Its impressive attributes, such as its ability to improve the performance of solid oxide fuel cells and create strong yet lightweight alloys, are just the tip of the iceberg. By integrating scandium into lightweight alloys, industries can significantly reduce the weight of their products and, as a result, the energy required to move them.

Scandium-aluminum alloys, for example, offer a material that’s not only stronger and more corrosion-resistant but also significantly lighter than those currently in use. This means cars and planes that require less fuel, translating to lower greenhouse gas emissions.

In the realm of clean energy technologies, scandium plays a pivotal role in developing solid oxide fuel cells (SOFCs). These fuel cells, known for their high efficiency in electricity production, can operate at lower temperatures when scandium is added to their electrolyte materials.

This not only improves their performance and longevity but also reduces the overall cost, making clean technology more accessible and widespread.

Scandium’s role in sustainability

Harnessing the unique properties of scandium is key to advancing sustainable practices in industries worldwide.

In transportation, scandium plays a pivotal role. When added to aluminium alloys, scandium can create materials that are stronger and lighter than those currently in use.

This means that vehicles, from cars to aeroplanes, can weigh less and consequently consume less fuel, which directly translates into reduced greenhouse gas emissions.

Scandium’s sustainability benefits don’t end with fuel cells. Scandium’s industrial applications span further, from aerospace to sports equipment, each benefiting from the element’s ability to improve performance while lessening energy use and waste.

Global scandium resources

Assessing the world’s scandium resources reveals a complex landscape that is essential for strategic planning in clean energy development.

Resource evaluation indicates that scandium reserves are not evenly distributed across the globe. The global availability is concentrated in a few regions, and the current supply assessment shows that there is a growing interest in expanding scandium production.

For example, several countries are stepping up efforts to increase their scandium reserves. Moreover, market demand analysis shows a clear upward trajectory, with companies throughout the supply chain collaborating to secure scandium sources. To ensure the transition to clean energy, developing robust supply chains for this critical element requires investment in research and development of new extraction technologies.

Innovations in recovery methods

As we delve into the realm of scandium recovery, it’s clear that innovative techniques are pivotal to unlocking the element’s full potential for clean energy applications.

Improved extraction processes are at the forefront as they determine the viability and sustainability of scandium’s use, particularly in sectors eager to capitalise on its alloy enhancements.

Technological advancements have paved the way for more efficient recovery methods, meaning that you can expect to see more scandium entering the market.

Cutting-edge techniques now enable the recovery of scandium from sources previously considered non-viable, including tailings from other mining operations and industrial waste.

Moreover, recycling methods are becoming increasingly important. The idea is to reclaim scandium from end-of-life products and manufacturing scrap, thereby creating a closed-loop system that not only meets demand but does so with a reduced environmental footprint.

This circular economy approach to scandium supply reduces waste and ensures that every ounce of this valuable element is put to good use.

The implications are significant; with greater access to scandium, manufacturers can produce cleaner energy technologies and more efficient products. It’s a game-changer for industries looking to enhance performance while adhering to stringent environmental standards.

Imagine vehicles with improved fuel economy and reduced CO2 emissions—all thanks to the integration of scandium into the manufacturing process. This element’s potential is immense, and with these innovations in recovery, you’re witnessing a pivotal shift in the clean energy landscape.

Scandium’s future in clean energy

Scandium’s applications present significant enhancements in clean energy sectors, driving sustainable energy solutions that could curb our environmental woes.

Scandium’s environmental impact can’t be overstated. By enabling lighter, stronger materials, we’re looking at vehicles that consume less fuel and emit fewer greenhouse gases.

It’s not just cars and planes; scandium’s industrial uses span across wind turbines and aerospace components, areas where every ounce of weight reduction and every increment in strength translate to significant energy savings and sustainability.

However, current production levels can’t meet the voracious demands of a burgeoning clean energy sector. To capitalise on scandium’s potential, we need to see a dramatic shift in scandium production.

Think of the children playing in cleaner cities, the breath of fresh air in industrial heartlands—this is the landscape that could be cultivated by embracing scandium. It’s not just about the element; it’s about the future that can be shaped by it.

