies, ranging from advanced gasoline vehicles to hybrids and full-battery electric vehicles.

The EPA’s analysis considers various available emission control technologies, ensuring consumers will continue to have diverse vehicle choices.

Compared to existing standards, the finalised standards for model year 2032 represent significant reductions in greenhouse gas emissions for both light-duty and medium-duty vehicles, contributing to improved air quality nationwide.

Impact on employment and industry growth

The EPA projects an increase in US auto manufacturing employment in response to these final vehicle emission standards.

Since President Biden’s inauguration, over $160bn in investments in US clean vehicle manufacturing have been announced, with the auto manufacturing sector adding over 100,000 jobs.

A statement from United Automobile Workers said: “The EPA has made significant progress on its final greenhouse gas emissions rule for light-duty vehicles.

“By taking seriously the concerns of workers and communities, the EPA has come a long way to create a more feasible emissions rule that protects workers building ICE vehicles while providing a path forward for automakers to implement the full range of automotive technologies to reduce emissions.”

Benefits for consumers and industry

These vehicle emission standards are expected to provide greater certainty for the auto industry, stimulating private investment, creating well-compensated union jobs, and fortifying the US auto sector.

Moreover, once fully implemented, the standards are estimated to save the average American driver approximately $6,000 in reduced fuel and maintenance costs over a vehicle’s lifespan.

The vehicle emission standards mark a pivotal step towards addressing climate change, promoting economic growth, and enhancing public health.

By fostering innovation in the auto industry and prioritising cleaner vehicle technologies, these standards are poised to yield substantial benefits for both society and the environment.

Mink Ventures Corporation (TSXV:MINK) is a Canadian mineral exploration company exploring for critical minerals (nickel, copper, cobalt) at its Warren and Montcalm projects, in the Timmins Nickel District, Ontario, Canada.

The assets are strategically located, highly prospective, polymetallic, Canadian critical minerals projects, ideally situated in a top-ranked mining jurisdiction with low geopolitical risk.

Mink’s portfolio offers significant opportunities for the discovery of critical minerals. The company’s capital structure, with only 18.8 million shares outstanding, enhances its shareholders’ potential to ride the Lasonde curve.

Location and advantages of Mink’s projects

Mink’s Montcalm Project covers 40 km2 and is adjacent to Glencore’s former Montcalm Mine. The former mine had a historical production of 3.93 million tonnes of ore grading 1.25% Ni, 0.67% Cu, and 0.051% Co (Ontario Geological Survey, Atkinson, 2010). Mink’s Warren Project is located just 35 km away.

These projects sit on the western edge of the Porcupine Camp and approximately 50km southwest of Canada Nickel’s Crawford project, which has recently attracted significant investment and attention from mining companies and battery manufacturers seeking an opportunity and a secure Canadian supply of these critical minerals.

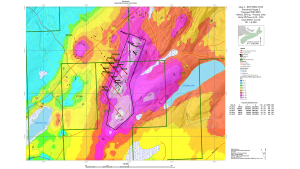

Fig.1: Mink’s property location map

Access and infrastructure to Mink’s projects, the adjacent Montcalm Mine, the Timmins Mining Camp, and milling facilities are exceptional. The proximity to infrastructure provides for extremely cost-effective exploration, with the availability of drills, crews, skilled labour force, equipment, and lower mobilisation costs.

All in diamond drill costs are in the range of approximately CAD$230 dollars per metre. This is extremely reasonable compared with drill programmes conducted outside of established mining areas.

Further, there is plentiful green, hydropower and all-weather road access to the projects.

Work on the Warren Project

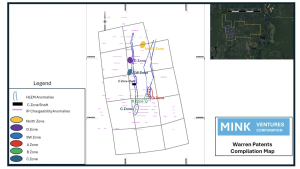

Mink is currently working on its recently acquired Warren Nickel Copper Cobalt Project. The Warren property covers 1,010 hectares of land and is located in Whitesides Township, approximately 35km west of Timmins (Fig. 1).

The Warren patented mining claims have a sporadic exploration history from the late 1920s to the present day, and yet a number of promising historical mineralised Cu Ni zones were outlined. That said, the majority of the exploration completed to date was conducted in a very minimal area of the property and completed over 60 years ago, as the patents were locked up and remained relatively untouched since.

More recent geophysical surveys from the early 1990s and 2008-2009 outlined a series of untested targets along strike from known mineralisation and/or new targets proximal to known mineralisation.

With the favourable geology, more recent geophysics, and extensive surface mineralisation, there is a significant opportunity for new Canadian critical mineral discoveries on the patents and across the expanded Warren project, which now includes additional staked claims (Warren East) and acquired claims (Warren North).

Mink’s work commitment to earn a 100% interest in the patented claims is $300,000. The company made a significant dent in that obligation with its recently completed $150,000 drill programme, half of which was funded by non-dilutive capital received through an Ontario OJEP exploration grant.

Though significant historical work exists on both the A and B zones, the bulk of the exploration efforts were limited to fairly shallow drilling and/or surface work, and the strike extents remain virtually untested. Consequently, there is a limited understanding of the geometry of these mineralised zones at depth.

Initial drill programme

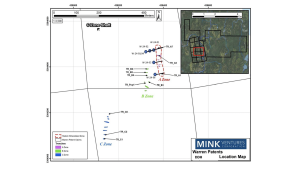

The ‘A’ Zone (Fig. 2,3,4) was the focus of Mink’s initial drill programme. It was selected as a high-priority target for drill testing as a result of a geological data review, a field examination, and a confirmation sampling programme during the summer of 2023. The ‘A’ Zone is exposed in historical trenches over a strike length of 120 metres.

Fig. 3: Warren trench and drill hole location map

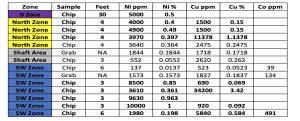

Mink’s grab samples on the ‘A’ Zone returned assay values ranging from 1.075% to 2.08% Cu. Nickel values ranged from 0.313% to 0.348% Ni. Cobalt values ranged from 0.0389% to 0.0498% Co and silver values of interest ranged from 10.3 ppm to 23.8 ppm Ag. (See press releases: February 5, 2024, September 20, 2023).

The drill programme consisted of a series of short holes on the A Zone to determine the extent of the mineralisation down plunge, down dip and along strike prior to evaluating the other mineralised zones and numerous untested priority geophysical targets on the property.

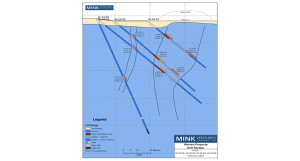

Fig. 4: ‘A’ Zone drill section: Drill holes W-24-01, W-24-02, W-24-03 and W-24-04

The programme consisted of six drill holes (507 metres) in the A Zone. Drilling confirmed the geophysical data and intersected broad zones of sulphide mineralisation in all six holes with anomalous nickel, copper and cobalt values associated with disseminated and net textured sulphides.

Drill hole W-24-01 was drilled to a depth of 60 metres and intersected 0.48% Nickel (Ni), 0.12% Copper (Cu), and 0.07% Cobalt (Co) over 0.9 metres in semi-massive sulphides typical of those found in the ‘A’ Zone surface trenches.