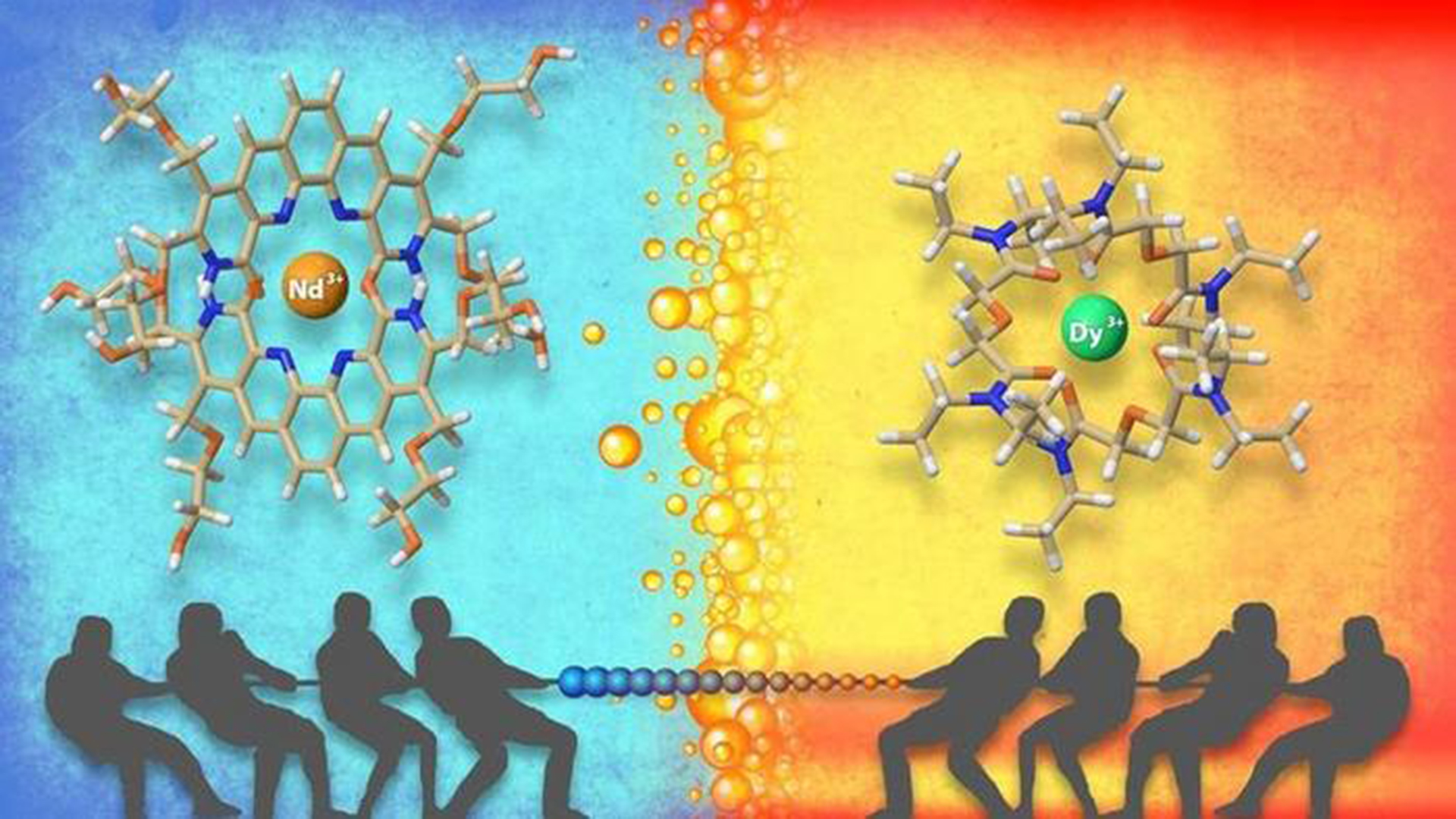

Researchers at Oak Ridge National Laboratory (ORNL) have pioneered a new method for separating critical metals known as lanthanides.

The scientists have devised an innovative ‘tug of war’ method that expertly separates and recovers precious lanthanides that are essential in a range of technologies.

These metals are widely used to manufacture clean energy technologies, such as electric vehicles, wind turbines, and even cancer treatments.

Santa Jansone-Popova of ORNL believes the new method will be crucial for obtaining these metals and enhancing sustainability: “Our approach is flexible and can be tailored to select specific lanthanides for a faster route to separating adjacent elements.

“Fundamental discoveries such as this one can advance economical and environmentally responsible separations strategies.”

Challenges with traditional separation techniques for lanthanides

There are 14 lanthanides, as well as yttrium and scandium, that are commonly known as rare earth elements.

Despite their name, they are not particularly rare, but they are often found in low concentrations, making their extraction challenging and costly.

Lanthanides exhibit similar chemical properties due to their electronic configuration, making them difficult to separate from one another.

These elements play crucial roles in various modern technologies due to their unique properties. For instance, cerium is utilised in catalytic converters to reduce harmful emissions from vehicles.

Neodymium and dysprosium are essential components of high-strength permanent magnets found in many electronic devices, including headphones, speakers, and electric motors in vehicles.

Europium is employed in phosphors for LED displays, producing vibrant colours in television screens and energy-efficient lighting.

Moreover, lanthanides find applications in nuclear technology, where they are used as control rods and shielding materials.

They are also integral to the production of lasers, fibre optics, and batteries for electric vehicles. Additionally, these elements contribute to the functionality of various medical devices, such as MRI machines and X-ray systems.

Overall, lanthanides play indispensable roles in modern technological advancements across numerous sectors, making advanced separation techniques vital.

Developing the tug of war method

To create their novel strategy, the scientists combined two types of organic substances known as ligands: one water-loving and the other oil-loving.

The fresh approach combines an oil-attracting ligand tailored for heavier lanthanides with a water-attracting counterpart designed for lighter elements. This strategic pairing engages in a tug of war, effectively separating lanthanides that pose significant challenges to divide.

Image courtesy of Adam Malin (with contributions from Santa Jansone-Popova and Alexander Ivanov), Oak Ridge National Laboratory

The scientists conducted experiments using two distinct liquids, oil and water, which do not mix. They dissolved the water-attracting substance in water and introduced the oil-attracting one into the oil phase.

Their findings revealed that this dual-liquid approach enhanced the separation of the lightest and heaviest rare earth elements more effectively than the previous single-liquid method.

Employing various analytical techniques, they investigated the interactions between these organic chemicals and rare earth elements, yielding valuable insights into the process mechanics and suggesting potential improvements for the separation system.