Drill core from W24-01 0.48%Ni over 0.9m in semi massive to massive sulphides

Assisting future drill programmes

Further, in several holes, Mink fortuitously clipped a sulphide zone in the upper portion of the holes which is interpreted to be the extension of the ‘B’ Zone. This valuable information provided some detail of how the A&B zones sit relative to one another which will assist in future drill programmes.

‘B’ Zone mineralisation is now known to extend approximately 75 metres beyond the historical trenches, for a total interpreted strike length of 200 metres. The ‘B’ Zone intercepts support the continuity of mineralisation along strike in general, as interpreted by geophysical surveys.

The geophysical signature for both the ‘A’ and ‘B’ Zones have a projected strike length of approximately 700 metres. Minimal drilling has been conducted on the ‘B’ Zone.

Two historical bulk samples on the ‘B’ Zone returned 0.21% Cu, 0.96% Ni, 0.11% Co and 0.10% Zinc (Zn), and a second bulk sample returned 2.83% Cu, 0.58% Ni, 0.10 Co and 0.13 Zn. Reference: Technical Report for Western Troy Capital Resources on the Warren Property (W. Hawkins P. Eng, 2021).

Surface sampling on the ‘A’ Zone and the recent drill programme have shown that the best values to date are associated with massive to semi-massive sulphides.

The current interpretation is that the initial ‘A’ Zone massive sulphide may have formed as a typical sulphide lens and then been broken apart by a later pulse of gabbro. This is based on a number of features seen in the drill core, the extent of massive and semi-massive sulphides, and Ni Cu Co values seen in the ‘A’ Zone trenches.

Further drilling is required to ascertain the extent of potential massive sulphide zones down the plunge and along the strike, as the ‘A’ Zone has only been tested by very shallow drilling (65 metres vertical) over a short strike length. The ‘A’ Zone geophysics suggests a strike length of approximately 700 metres.

Select historical sample data – see Fig. 2 compilation map Reference: Ontario Resident Geologists Office Timmins Ontario; Maxmin, Magnetometer and VLF Surveys Evaluation Report, Whitesides and Massey Twp. Claims (C Mackenzie Consulting Geologist, 1990)

Evaluating high-priority zones

The Warren project contains numerous historical, trenched surface zones, with significant Cu and Ni values which are associated with coincident geophysical responses including magnetics, electromagnetic (EM) and induced polarisation (IP) anomalies over long strike lengths. The majority of these occurrences have had little or no drilling.

At this time, it is thought that the ‘Shaft Area’, along with the ‘D’ Zone, and ‘SW’ Zone are extensions of the ‘C’ Zone. This system has had very minimal exploration along a strike length of approximately 1.5 km from geophysical data.

Mink plans to evaluate a number of these high-priority zones in order to outline a follow-up drill programme. The initial prospecting work will be conducted in the early spring/summer in order to prioritise targets for future drill testing in 2024.

The project has only gotten more compelling with the results of this programme. Given the extent of surface mineralisation on the property over seven historical mineralised zones, with significant untested strike lengths, the data is captivating and more drilling is warranted. The team looks forward to reporting its progress as the geological puzzle unfolds.

Warren property geology

The Warren property, one of Mink’s Canadian critical minerals projects, is hosted within the Kamiskotia Gabbro Complex (KGC) and is thought to be broadly equivalent to the Montcalm Gabbro Complex (MGC) but separated by a granitic arch.

The MGC hosts the former Montcalm Mine, which produced approximately 3.93 million tonnes grading 1.25% Ni, 0.67% Cu and 0.05% Co (OGS, Atkinson, B, 2010).

According to an estimate in the Ontario Mineral Inventory Record MD 142B09NE00007, dated January 2009, the mine hosted Mineral Reserves of 2,800,000 tonnes grading 1.26% Ni, 0.59 Cu, and 0.05% Co. *The reserve calculation is historical in nature and is not NI43-101 compliant; it is not to be relied upon and is reported as a historical statement only.

Gabbro complexes such as MGC and KGC are known to be prospective for magmatic nickel copper sulphide deposition, as demonstrated by the Montcalm Mine located within the MGC. The Warren property complements Mink’s Montcalm property due to the distinctly similar prospective geological environments found in the MGC and the KGC, as well as the presence of significant Cu Ni zones on the Warren Property.

Adhering to ESG measures

Environment

Mink complies with all environmental and permitting requirements of the province. The mineralised zones at Warren are present on patented mining claims which means that the company controls the surface rights and mineral rights. Early-stage exploration efforts such as diamond drilling do not require permitting when working on patented claims.

However, the same standard of care with respect to the environment is taken on Mink’s patented claims, and all activities conducted adhere to or supersede the permit guidelines.

Social

Mink is led by a female CEO, and the company has nearly equal representation. Additionally, the company is operating in a part of Northern Ontario, where there is a clear and articulate process to build solid relationships and work side by side with local communities and First Nations.

Governance

The company operates with high standards and conduct and has excellent governance due to the experienced directors and officers with track records of success in the industry.

The U.S. Department of Energy (DOE) has unveiled a strategic initiative aimed at bolstering the nation’s electrical grid with clean energy solutions.

With an investment of $34m across eleven selected projects, the DOE is paving the way for a more resilient and sustainable US electrical grid powered by wind and solar energy.

Additionally, the DOE has announced a $10m funding opportunity to streamline the interconnection process for clean energy, further propelling the nation towards the ambitious target of achieving 100% clean electricity by 2035.

Advancing electrical grid reliability with clean energy

However, as the US electrical grid incorporates larger amounts of variable renewable energy, such as solar and wind, novel tools are essential to manage their intermittency effectively.

Rising temperatures exacerbated by climate change, alongside the retirement of conventional power plants and the surge in demand from various sectors, pose significant challenges to power grid reliability.

By optimizing the integration of renewable technologies, these projects will enhance US electrical grid flexibility and resilience, mitigating the impacts of weather events and demand fluctuations.

The 11 selected projects include:

Florida International University: $2.4m

Washington State University: $2.4m

Georgia Institute of Technology: $2.8m

Iowa State University: $3m

Midcontinent Independent System Operator: $3m

National Renewable Energy Laboratory: $6.5m

University of Connecticut: $3.3m

Arizona State University: $3m

Pacific Northwest National Laboratory: $3.6m

Quanta Technology: $3.8m

Streamlining interconnection processes

With hundreds of gigawatts of solar, wind, and energy storage capacity expected to come online in the near future, efficient interconnection processes are paramount.

Currently, over 2,000 gigawatts of capacity are awaiting transmission interconnection, highlighting the urgent need for streamlined procedures.

With a $10m investment, this initiative aims to enhance software tools that expedite interconnection studies for renewable energy projects.

By providing developers with crucial data on transmission system characteristics, such as stability and voltage, these tools will reduce wait times and uncertainty, facilitating the rapid deployment of clean energy projects.

The SWIFTR funding opportunity aligns with the Interconnection Innovation e-Xchange (i2X), launched in 2022 to simplify and accelerate clean energy interconnections.

Complementing the Federal Energy Regulatory Commission’s efforts to reform interconnection procedures, i2X focuses on enhancing US electrical grid reliability, resilience, and security.

In 2023, i2X introduced a draft roadmap outlining strategies to expedite the interconnection process, emphasising the importance of maintaining a reliable grid and increasing data access and transparency.

The latest funding opportunity represents a significant step towards realising these objectives, fostering a more efficient and robust electrical grid for the future.

US Secretary Jennifer Granholm commented: “We can’t deploy clean energy if we can’t get renewable sources connected to our grid.

“Thanks to support from the Biden-Harris Administration, we are developing new, state-of-the-art tools to break up logjams to connect more clean energy sources to the grid even faster, giving Americans access to more affordable and resilient sources of clean energy.”

As the US strives towards a cleaner and more sustainable energy landscape, investments in grid modernisation and clean energy technologies are critical.

The DOE’s latest initiatives signal a concerted effort to overcome challenges and accelerate the transition towards a renewable-powered future.

With an anticipated infusion of over $430bn in climate and clean energy programmes over the next decade, these legislations are designed to expedite the shift towards a decarbonised energy system.

Key stipulations encompass investments and tax credits specifically for zero-carbon electricity generation and storage, thereby stimulating the deployment of clean energy. This article assesses the potential impacts of the IRA and BIL on the US energy system, considering a myriad of policy implementations and market conditions.

A crucial aspect of this examination will also be an exploration of the role of advanced nuclear reactors in this energy transition, offering a glimpse into potential market opportunities. Undeniably, the outcomes of this analysis will offer crucial insights into the practicality, costs, and benefits of cultivating renewable resources, electricity transmission, and carbon dioxide infrastructure under these fresh policy frameworks.

Understanding the Inflation Reduction Act

Delving into the intricacies of the Inflation Reduction Act of 2022, it is crucial to note that this legislation, alongside the Bipartisan Infrastructure Law, represents a significant investment by the US Federal Government in modernising and decarbonising the nation’s energy system. These laws are designed to drive a massive shift in the energy industry, with far-reaching policy implications and economic effects.

The policy implications of the IRAS and BIL are substantial. They aim to accelerate the transition to a cleaner, more sustainable energy system, driving regulatory changes to reshape the industry. These changes include incentivising clean energy deployment and creating a favourable tax environment for zero-carbon-emitting electricity generation and storage.

The economic effects of these laws are expected to be profound. By incentivising investment in clean energy, they aim to stimulate economic growth, create jobs, and reduce dependence on fossil fuels. They also aim to reduce consumer costs, making clean energy more affordable and accessible.

From an industry perspective, the new laws present both challenges and opportunities. They necessitate a shift towards cleaner energy sources, requiring significant investment in new technologies and infrastructure. However, they also open up new market opportunities for companies that can innovate and adapt.

Stakeholder engagement is essential in implementing these laws effectively. It is necessary to work collaboratively with all stakeholders, including the energy industry, environmental groups, regulators, and the wider public, to ensure that the transition to a cleaner energy future is achieved in a way that benefits everyone. This requires open dialogue, mutual understanding, and a shared commitment to achieving climate goals.

Key provisions and incentives

After thoroughly understanding the Inflation Reduction Act and its broad policy implications, it is essential to highlight the key provisions and incentives embedded within these laws designed to stimulate clean energy deployment. A critical component of these laws is their use of tax credit benefits. These benefits serve as clean energy incentives, promoting zero-carbon electricity generation and storage technology investment.

Investment and production tax credits (ITC and PTC) offer significant financial advantages to industries incorporating clean energy technologies. These tax credits, coupled with CO2 capture and storage incentives, form a robust framework geared towards accelerating the transition to a low-carbon energy system. The incentives are not limited to large-scale utility providers. They also encourage smaller entities to invest in clean energy, promoting a widespread, grassroots transition to cleaner energy sources.

Another noteworthy aspect is the emphasis on innovation promotion. The legislation provides the fiscal stimulus required for research and development in clean energy technologies. This provision is pivotal in driving the technological advancements necessary to achieve a sustainable energy system.

Scenario analysis and assessments

To fully comprehend the potential impacts of the Inflation Reduction Act and the Bipartisan Infrastructure Law on the US energy system, it’s essential to examine two distinct scenarios: the no new policy scenario and the IRA-BIL scenario. These scenarios represent different policy enactments and their implications on market dynamics, technology assessment, regulatory challenges, and investment opportunities.

The no new policy scenario provides a baseline, assuming current policies continue without the introduction of the IRA or BIL. Conversely, the IRA-BIL scenario incorporates the policy changes proposed by both legislations.

Scenario

Policy Implications

Market Dynamics

No new policy

Reflects regulatory challenges of current policies

Depicts current market dynamics without IRA-BIL

IRA-BIL

Highlights new policy implications

Shows potential changes in market dynamics

Both scenarios consider future variables such as electricity market conditions, technology costs, natural gas prices, and renewable resource development. The IRA-BIL scenario, for example, assumes substantial investment opportunities in clean energy technologies driven by the policy incentives of the IRA and BIL.

US energy system impact evaluation

Evaluating the potential impacts of the Inflation Reduction Act and the Bipartisan Infrastructure Law on the US energy system reveals far-reaching implications across various sectors.

Primarily, these legislations could significantly improve grid resilience. By encouraging investments in modern infrastructure and advanced technologies, the potential for system failures and outages could be reduced. This is particularly crucial in an era where climate change poses increased threats to the stability of energy systems.

Secondly, these legislations promote renewable integration. The push for clean energy sources such as wind, solar, and hydroelectric power is key to a sustainable energy future. The laws facilitate this by creating favourable conditions for the deployment and integration of these resources into the existing grid.

Thirdly, the laws enable greater energy efficiency. By incentivising businesses and households to adopt energy-efficient practices and technologies, energy consumption can be reduced while maintaining or improving service levels.

Fourthly, carbon pricing mechanisms embedded within these laws send a clear signal to the market about the true cost of carbon emissions. This drives businesses to innovate and adopt cleaner technologies, fostering a culture of technology innovation.

Ultimately, the Inflation Reduction Act and the Bipartisan Infrastructure Law have the potential to reshape the US energy system profoundly. They could guide it towards a path of resilience, efficiency, and sustainability while driving the innovation necessary for a low-carbon future.

Emission reduction potential

Building on the potential effects of the Inflation Reduction Act and the Bipartisan Infrastructure Law on the US energy system, an important aspect to consider is their potential for emissions reduction. These legislations provide a framework for emission reduction strategies, advancing clean energy benefits and influencing sectoral impacts. They also facilitate renewable integration and establish decarbonisation pathways.

The table below presents an overview of key emission reduction strategies and their potential impacts:

Emission Reduction Strategies

Potential Impacts

Clean energy deployment

Accelerates the transition towards renewable sources, reducing reliance on fossil fuels

Energy efficiency measures

Reduces energy consumption, leading to lower emissions

Carbon capture and storage

Captures and stores CO2 emissions, aiding in climate change mitigation

Renewable integration

Enhances grid flexibility and stability, supporting a higher percentage of renewables

Decarbonisation of industrial sectors

Leads to emission reductions in high-emitting sectors like heavy industry and transportation

The clean energy benefits of these measures are manifold, encompassing both environmental and economic advantages. Sectoral impacts are anticipated across various industries, particularly in transportation and manufacturing, with the potential to transform these sectors towards low-carbon models.