Combining an oil-attracting and a water-attracting compound to extract particular valuable elements from a chemical mixture is viable on an industrial level.

Upscaled, this process would enable the use of smaller equipment, reduce chemical usage, and decrease waste generation.

Consequently, the new approach would offer enhanced efficiency and environmental friendliness compared to traditional methods.

In a landmark move, the EU and Norway have sealed a partnership for sustainable land-based raw materials and battery value chains.

A Memorandum of Understanding (MoU), signed by Maroš Šefčovič, Executive Vice-President for the European Green Deal, and Jan Christian Vestre, Minister of Trade and Industry of the Kingdom of Norway, outlines a comprehensive framework for raw materials and battery value chains collaboration between the EU and Norway.

This significant agreement marks a pivotal milestone in the EU-Norway Green Alliance, initially announced by Commission President Ursula von der Leyen and Norwegian Prime Minister Jonas Gahr Støre in April 2023.

Leveraging their geographical proximity, the alliance aims to bolster integration, thereby mitigating the risks of trade disruptions while enhancing the overall competitiveness of both economies.

Moreover, the initiative is anticipated to generate high-quality job opportunities, contributing to sustainable economic growth.

The timing of the agreement is particularly poignant, coinciding with the 30th anniversary of the European Economic Area Agreement, which solidifies Norway’s participation in the Single Market.

This agreement has long been hailed as a cornerstone of EU-Norway relations, emphasising the mutual benefits and potential for further collaboration.

Šefčovič commented: “We are bringing cooperation between the EU and Norway to another level, as today’s signature is of strategic value.

“It will create a wide range of business and research opportunities on both sides, strengthening both our industrial base and our political bond.”

How Norway will bolster EU raw materials and battery value chains

Norway, a nation abundant in mineral resources, including rare earths, magnesium, titanium, vanadium, and phosphate rock, boasts a substantial processing capacity for various raw materials.

Over recent years, Norway has witnessed a notable surge in the battery sector, marked by the emergence of numerous ventures spanning the entire value chain.

These vast resources and expertise will be essential to reinforcing EU raw materials and battery value chains.

Supporting the growing EU battery sector

The EU boasts a flourishing market for green technologies, particularly batteries, with an estimated demand reaching 175 GWh in 2023.

The EU’s battery industry stands as the second-largest globally, supported by existing facilities capable of ramping up to 220 GWh in capacity.

Moreover, the region is witnessing a surge in battery manufacturing endeavours, with an additional 1 TWh of projects either announced or currently in the construction phase.

This robust demand landscape presents a plethora of opportunities for forging offtake agreements, engaging in joint ventures, and collaborating on research and innovation (R&I) projects.

Furthermore, the EU is actively harnessing its potential in critical and strategic raw materials, paving the way for potential collaborations with Norwegian counterparts.

Details of the EU-Norway partnership

The MoU establishes a robust framework for close collaboration between the EU and Norway across five key areas:

Integration of raw materials and battery value chains

The MoU aims to foster joint investment projects by facilitating partnerships such as joint ventures, consortia, and special-purpose vehicles among industrial players.

This collaboration seeks to link final users with raw materials suppliers, enhancing efficiency and sustainability across the value chains.

Co-operation on research and innovation (R&I)

Both parties commit to collaborative R&I efforts, leveraging joint projects to drive potential industrial adoption and implementation.

Norway’s active participation in the EU Framework Programme for R&I – Horizon 2020 and its continued involvement in Horizon Europe underscores the commitment to advancing innovation collectively.

Adherence to high environmental, social, and governance standards

The MoU promotes the application of rigorous environmental, social, and governance standards throughout the raw materials and battery value chains.

Mutual consultation and exchange of information on relevant policies and initiatives, including recycling and waste management, will facilitate the adoption of best practices.

Mobilisation of financial and investment instruments

This mobilisation aims to accelerate the development and deployment of sustainable initiatives within the raw materials and battery sectors.

Development of skills for high-quality jobs

The MoU emphasises the importance of nurturing the necessary skills for high-quality jobs in the raw materials and battery sectors.

Stakeholder mobilisation and financial support for initiatives such as the European Battery Academy will play a pivotal role in enhancing workforce capabilities and driving sectoral growth.

Following the signing of the deal, the EU and Norway will collaborate with stakeholders to implement the roadmap for the partnership.

Australia’s government will inject AU$840m into a rare earths refinery in the country’s north as part of efforts to boost the country’s role in the energy transition supply chain.

Albanese explained: “My government is focused on a future made in Australia, and this project is an important part of that plan.

“We will deliver critical jobs and economic development in the heart of the Territory and the north.”

The importance of a domestic supply of rare earths

Rare earths are a group of 17 elements, four of which are essential for permanent magnets used in a variety of technologies, including electric vehicle batteries and wind turbines.

Australia has made efforts to reduce its dependence on China for the minerals.

However, this remains difficult as China accounts for 70% of rare earth supplies, 85% of rare earth processing, and 90% of rare-earth magnet production.

The government hopes the rare earths refinery will encourage international financiers and banks to back the project, which it says will create 300 new jobs.

The rare earths refinery is set to hugely contribute to global supplies

Speaking with Australia’s national broadcaster, Minister for Resources Madeleine King said while it was “a lot of money,” the funds were going toward a very important project that could provide up to 5% of global supply.

She said: “The refinery will be the first fully integrated mine and processing facility that will produce rare earth oxide, which will be used in really important and advanced technology for green technology and defence applications.”

Australia wants to move further downstream and capture more value from its raw material exports, particularly in critical minerals like rare earths.

It is home to Lynas, the only rare earths miner and processor with supply chains outside of China.

Under Scott Morrison, Australia’s former prime minister, the government in 2022 approved a $1.25bn loan to critical minerals company Iluka Resources to develop the country’s first rare earths refinery in Western Australia.

However, its critical minerals ambitions have faced headwinds, as other battery metals like nickel and lithium suffer from price slumps, with demand for EVs growing slower than forecast.

Nickel miners in Australia, in particular, have been hit hard by an increase in supply from Indonesia.

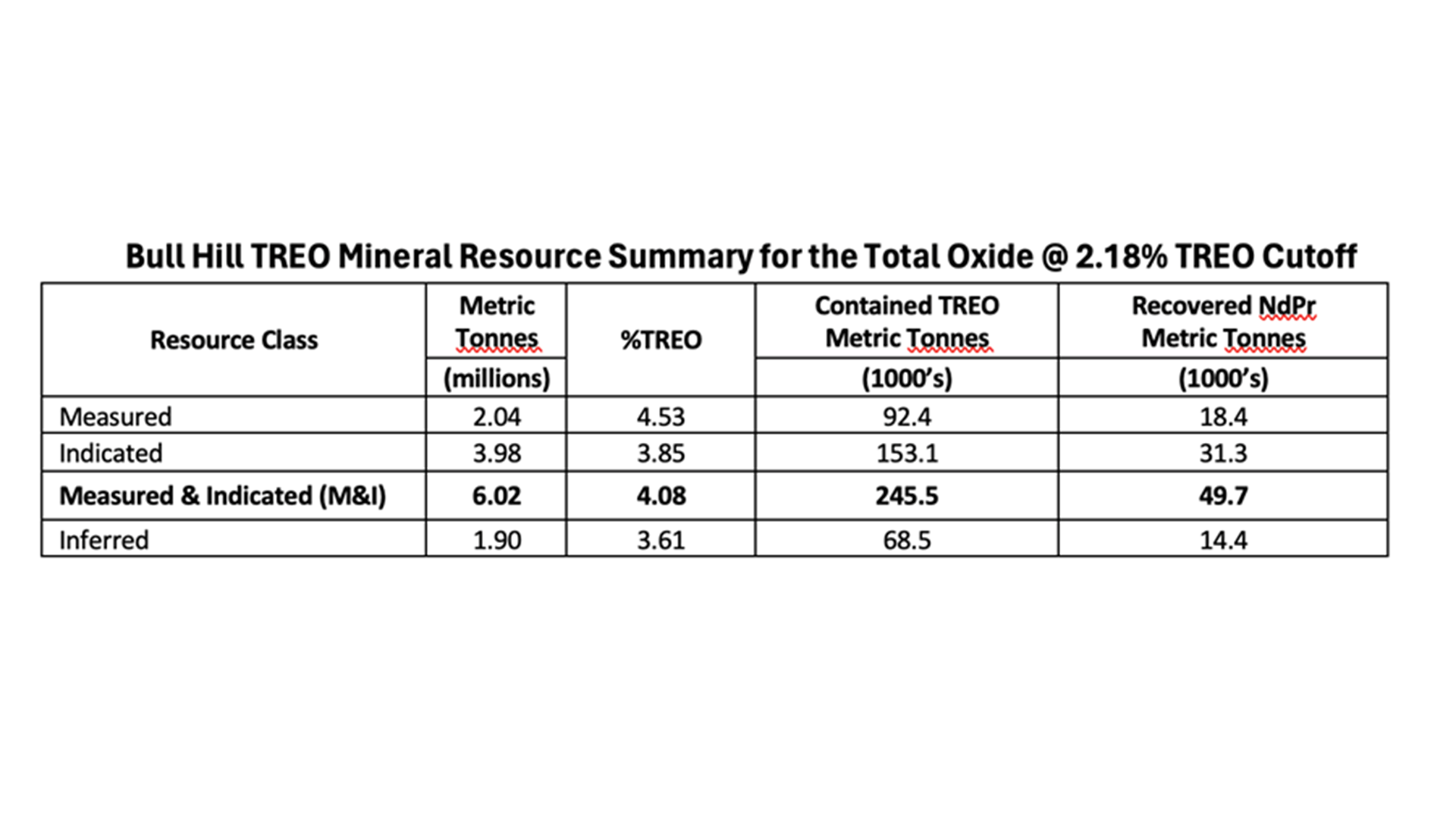

The magnet materials explored in the new resource estimate include neodymium (Nd), praseodymium (Pr), terbium (Tb), dysprosium (Dy), and other critical rare earths like lanthanum (La).

This estimate centres on the Bull Hill deposit within the Bear Lodge Project, situated in northeastern Wyoming. The project also holds promising potential in the Carbon, Whitetail, and Taylor deposits within the Company’s mineral claims.

Excellent magnet materials potential identified

The mineral resource estimation utilised comprehensive data extracted from 252 core holes drilled between 2009 and 2013.

These holes provided 20,491 assay intervals, amounting to 186,712.5 feet (56,910 meters) of drilling from the Company’s extensive drill hole database.