Renewable integration into the US energy system is another crucial facet, promoting the diversification of energy sources, boosting energy security, and contributing to emission reductions. Decarbonisation pathways, meanwhile, outline a strategic approach towards achieving a carbon-neutral future, enhancing sustainability, and mitigating the adverse effects of climate change.

Advanced nuclear reactor opportunities

In light of the recent legislative measures, substantial opportunities are emerging for the development and deployment of advanced nuclear reactors in the US energy system. These modern reactors possess unique features such as enhanced safety measures, improved efficiency, and reduced waste, making them suitable for various industrial applications.

Market integration of these advanced reactors could contribute significantly to the diversification of energy sources, thereby enhancing energy security. This integration would involve the electricity market and other sectors, such as manufacturing and transportation, which could benefit from nuclear energy’s reliability and low-carbon emissions.

Industry partnerships are essential for the successful deployment of advanced reactors. Collaboration between nuclear technology providers, energy users, and regulatory bodies would ensure the alignment of interests and accelerate the adoption of these innovative technologies. These partnerships could also foster an environment conducive to sharing knowledge and expertise, further driving the development of advanced reactors.

The economic benefits of advanced nuclear reactors are manifold. They range from job creation in the nuclear sector to cost savings from the use of low-carbon energy. Moreover, the export of advanced reactor technologies could generate significant revenue and enhance the US competitiveness in the global nuclear market.

Lastly, the deployment of advanced nuclear reactors presents numerous innovation opportunities. These include the development of next-generation nuclear technologies, the enhancement of existing nuclear infrastructure, and the exploration of novel applications of nuclear energy. Together, these opportunities can contribute to the sustainability and resilience of the US energy system.

Financing clean energy technologies

Securing adequate and sustainable funding is critical in successfully deploying and scaling clean energy technologies. Renewable financing and clean tech investment are two crucial elements of this financial infrastructure. They provide the capital necessary for research, development, and implementation of innovative solutions that can help transition our energy systems from fossil fuels to cleaner, more sustainable sources.

To maximise the impact of sustainable finance, it is important to adopt strategic energy funding strategies. This could include leveraging public funds to attract private investment, implementing clean energy incentives, and developing financing models that are accessible and appealing to a wide range of investors. One example is green energy financing, where investments are made in projects that deliver environmental benefits alongside a financial return.

Furthermore, the Inflation Reduction Act is expected to play a key role in shaping the landscape of clean energy financing in the US. Its provisions for tax credits and incentives for clean energy technologies represent significant steps towards a more sustainable and resilient energy system. By providing a favourable environment for clean technology investment, it is hoped that this legislation can stimulate the growth and development of renewable energy technologies.

The US Inflation Reduction Act (IRA) has been a significant catalyst in the economic landscape, particularly within the solar photovoltaic (PV) manufacturing industry.

This article will explore the beneficial impact of the IRA on this green technology sector, considering the financial implications, the stimulation of technological advancement, and the prospects under the current legislation.

We will unravel the intricacies of this relationship, setting a foundation for a comprehensive understanding of the future trajectory of the solar PV manufacturing industry in the context of the IRA.

Understanding the Inflation Reduction Act

To fully grasp the impact of the Inflation Reduction Act on solar PV manufacturing, a comprehensive understanding of this legislation is necessary.

The act’s interpretation is rooted in the law’s intent to curb inflation by manipulating economic strategies and regulating financial practices, which brings a focus to its economic implications.

At its core, the IRA aims to stabilise pricing and enhance the dollar’s purchasing power, inadvertently promoting the affordability of renewable energy technologies like solar PV manufacturing.

The legal provisions of the act are its foundational pillars, governing its implementation and enforcement. They outline the responsibilities of key stakeholders, the rights of affected industries, and the penalties for non-compliance.

For the solar PV manufacturing sector, the act’s provisions could potentially reduce production costs and foster competitiveness.

However, like any significant policy shift, the act also brings Implementation Challenges. These can include industries needing to adapt to new economic conditions or potential resistance from sectors negatively affected by the act.

The solar PV manufacturing industry may need to invest in operational adjustments to fully exploit the benefits of the act.

IRA’s impact on solar PV manufacturing

Drawing upon the legal provisions and economic implications of the IRA, we can explore its tangible effects on the solar PV manufacturing sector.

The act, through its policy implementation, has instigated several changes in this sector, notably in job creation, trade relations, environmental impact, and market competition.

The IRA has been instrumental in job creation within the solar PV manufacturing industry. It has stimulated this growth by providing tax incentives for manufacturing companies to enhance their workforce. This policy implementation has bolstered the industry and helped reduce unemployment rates.

Trade relations have also been impacted by the IRA. The act has fostered a more favourable trading environment for solar PV manufacturers by reducing inflationary pressures on imported raw materials. This has enhanced the competitiveness of US manufacturers in the global market, improving the country’s trade balance in the process.

Regarding environmental impact, the IRA has indirectly boosted the use of renewable energy sources. By making solar PV manufacturing more economically viable, the act has encouraged the production and use of solar panels, thereby reducing greenhouse gas emissions.

Lastly, the act has spurred market competition. The reduced inflation rates have made it more cost-effective for new businesses to enter the solar PV manufacturing sector. This has increased the number of manufacturers, promoting a more competitive market and a wider range of options for consumers.

Delving into the financial benefits of the Inflation Reduction Act, we observe a significant enhancement in the economic viability of the solar PV manufacturing sector. The IRA offers multiple rewards that collectively contribute to the growth and prosperity of this industry.

One of the most compelling benefits is the provision of tax incentives. These incentives lower the tax burden for solar PV manufacturers, freeing up capital that can be reinvested in the business.

This leads to investment growth, another key benefit of the IRA. Increased investment enables manufacturers to expand their operations, purchase new equipment, and hire more employees, fostering business expansion.

In addition to tax incentives and investment growth, the IRA promotes cost efficiency. By reducing the inflation rate, the act increases the purchasing power of manufacturers. This allows them to acquire raw materials and other necessities at lower costs, thereby improving the bottom line and encouraging economic stability.

Moreover, economic stability is further enhanced as the IRA helps to stabilise the value of the dollar. This is crucial for solar PV manufacturers, who often deal in international markets. A stable dollar value reduces the risk of currency fluctuations, providing a more predictable business environment.

IRA and technological advancements

Building on the economic implications, the Inflation Reduction Act also catalyses technological advancements in the solar PV manufacturing industry.

By providing financial incentives, the IRA stimulates technological investments, leading to accelerated innovation in solar PV technology. These investments are crucial for research and development, enabling companies to explore new, efficient methods of solar PV production.

The IRA implications on technological advancements are significant. The policy’s effectiveness in encouraging investments has been reflected in increased technological breakthroughs, improved production processes, and enhanced solar panel efficiency.