With approximately 500 drill holes and over 285,000 feet (86,868 meters) of core, this database offers a robust foundation for analysis.

Additionally, the estimation integrated recovery data derived from the 2021 pilot plant testing of the Company’s proprietary recovery and separation technology.

This technology is currently being implemented in the demonstration plant project underway in Upton, Wyoming.

Focusing on the oxide and oxide-carbonate zones, deemed optimal for yielding the best recoveries and costs, the mineral resource estimate utilised a cut-off grade of 2.18% total rare earth oxide (TREO).

Resource Notes: (1) Mineral resources do not have demonstrated economic viability. There is no guarantee that any part of the mineral resource will be converted to mineral reserves in the future. All figures are rounded to reflect the accuracy of the grade and tonnage estimates. (2) This mineral resource estimate is reported in accordance with Regulation S-K (CFR Title 17 Part 229 Items 1300-1305) at a cut-off grade of 2.18% TREO. (3) Only certain rare earth elements (La, Nd, Pr, Dy, and a heavy rare earth element mixed oxide including Yb, Tm, Tb, Er, Ho, Lu) are considered payable for pit optimization purposes. Commodity price assumptions used in the preparation of the mineral resource estimateare set forth in the TRS. (4) The estimated overall NdPr process recovery is 90%.

Brent Berg, President and CEO of the Company, commented: “With demand for magnet materials expected to grow exponentially over the next 30 years, driven primarily by their use in defence and green technologies, it makes sense to focus our efforts on those key magnet materials in this resource model.

“This will ensure that, over the longer term, we are aligned with the national security interests and decarbonisation goals of the United States.

“Our proprietary rare earth recovery and separation technology enabled us to look at the body of geological data we have generated through a different lens.

“That work allows us to focus on a higher grade and smaller pit design. I believe this strategy provides the greatest opportunity for the Company to capitalise on the projected rare earth demand growth and most clearly aligns with our innovative technology while allowing us to preserve the long-term, upside potential of the Bear Lodge Project.”

Preparation of technical reports

In compliance with regulations, Rare Element Resources is preparing a Technical Report Summary (TRS) under Regulation S-K (CFR Title 17 Part 229 Items 601(b)(96) and 1300-1305). This summary will be filed concurrently with this release on a current report on Form 8-K and will be accessible at www.sec.gov.

Moreover, an updated technical report conforming to Canadian National Instrument NI 43-101 – Standards of Disclosure for Mineral Projects (“NI 43-101”) is in the works.

This report will be filed on the Company’s SEDAR profile at www.sedarplus.ca within 45 days from the release date of this press statement.

The mineral resource work and technical reports are spearheaded by Alan C. Noble, P.E., the principal engineer of Ore Reserves Engineering (ORE). Noble’s extensive modelling work on the Bear Lodge Project over the past decade has been instrumental in this endeavour.

The forthcoming reports will comprehensively detail the economic assumptions and cut-off grade sensitivity used in the evaluation.

The Natural Resources Canada discusses the potential of Canada’s rare earths and the importance of responsible sourcing to meet increasing demand for clean energy technologies.

The demand for minerals and metals associated with the clean energy transition and the transition to zero-emission vehicles is expected to increase significantly over the next ten years. Fortunately, Canada possesses significant potential to increase the mining and processing of many of these critical minerals, which will drive economic growth in Canada, create jobs for Canadian workers, and reduce Canada and our allies’ vulnerability to supply risks.

In this context, Canada is utilising its potential to step up to develop secure and stable supply chains for the minerals and metals essential to reaching net zero and support likeminded partners in critical minerals security to insulate Canada and its allies from geopolitics and reliance on an anti-market economy or anti-democratic nations.

The importance of rare earths to Canada

In recognition of this potential, the Canadian Critical Minerals Strategy aims to increase the supply of responsibly sourced critical minerals and support the development of secure, reliable domestic and global value chains, in collaboration with our like-minded international partners, for clean technologies, information and communication technologies, and advanced manufacturing inputs, such as military and defence applications.

Due in part to their important role in these value chains, rare earth elements (REE) are among the minerals identified for initial prioritisation under the Strategy.

Permanent magnets represent over 90% of the market value for REE. They are an essential component of modern electronics such as cell phones, televisions, computers, automobiles (including electric vehicle motors), wind turbines, and jet aircraft, among other products. Neodymium magnets (or NdFeB magnets) are the most common type of permanent magnet used globally, having the highest magnetic field per unit of volume and being relatively low cost to produce. Neodymium (Nd), praseodymium (Pr), dysprosium (Dy), and terbium (Tb) are four of the key REE used to create NdFeB magnets.

Demand for and prices of all permanent magnets are forecast to increase significantly, in the range of over 25% to 40% by 2040, according to the International Energy Agency, largely due to both global and domestic growth in the electric vehicle (EV) and wind power sectors. As an example, demand for neodymium is anticipated to more than double from about 50,000 tonnes in 2022 to 125,000 tonnes by 2050.¹

The permanent magnet value chain consists of several stages, including extracting rare earths from ore, separating rare earths into individual oxides, and turning rare earths into alloys and magnets.

Currently, the NdFeB magnet value chain (covering mining, processing, and manufacturing) is heavily concentrated in China. Canada, its allies, and industry stakeholders worldwide are seeking to diversify the sourcing of rare earths to ensure a reliable, responsible, and sustainable supply as demand grows internationally and domestically in Canada.

This is an opportunity Canada is well positioned to seize due to our abundant mineral resources, advanced projects and innovative processes being developed across the value chain.

Opportunities for Canada’s rare earths

Canada has some of the world’s largest known reserves and resources (measured and indicated) of rare earths, estimated at over 15.2 million tonnes of rare earth oxide in 2023 and is host to several advanced exploration projects across the country. Some of these projects contain high concentrations of highly valued ‘heavy’ rare earths such as dysprosium and terbium that are in limited global supply.

Canada is also developing capacity in processing and separation, producing metal and alloy, and recycling rare earth magnets. Both the federal and provincial governments have announced funding support for initiatives along the value chain, including: Processing and separation operations in Saskatchewan; scaling up separation technology in Ontario; and Quebec and Ontario-based projects to scale up technology that recovers rare earths from magnetic waste. Several Canadian rare earth projects have also drawn funding and/or interest from the private sector, as well as Canada’s allies.

Canada also has the potential to develop magnet-making capacity, given it is already an established supplier of steel, aluminium, and alloys to automotive suppliers; has strong relationships with auto manufacturers; has a low-cost, clean power grid; and Canadian workers with established skilled manufacturing capabilities. As demand for EVs increases, permanent magnet manufacturing facilities could supply EV drivetrain production in North America.

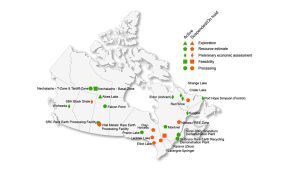

Map of Canadian REE deposits

Canada benefits from its attractiveness as a destination for foreign investment due to factors like its high environmental, social, and governance (ESG) standards, wide availability of clean and relatively cheap electricity, highly regarded innovation ecosystem, and reliability and security as a supply-chain participant.

While we look to maximise domestic opportunities, Canada understands that improved global coordination is required to create resilient and diversified permanent magnet value chains. The concentration of critical mineral production in a few countries overseas that use non-market-based practices raises the risk of supply chain disruptions and inflated prices of key minerals and materials for Canada and its allies.

The risk inherent to this concentration of production is being accentuated by geopolitical events, which further fuels supply uncertainties. In addition, some jurisdictions have not prioritised (ESG) standards, including in the resource development activities they undertake in other countries.

In important recognition of this reality, the Critical Minerals Strategy includes a Global Leadership and Security pillar, recognising that Canada can and must be a leader in the responsible, inclusive, and sustainable production of critical minerals and resilient value chains. This aligns with an accelerating interest among Canada’s allies to pursue collective action on critical minerals in support of the global transition to net zero.

As part of the green transition, advanced manufacturers are seeking to ensure their supply chains are carbon-competitive, environmentally sustainable, and respectful of human rights. As a trusted and reliable supplier of responsibly sourced mineral and metal products, Canada is well-positioned to be a leader in the responsible, inclusive, and sustainable production of critical minerals and resilient value chains.

Work under the Global Leadership and Security pillar of the Canada Critical Minerals Strategy is well underway. Since January 2020, Canada has formalised bilateral cooperation agreements on critical minerals with the United States, the European Union, and Japan. It is actively engaging with additional allies, such as the United Kingdom and the Republic of Korea.

Canada is also actively engaging key multilateral organisations on the topic of critical minerals and the transition to net-zero by 2050, including the Organisation for Economic Cooperation and Development (OECD); the G7/G20, including the G7’s Critical Minerals Five-Point Plan; the International Energy Agency and the Agency’s Critical minerals Working Party; the World Bank Climate Smart Mining Initiative; the Intergovernmental Forum on Mining, Minerals, Metals and Sustainable Development (IGF); the International Organization for Standardization; the Extractive Industries Transparency Initiative (EITI); the Conference on Critical Minerals and Materials – which Canada will chair in 2024; and the Minerals Security Partnership.

The federal government is supporting these efforts with investments and policy. This includes $70m for global partnerships to promote Canadian mining leadership, such as promoting ESG standards and supporting bilateral and multilateral critical mineral commitments, launching a Responsible Business Conduct (RBC) Strategy to continue enhancing Canada’s regulation abroad and strengthening the global RBC ecosystem, and policy commitments – including the leveraging of our existing ‘Towards Sustainable Mining’ framework – to drive the global uptake of ‘nature-forward’ mining practices that minimise and mitigate environmental impacts and work to return the land to its natural state.

Canada is uniquely positioned to take advantage of this global context. As a mineral-rich country, we are lucky to be endowed with many of the critical minerals needed for the green and digital economy, including REEs. We have clean energy resources and are carbon-competitive. Canada has mining expertise, advanced technologies, and manufacturing capabilities, and we have strong ESG credentials. This presents an opportunity for Canada – as a trusted global partner and supplier – to play a leadership role with our key allies in creating a more diversified global supply of critical minerals, such as for REEs.

Challenges confronting the rare earth industry

The global REE market is relatively small in terms of volumes of production. In 2023, there were approximately 350,000 tonnes of all total rare earth oxides produced globally (compared to 22 million tonnes of copper, for example).

The market is also relatively opaque, with limited pricing data, high price volatility, and the majority of market share held by only a few players, which increases the risk of pricing manipulation. As the dominant producer and consumer of rare earth products, developments in the Chinese domestic market have historically been critical to the global rare earths industry.