These advancements not only strengthen the industry’s competitive edge but also contribute to environmental sustainability by promoting cleaner energy sources.

However, advancement challenges persist. The rapidly evolving nature of technology necessitates continuous investment and innovation. Despite the financial benefits provided by the IRA, the high costs associated with advanced technology development and implementation can pose a hurdle.

Therefore, while the IRA has been instrumental in fostering growth and innovation, addressing these challenges requires strategic planning and sustained commitment.

Moreover, the effectiveness of the IRA in driving technological advancements is contingent on a supportive regulatory environment. Policymakers must ensure that the IRA’s provisions align with the industry’s evolving needs, encouraging continued investment and innovation.

A dynamic policy framework can help maintain the momentum of technological progress, ensuring the solar PV manufacturing industry’s long-term competitiveness and sustainability.

Future solar energy prospects under the IRA

Looking ahead, the Inflation Reduction Act holds promising potential for the future growth and development of the solar PV manufacturing industry.

It is expected to usher in advancements in various dimensions, including job creation, market expansion, environmental impact, global competition, and sustainable development.

The IRA could stimulate job creation by allocating funds for research, development, and manufacturing processes in the solar PV industry. This would not only increase employment but also enhance the skills of the workforce in this thriving sector.

Market expansion is another potential benefit of the IRA. With reduced inflation, the purchasing power of consumers is likely to increase, leading to heightened demand for solar PV products. This would pave the way for the expansion of the solar PV market.

The table below encapsulates the future prospects under the IRA for the solar PV manufacturing industry:

Prospects

Current Scenario

Expected Improvement

Job Creation

Limited job opportunities

Increase in employment and skill enhancement

Market Expansion

Restricted market growth

Increase in demand and market size

Environmental Impact

High carbon footprint

Reduction in greenhouse gas emissions

Global Competition

Moderate competitive edge

Increased global market share

Sustainable Development

Limited sustainability measures

Enhanced sustainability practices

The IRA could bring about positive environmental impacts by encouraging cleaner energy production, thus reducing greenhouse gas emissions.

Additionally, it could enhance global competition by providing the US solar PV industry with a competitive edge.

Lastly, the IRA could foster sustainable development by promoting environmentally friendly and sustainable practices in the industry. These prospects under the IRA paint a bright future for the solar PV manufacturing industry.

The Inflation Reduction Act of 2022, landmark legislation on climate change, has undoubtedly set the United States on a transformative path towards clean energy leadership.

However, the Act’s potential influence extends beyond US borders, touching global clean energy supply chains and raising critical questions about international trade dynamics and national security.

How are clean energy supply chains reflected in the Inflation Reduction Act?

The Inflation Reduction Act is a monumental piece of legislation characterised by diverse provisions designed to invigorate the clean energy sector and reduce greenhouse gas emissions, therefore reshaping the American energy landscape.

This legislation has significant implications for the United States, the global energy sector, and our collective efforts to achieve environmental sustainability.

Impact analysis of the Act reveals a forward-thinking approach towards creating economic benefits. These are expected to be realised through increased investment in the clean energy sector and the creation of new jobs.

The Act also aims to strengthen the resilience of energy supply chains by diversifying sources and reducing dependence on foreign oil.

It also recognises the importance of global partnerships. It seeks to inspire international cooperation in the fight against climate change while gaining a competitive edge in the global clean energy market. The legislation promotes the sharing of technological advancements and collaborative efforts in research and development, thus fostering an international community committed to environmental sustainability.

However, perhaps the most crucial aspect of this legislation is its focus on supply chain resilience. The Act aims to create a more stable and reliable energy supply chain by encouraging domestic production and incentivising industries vital to US national security.

This focus on resilience serves the dual purpose of creating economic opportunities at home while reducing vulnerability to external supply shocks and geopolitical instability.

Policy recommendations for energy resources

Building on the implications of the Inflation Reduction Act for clean energy supply chains, a set of strategic policy recommendations emerges to bolster further the Bureau of Energy Resources’ efforts to foster a resilient and sustainable energy landscape.

These recommendations focus on international partnerships, resource sustainability, private investment, diplomatic engagement, and the importance of critical minerals.

Firstly, strengthening international partnerships is crucial in promoting resource sustainability. This can be achieved through multilateral agreements on clean energy technology and the development of ethical sourcing for critical minerals. It is recommended that the US expand the Mineral Security Partnership (MSP) to include more nations committed to MSP principles and create a ‘Battery Passport’ to facilitate the trade of ethically sourced battery components among member states.

Private investment is also critical in transitioning to a clean energy future. The US government can support private firms and entrepreneurs by forming diplomatic and expert task forces to secure deals with emerging economies vital to clean energy supply chains.

Moreover, diplomatic engagement can ensure international cooperation. Encouraging Free Trade Agreements, including bilateral critical mineral agreements, with international partners can foster global collaboration.

Lastly, critical minerals are essential to clean energy technologies. The US should establish a Strategic Critical Mineral Stockpile among MSP member states to ensure a steady supply.

Evolution of the US manufacturing sector

Since the turn of the new millennium, significant changes have swept across the United States manufacturing sector, partially due to the rise of Chinese competitive pressures.

The sector has undergone an evolution analysis, rebalancing towards industries where the US holds a comparative advantage. Future trends, such as technological advancements and market competition, have driven this transformation.

While this shift has had a global impact, particularly on supply chains, it has also made the sector more resilient and competitive. With the help of the Inflation Reduction Act, the US manufacturing sector is now strategically positioned to lead the global transition towards clean energy.

Looking ahead, the manufacturing sector is expected to continue evolving in response to the potential offered by the clean energy transition.

The Inflation Reduction Act, coupled with technological advancements and market competition, has the potential to transform the US into a global leader in clean energy.

Critical investments in infrastructure and manufacturing

Under President Biden’s administration, significant legislative strides in infrastructure and manufacturing have been made, as evidenced by the Infrastructure Investment and Jobs Act (IIJA), the CHIPS and Science Act, and the Inflation Reduction Act.

These acts collectively represent an unprecedented commitment towards enhancing infrastructure, advancing manufacturing capabilities, and promoting clean energy transition. The impact analysis of these critical investments reveals a strategic plan to strengthen supply chain resilience, stimulate investment opportunities, and ensure regulatory compliance.

The IIJA, for instance, earmarks over $1tr for infrastructure improvement, focusing on traditional areas like roads and bridges while prioritising clean energy and digital infrastructure.

The CHIPS Act, on the other hand, targets domestic semiconductor production, an apparent move to fortify the technology supply chain.

The IRA, however, stands out as the most pertinent to our discussion on clean energy supply chains. This act directs substantial funding towards clean energy tax credits, air pollution regulation, and clean manufacturing tax credits, among other things. It underlines the administration’s commitment to a more sustainable, resilient, and domestically-centred clean energy supply chain.

This legislative push also encourages global partnerships. As US firms align their strategies with the provisions of these acts, we foresee an increase in international collaborations.

These partnerships will ensure supply chain resilience and open up new investment opportunities.