Demand and supply dynamics are complicated by the fact that rare earths are found and extracted together despite differences in the end market for each of them, which causes oversupply for some REEs.

Beyond market factors, there is a range of technical challenges confronting the industry. For example, the mineralogy of Canadian deposits is often complex and difficult to concentrate and process. Each ore is unique and requires specialised processing to produce a mixed rare earth salt for midstream separation and refining.

These processes are capital and operating-intensive, involving multiple units of operation. Long flowsheets are required to get to a purified, separated REE product. Further technology development is required to optimise recovery and manage radioactivity where applicable. Expertise in Canada and North America is beginning to build, and further investments in highly qualified personnel will help grow this emerging industry.

Role of innovation

Natural Resources Canada’s CanmetMINING research laboratory undertook a six-year REE Research and Development program, under which several advances were made to improve recoveries and reduce capital and operating expenses of REE mining. Work under the new Critical Minerals Research, Development and Demonstration program (CMRDD) will engage directly with the industry to build on this progress and address remaining gaps.

The following are specific examples of where federal researchers and other Canadian entities are making important research advancements.

Improving grades

Low ore grade is the primary weakness for Canadian projects trying to compete with others economically. To improve this challenge, a great deal of ongoing R&D is focused on pre-concentration and mineral processing. Many Canadian REE projects are now testing pre-concentration technologies such as sensor-based ore sorting and dense media separation. Federal researchers and academia alike are testing out novel and selective chemical reagents for flotation or other mineral processing methods to overcome this hurdle.

Reducing energy intensity

Most REE processing facilities rely on high temperatures (200°C to 600°C in the Chemical Decomposition step to extract REE from the minerals. Researchers from Canadian Federal laboratories are challenging this conventional approach, and they have successfully developed early-stage processes that operate at < 100°C and are applicable and effective for processing Canadian REE minerals. Some of these patent-pending processes are in the process of scale-up.

Improving separation

The separation of REE into individual elements is conventionally undertaken through a process known as solvent extraction, which requires hundreds of separation steps. Multiple groups in Canada are evaluating options/alternatives to make this process easier. For example, the Saskatchewan Research Council is manufacturing their own proprietary solvent extraction equipment in their Rare Earth processing facility under construction in Saskatoon, supported by an investment of almost $5m from the federal government.

Additionally, Ucore has developed RapidSX technology, accelerating the separation process at reduced costs, and is currently being demonstrated at a pilot plant in Kingston, Ontario. Federal and post-secondary researchers are investigating further novel technologies that can either complement or replace solvent extraction.

Strengthening International Standards

Canadian experts in REE represent Canada in the ISO efforts to draft standards for REE. Working with international partners, Canada is helping to ensure that pertinent and comprehensive standards are developed for the mining and processing of REE ores and the production of compounds and materials to supply manufacturers of REE-containing end-products.

In addition to the potential for REE production from primary sources, Natural Resources Canada’s Mining Value from Waste Program is looking to identify sources of critical minerals, including REE, from existing mine tailings. Reprocessing these tailings and repurposing the remaining residues would result in a pathway to creating a fully Canadian value chain while reducing the liability from long-term tailings storage.

Made-in-Canada processes are required to reduce processing steps, costs, and chemical and energy intensity while providing improved environmental performance. An important step is the piloting and demonstrating these novel processes to ensure successful scale-up and provide investor and regulator confidence.

Mining innovation is being driven by the needs of the net zero economy, and Canada is a global leader in this space. The Government of Canada is uniquely positioned to leverage our world-leading labs. We are working to catalyse the private sector to accelerate technological innovation in Canada’s critical minerals sector and associated industries, enhancing Canadian competitiveness and environmental performance.

Canada’s potential in the rare earths market

The net-zero energy transition, building a digital economy, and ensuring national security require a reliable and sustainable supply of neodymium magnets. The current status quo, with one non-market economy dominating production across the value chain, is untenable.

While no single country is going to address global capacity shortfalls at every stage, Canada is well-positioned to play an important role in diversifying supply. Canadian companies are already key global players in this market, and even more are stepping up with promising projects.

Through strengthened partnerships with provinces and territories, Indigenous communities, industry and international allies and partners, Canada can build on current positive momentum and see some of these projects through from pilots and demonstrations into commercial production. Canada continues to work closely with and support our like-minded international partners in critical mineral security through collaborative efforts to ensure secure, reliable, and sustainable global supply chains for the minerals and metals needed to meet our net-zero ambitions.

Canada is well positioned to be a global leader in critical minerals given our innovative industries, strong ESG credentials, clean energy, and regulatory regime. We know the race to net zero provides a tremendous and historic opportunity, and Canada is leading the way.

Discarded fluorescent bulbs have previously been recycled for glass and mercury, but researchers have found that they could also be used to recycle rare earths.

Rare earths, a group of 17 metals, are not yet widely available and aren’t easily extracted with existing recycling methods, despite their societal importance.

Now, a team of researchers have discovered a new method to collect slightly magnetic particles from spent fluorescent bulbs that contain rare earths.

Because of their unique magnetic, electrical, and optical characteristics, rare earths are used in many modern technologies, such as electric vehicles and microchips.

However, untapped deposits of these metals are rare.

On top of this, large-scale methods to recycle rare earths from outdated devices are a challenge because the metals are integrated into different components and are only present in small amounts.

Rare earths in fluorescent bulbs

Mixtures of rare earth-based phosphors, the substances that contribute to a light’s colour, are found in a thin coating inside the fluorescent bulb.