Environmental implications of the IRA

In assessing the environmental implications of the Inflation Reduction Act, it’s crucial to examine the legislation’s potential to reduce greenhouse gas emissions and promote sustainable energy practices.

The IRA is a significant step towards US commitments to climate resilience, with various strategies in place to ensure sustainable practices in clean energy development.

An impact assessment of the IRA suggests promising outcomes. The Act seeks to mobilise government agencies and the private sector to develop efficient, resilient, sustainable clean energy supply chains.

Climate models indicate that the IRA could help the US achieve up to 84% of its emissions reduction goal, a significant stride towards mitigating climate change.

Global partnerships are central to the IRA’s approach. The Act promotes reshaping supply chains to align with US geostrategic interests and encourages sourcing from partners based in allied countries. Diversifying can enhance supply shock resilience and encourage ethical sourcing in clean energy supply chains.

In essence, the IRA is a robust policy instrument designed to promote environmental sustainability, foster global partnerships, and achieve significant reductions in greenhouse gas emissions.

Strategic motivations behind the IRA

Building on the environmental implications of the Inflation Reduction Act, it is crucial to understand the critical strategic motivations that fuelled its creation and implementation.

The Act was a response to inflation pressures and a strategic initiative to ensure America’s economic competitiveness and energy security in a rapidly changing world.

Impact analysis of the IRA reveals an intent to reposition the US as a global leader in clean energy. The Act seeks to stimulate the domestic clean energy sector by offering tax incentives, investment initiatives, and sustainable development.

This approach aligns with the broader objective of enhancing energy security, reducing dependency on fossil fuels, and fostering resilience against global supply chain shocks.

A significant strategic motivation behind the IRA was creating and nurturing global partnerships. The Act encourages cooperation with international partners, seeking to forge alliances that strengthen clean energy supply chains. These partnerships aim to create a more diversified supply, increase resilience, and promote economic competitiveness.

Finally, the IRA promotes sustainable development, integrating economic growth with environmental stewardship. By incentivising clean energy, the Act contributes to the global effort to combat climate change while creating new opportunities for American businesses.

Future impact on global clean energy supply chains

The Act’s core purpose is to bolster the United States’ position in the clean energy industry, thereby reducing reliance on foreign energy sources and creating a more sustainable and resilient economy.

The Act’s overview reveals funding provisions totalling $370bn. This funding is dedicated to tax incentives and investment initiatives to increase supply and demand within the clean energy sector.

The implications of these provisions could potentially reshape the energy industry’s landscape, creating a more competitive and sustainable market.

An in-depth analysis of the Act’s provisions demonstrates an explicit emphasis on domestic clean energy production. This has garnered criticism from international partners, who view these provisions as a barrier to free trade.

However, these provisions’ benefits for the US economy cannot be understated, as they promote local industry and employment opportunities.

The impact of the Act’s provisions on the global clean energy supply chains is expected to be significant. By incentivising domestic production, the Act could disrupt existing supply chains, forcing companies to reevaluate their sourcing and manufacturing strategies.

This could lead to a greater diversification of clean energy sources, ultimately promoting sustainability and resilience in the face of potential supply shocks.

Devin Arthur, Director of Government Relations at the EV Society, discusses Canada’s rapid progress in the electric vehicle industry, highlighting the importance of addressing affordability, infrastructure, and supply chain development to accelerate adoption.

When we cast our minds back to five years ago, the Canadian, and even global, electric vehicle (EV) industry was still in its infancy. Within this time, we have seen the development of holistic battery electric vehicle (BEV) supply chain, complete with billion-dollar investments, additional mineral processing, battery cell manufacturing, and reskill initiatives to support these sectors.

Everyone wants to own a car to enjoy the freedom of mobility and access. Consequently, with demand for personal vehicles continuing to rise, attention must turn to ensuring EVs present a viable alternative to existing vehicles.

In Canada, around 30-35% of all emissions are from personal transportation. Eliminating these emissions will rapidly accelerate decarbonisation, explaining Canada’s focus on electric vehicles and target of 100% EV sales by 2035.

Yet, if EVs are to meet sustainable goals, the supply chain as a whole must become less wasteful. Action must be taken to establish a circular economy that maximises the use of resources and guarantees the continued ability to meet future demand.

Recently, the concept of a global battery passport, aiming to track the emissions produced across the battery supply chain, has been proposed. Introducing standards and regulations such as this will enable companies and the industry as a whole to be held accountable and ensure batteries are manufactured with low-impact and sustainable methods.

Barriers to EV adoption

This is not to say that EV adoption is not without issue. In North America, one of the largest barriers to adoption is affordability.

Many of the EV models currently on the market are large and, therefore, expensive, pricing them out of the average income range without financial incentives.

There is a balance to be struck with industry in providing these incentives or considering ways to increase supply volumes of more affordable options in order to bring prices down.

Improving EV infrastructure

As the adoption of EVs takes hold, the associated infrastructure must improve and, equally, expand. The major metropolitan areas are mostly equipped with some form of charging infrastructure, whether at home, curbside, or gas stations.

But with the increase in EV adoption, the next phase of expansion must provide rural infrastructure for those who want to drive longer distances. In Canada especially, there is a vast expanse of rural geography in the North with little other than highways.

Therefore, infrastructure must be expanded in those areas, and its reliability must be improved to increase consumers’ confidence that an EV can fulfil their needs.

Canada’s potential to establish a supply chain

The recent Bloomberg NEF report highlighting Canada as the most sought-after place to establish a supply chain illustrates the potential of dedicated attention. There is a nationwide understanding of what is required for the EV industry to succeed.

At every level, federal, provincial, and municipal governments have collaborated to provide companies with a robust supply chain, skilled workers, and an open line of communication.

Work of the EV Society

The EV Society is an integral part of this communication. Acting in both a consumer-facing capacity and participating in regulatory meetings, the society acts as an intermediary between industry, policymakers, and end-users, advocating for the uptake and improvement of EVs.

The society has recently worked with the federal government on an industry working group for the EV ecosystem. This aims to consider how Canada can meet that 2035 target and strive for equitable access, accounting for affordability, rural infrastructure, and complicated urban infrastructure (e.g., for those living in apartments or unable to charge at home).

Regular involvement in the consultations and regulatory meetings enables us to advocate on behalf of the consumer and communicate their concerns. Information is critical to increasing the adoption of EVs. The society fosters more informed decision-making by promoting the benefits and dispelling the myths surrounding electric vehicles through regular webinars.

It also provides a platform connecting potential buyers to existing EV drivers in the community, building connections and consumer confidence.

The EV Society in Sudbury is in a unique spot with an established mining industry that is over 100 years old. There is a huge level of mining knowledge and experience in the area, surrounded by extraction and processing. The local community consistently exceeds average EV adoption, recently passing 1,000 EVs on the road – a considerable achievement for a community of 185,000. Sudbury is a prime example of how engagement and awareness are critical for the uptake of EVs and is now making the connection that EV sales directly impact the local economy.

Canada and the rest of the world must continue to encourage and support the significant economic and environmental potential electric vehicles offer. Globally, if we are to meet green targets, we cannot afford to lose momentum in the adoption of EVs. The work must now be directed into logistics, infrastructure, and equal access. Governments, companies, and the general population alike must be assured that the future of transportation still lies in electricity.

Please note, this article will also appear in the seventeenth edition of our quarterly publication.

The Natural Resources Canada discusses the potential of Canada’s rare earths and the importance of responsible sourcing to meet increasing demand for clean energy technologies.

The demand for minerals and metals associated with the clean energy transition and the transition to zero-emission vehicles is expected to increase significantly over the next ten years. Fortunately, Canada possesses significant potential to increase the mining and processing of many of these critical minerals, which will drive economic growth in Canada, create jobs for Canadian workers, and reduce Canada and our allies’ vulnerability to supply risks.

In this context, Canada is utilising its potential to step up to develop secure and stable supply chains for the minerals and metals essential to reaching net zero and support likeminded partners in critical minerals security to insulate Canada and its allies from geopolitics and reliance on an anti-market economy or anti-democratic nations.

The importance of rare earths to Canada

In recognition of this potential, the Canadian Critical Minerals Strategy aims to increase the supply of responsibly sourced critical minerals and support the development of secure, reliable domestic and global value chains, in collaboration with our like-minded international partners, for clean technologies, information and communication technologies, and advanced manufacturing inputs, such as military and defence applications.

Due in part to their important role in these value chains, rare earth elements (REE) are among the minerals identified for initial prioritisation under the Strategy.

Permanent magnets represent over 90% of the market value for REE. They are an essential component of modern electronics such as cell phones, televisions, computers, automobiles (including electric vehicle motors), wind turbines, and jet aircraft, among other products. Neodymium magnets (or NdFeB magnets) are the most common type of permanent magnet used globally, having the highest magnetic field per unit of volume and being relatively low cost to produce. Neodymium (Nd), praseodymium (Pr), dysprosium (Dy), and terbium (Tb) are four of the key REE used to create NdFeB magnets.

Demand for and prices of all permanent magnets are forecast to increase significantly, in the range of over 25% to 40% by 2040, according to the International Energy Agency, largely due to both global and domestic growth in the electric vehicle (EV) and wind power sectors. As an example, demand for neodymium is anticipated to more than double from about 50,000 tonnes in 2022 to 125,000 tonnes by 2050.¹

The permanent magnet value chain consists of several stages, including extracting rare earths from ore, separating rare earths into individual oxides, and turning rare earths into alloys and magnets.

Currently, the NdFeB magnet value chain (covering mining, processing, and manufacturing) is heavily concentrated in China. Canada, its allies, and industry stakeholders worldwide are seeking to diversify the sourcing of rare earths to ensure a reliable, responsible, and sustainable supply as demand grows internationally and domestically in Canada.

This is an opportunity Canada is well positioned to seize due to our abundant mineral resources, advanced projects and innovative processes being developed across the value chain.

Opportunities for Canada’s rare earths

Canada has some of the world’s largest known reserves and resources (measured and indicated) of rare earths, estimated at over 15.2 million tonnes of rare earth oxide in 2023 and is host to several advanced exploration projects across the country. Some of these projects contain high concentrations of highly valued ‘heavy’ rare earths such as dysprosium and terbium that are in limited global supply.

Canada is also developing capacity in processing and separation, producing metal and alloy, and recycling rare earth magnets. Both the federal and provincial governments have announced funding support for initiatives along the value chain, including: Processing and separation operations in Saskatchewan; scaling up separation technology in Ontario; and Quebec and Ontario-based projects to scale up technology that recovers rare earths from magnetic waste. Several Canadian rare earth projects have also drawn funding and/or interest from the private sector, as well as Canada’s allies.

Canada also has the potential to develop magnet-making capacity, given it is already an established supplier of steel, aluminium, and alloys to automotive suppliers; has strong relationships with auto manufacturers; has a low-cost, clean power grid; and Canadian workers with established skilled manufacturing capabilities. As demand for EVs increases, permanent magnet manufacturing facilities could supply EV drivetrain production in North America.

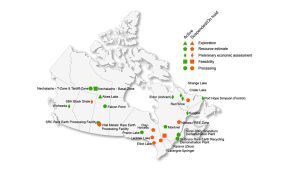

Map of Canadian REE deposits

Canada benefits from its attractiveness as a destination for foreign investment due to factors like its high environmental, social, and governance (ESG) standards, wide availability of clean and relatively cheap electricity, highly regarded innovation ecosystem, and reliability and security as a supply-chain participant.

While we look to maximise domestic opportunities, Canada understands that improved global coordination is required to create resilient and diversified permanent magnet value chains. The concentration of critical mineral production in a few countries overseas that use non-market-based practices raises the risk of supply chain disruptions and inflated prices of key minerals and materials for Canada and its allies.

The risk inherent to this concentration of production is being accentuated by geopolitical events, which further fuels supply uncertainties. In addition, some jurisdictions have not prioritised (ESG) standards, including in the resource development activities they undertake in other countries.

In important recognition of this reality, the Critical Minerals Strategy includes a Global Leadership and Security pillar, recognising that Canada can and must be a leader in the responsible, inclusive, and sustainable production of critical minerals and resilient value chains. This aligns with an accelerating interest among Canada’s allies to pursue collective action on critical minerals in support of the global transition to net zero.

As part of the green transition, advanced manufacturers are seeking to ensure their supply chains are carbon-competitive, environmentally sustainable, and respectful of human rights. As a trusted and reliable supplier of responsibly sourced mineral and metal products, Canada is well-positioned to be a leader in the responsible, inclusive, and sustainable production of critical minerals and resilient value chains.

Work under the Global Leadership and Security pillar of the Canada Critical Minerals Strategy is well underway. Since January 2020, Canada has formalised bilateral cooperation agreements on critical minerals with the United States, the European Union, and Japan. It is actively engaging with additional allies, such as the United Kingdom and the Republic of Korea.

Canada is also actively engaging key multilateral organisations on the topic of critical minerals and the transition to net-zero by 2050, including the Organisation for Economic Cooperation and Development (OECD); the G7/G20, including the G7’s Critical Minerals Five-Point Plan; the International Energy Agency and the Agency’s Critical minerals Working Party; the World Bank Climate Smart Mining Initiative; the Intergovernmental Forum on Mining, Minerals, Metals and Sustainable Development (IGF); the International Organization for Standardization; the Extractive Industries Transparency Initiative (EITI); the Conference on Critical Minerals and Materials – which Canada will chair in 2024; and the Minerals Security Partnership.

The federal government is supporting these efforts with investments and policy. This includes $70m for global partnerships to promote Canadian mining leadership, such as promoting ESG standards and supporting bilateral and multilateral critical mineral commitments, launching a Responsible Business Conduct (RBC) Strategy to continue enhancing Canada’s regulation abroad and strengthening the global RBC ecosystem, and policy commitments – including the leveraging of our existing ‘Towards Sustainable Mining’ framework – to drive the global uptake of ‘nature-forward’ mining practices that minimise and mitigate environmental impacts and work to return the land to its natural state.

Canada is uniquely positioned to take advantage of this global context. As a mineral-rich country, we are lucky to be endowed with many of the critical minerals needed for the green and digital economy, including REEs. We have clean energy resources and are carbon-competitive. Canada has mining expertise, advanced technologies, and manufacturing capabilities, and we have strong ESG credentials. This presents an opportunity for Canada – as a trusted global partner and supplier – to play a leadership role with our key allies in creating a more diversified global supply of critical minerals, such as for REEs.

Challenges confronting the rare earth industry

The global REE market is relatively small in terms of volumes of production. In 2023, there were approximately 350,000 tonnes of all total rare earth oxides produced globally (compared to 22 million tonnes of copper, for example).

The market is also relatively opaque, with limited pricing data, high price volatility, and the majority of market share held by only a few players, which increases the risk of pricing manipulation. As the dominant producer and consumer of rare earth products, developments in the Chinese domestic market have historically been critical to the global rare earths industry.

Demand and supply dynamics are complicated by the fact that rare earths are found and extracted together despite differences in the end market for each of them, which causes oversupply for some REEs.

Beyond market factors, there is a range of technical challenges confronting the industry. For example, the mineralogy of Canadian deposits is often complex and difficult to concentrate and process. Each ore is unique and requires specialised processing to produce a mixed rare earth salt for midstream separation and refining.

These processes are capital and operating-intensive, involving multiple units of operation. Long flowsheets are required to get to a purified, separated REE product. Further technology development is required to optimise recovery and manage radioactivity where applicable. Expertise in Canada and North America is beginning to build, and further investments in highly qualified personnel will help grow this emerging industry.

Role of innovation

Natural Resources Canada’s CanmetMINING research laboratory undertook a six-year REE Research and Development program, under which several advances were made to improve recoveries and reduce capital and operating expenses of REE mining. Work under the new Critical Minerals Research, Development and Demonstration program (CMRDD) will engage directly with the industry to build on this progress and address remaining gaps.

The following are specific examples of where federal researchers and other Canadian entities are making important research advancements.

Improving grades

Low ore grade is the primary weakness for Canadian projects trying to compete with others economically. To improve this challenge, a great deal of ongoing R&D is focused on pre-concentration and mineral processing. Many Canadian REE projects are now testing pre-concentration technologies such as sensor-based ore sorting and dense media separation. Federal researchers and academia alike are testing out novel and selective chemical reagents for flotation or other mineral processing methods to overcome this hurdle.

Reducing energy intensity

Most REE processing facilities rely on high temperatures (200°C to 600°C in the Chemical Decomposition step to extract REE from the minerals. Researchers from Canadian Federal laboratories are challenging this conventional approach, and they have successfully developed early-stage processes that operate at < 100°C and are applicable and effective for processing Canadian REE minerals. Some of these patent-pending processes are in the process of scale-up.

Improving separation

The separation of REE into individual elements is conventionally undertaken through a process known as solvent extraction, which requires hundreds of separation steps. Multiple groups in Canada are evaluating options/alternatives to make this process easier. For example, the Saskatchewan Research Council is manufacturing their own proprietary solvent extraction equipment in their Rare Earth processing facility under construction in Saskatoon, supported by an investment of almost $5m from the federal government.

Additionally, Ucore has developed RapidSX technology, accelerating the separation process at reduced costs, and is currently being demonstrated at a pilot plant in Kingston, Ontario. Federal and post-secondary researchers are investigating further novel technologies that can either complement or replace solvent extraction.

Strengthening International Standards

Canadian experts in REE represent Canada in the ISO efforts to draft standards for REE. Working with international partners, Canada is helping to ensure that pertinent and comprehensive standards are developed for the mining and processing of REE ores and the production of compounds and materials to supply manufacturers of REE-containing end-products.

In addition to the potential for REE production from primary sources, Natural Resources Canada’s Mining Value from Waste Program is looking to identify sources of critical minerals, including REE, from existing mine tailings. Reprocessing these tailings and repurposing the remaining residues would result in a pathway to creating a fully Canadian value chain while reducing the liability from long-term tailings storage.

Made-in-Canada processes are required to reduce processing steps, costs, and chemical and energy intensity while providing improved environmental performance. An important step is the piloting and demonstrating these novel processes to ensure successful scale-up and provide investor and regulator confidence.

Mining innovation is being driven by the needs of the net zero economy, and Canada is a global leader in this space. The Government of Canada is uniquely positioned to leverage our world-leading labs. We are working to catalyse the private sector to accelerate technological innovation in Canada’s critical minerals sector and associated industries, enhancing Canadian competitiveness and environmental performance.

Canada’s potential in the rare earths market

The net-zero energy transition, building a digital economy, and ensuring national security require a reliable and sustainable supply of neodymium magnets. The current status quo, with one non-market economy dominating production across the value chain, is untenable.

While no single country is going to address global capacity shortfalls at every stage, Canada is well-positioned to play an important role in diversifying supply. Canadian companies are already key global players in this market, and even more are stepping up with promising projects.

Through strengthened partnerships with provinces and territories, Indigenous communities, industry and international allies and partners, Canada can build on current positive momentum and see some of these projects through from pilots and demonstrations into commercial production. Canada continues to work closely with and support our like-minded international partners in critical mineral security through collaborative efforts to ensure secure, reliable, and sustainable global supply chains for the minerals and metals needed to meet our net-zero ambitions.

Canada is well positioned to be a global leader in critical minerals given our innovative industries, strong ESG credentials, clean energy, and regulatory regime. We know the race to net zero provides a tremendous and historic opportunity, and Canada is leading the way.

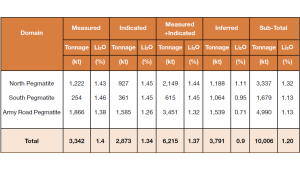

Lithium Springs Limited’s maiden MRE for the Brazil Lake lithium project signals a promising lithium reserve, coupled with an excellent location, making for an excellent lithium resource.

Lithium Springs Limited (LS1) is proud to announce our maiden Mineral Resource Estimate (MRE) for the Brazil Lake lithium (Li) project of 10.01 million tonnes @ 1.20% Li2O at a cutoff grade of 0.33% Li2O, reported under JORC (2012) guidelines. This highly encouraging outcome results from an extensive and well-executed drill programme that started in October 2022, and involved the drilling of 97 diamond core holes for over 26,700m and the use of 70 historic drill holes for approximately 6,600m.

Location of the Brazil Lake lithium project

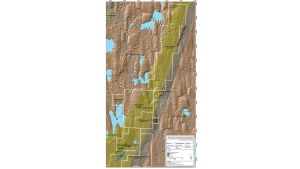

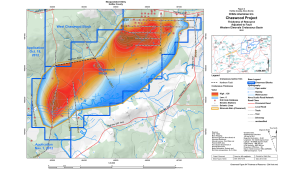

The Brazil Lake lithium project is located in southern Nova Scotia, Canada, approximately 25km north-east of Yarmouth and approximately 300km south-west of the city of Halifax (Fig. 1).

Fig. 1: Location of the Brazil Lake lithium project

The region can be accessed via highways 101 and 103, and the project area is easily accessible via Route 340 (bitumen road) and then along secondary gravel roads.

Geology and mineralisation