Because of this, the team wanted to develop a low-tech method to easily collect these phosphors. The method would take advantage of the elements’ weak magnetic properties.

The team utilised a magnetic field

In their rare earth recycling method, the researchers used a wire coil to apply a magnetic field to a glass chromatography column filled with stacked disks of stainless-steel mesh. A demonstration sample was then prepared, which was passed through the column to see if it could capture the phosphors.

The team first obtained three different weakly magnetic rare earth phosphors from a lamp manufacturer. They then mimicked old fluorescent lamp parts by mixing the phosphor particles in a liquid solution with nonmagnetic silica oxide and strongly magnetic iron oxide nanoparticles. These represented glass and metal components in the bulbs.

When the liquid was injected and flowed through the chromatography column, the phosphors and iron oxide nanoparticles stuck to the magnetised stainless-steel mesh. The water and silica particles flowed out the other end.

Removing the phosphors

The team removed the phosphors from the column by slowly reducing the strength of the external magnetic field while rinsing the column with liquid.

The magnetic iron oxide nanoparticles were released from the column when the magnetic field was turned off.

A 93% recovery rate

The researchers found that their method recovered 93% of the rare earth phosphors from the initial mixture that mimicked lamp components.

Although more work is needed to separate individual rare earths from phosphors and to scale the method for industrial recycling applications, the team believe that their approach is a step forward in rare earth recycling for a more sustainable future.

Lithium Springs Limited’s maiden MRE for the Brazil Lake lithium project signals a promising lithium reserve, coupled with an excellent location, making for an excellent lithium resource.

Lithium Springs Limited (LS1) is proud to announce our maiden Mineral Resource Estimate (MRE) for the Brazil Lake lithium (Li) project of 10.01 million tonnes @ 1.20% Li2O at a cutoff grade of 0.33% Li2O, reported under JORC (2012) guidelines. This highly encouraging outcome results from an extensive and well-executed drill programme that started in October 2022, and involved the drilling of 97 diamond core holes for over 26,700m and the use of 70 historic drill holes for approximately 6,600m.

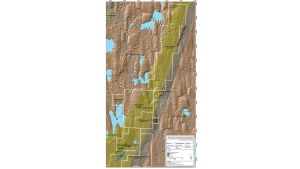

Location of the Brazil Lake lithium project

The Brazil Lake lithium project is located in southern Nova Scotia, Canada, approximately 25km north-east of Yarmouth and approximately 300km south-west of the city of Halifax (Fig. 1).

Fig. 1: Location of the Brazil Lake lithium project

The region can be accessed via highways 101 and 103, and the project area is easily accessible via Route 340 (bitumen road) and then along secondary gravel roads.

Geology and mineralisation

The highly evolved, spodumene-bearing pegmatites within the Brazil Lake lithium project that are the focus of Lithium Springs Limited’s exploration are hosted by meta-sedimentary and meta-volcanic rocks of the White Rock Formation sequence, which locally include quartzite, amphibolite, tuff, psammite and pelitic schist and strikes northeast/southwest and locally dips steeply to both north-west and south-east. These rocks are part of the south-western part of the Meguma terrane of the Canadian Appalachian Orogen. The favourable geology of the host sub-unit, the Government Brook Member, bounded on the east by a major regional shear zone, extends greater than nine kilometres NE of the drilling to date.

Exploration and drilling

The most recent exploration and drilling on the Brazil Lake lithium project was completed by Lithium Springs Limited, in conjunction with our project partners Champlain Mineral Ventures Ltd. (a GOLDFIELDS Group Company). Before LS1’s involvement in the project, all previous exploration of the Brazil Lake lithium project and the surrounding areas was completed by Champlain Mineral Ventures Ltd; other than some early-stage exploration completed by the Nova Scotia Department of Natural Resources and Renewables (NSDNRR) between 1960-1993, which included five drill holes for a total of 577m.

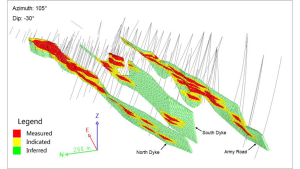

Fig. 2a: Location of the three spodumene-bearing pegmatite bodies relative to the Brazil Lake lithium project tenure

Champlain completed 16 diamond drill holes for a total of 1,325m in 2002; 16 diamond drill holes for a total of 801m in 2003; 28 drill holes for a total of 2,666m in 2010; five drill holes for a total of 505m in 2019; and six drill holes for a total of 1018m in 2020, as well as field mapping and sampling (including pits), soil surveys, trenching, and geophysics.

This sample was then subjected to metallurgical test work, which produced a spodumene concentrate with highly encouraging Li2O grade and recoveries utilising heavy liquid separation. Lithium Springs is currently in the process of verifying the historical metallurgical test work through independently verified test work to be completed by SGS Lakefield, Canada.

Fig. 2b: Extent of Government Brook Member relative to known dykes

Mineral resource estimate

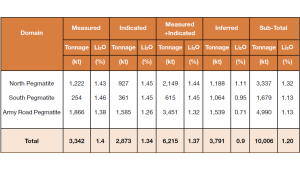

The Brazil Lake lithium project mineral resource estimate (MRE) as of 6 August 2023 is 10.01MT @ 1.20% Li2O at a cutoff grade of 0.33% Li2O and is reported in accordance with JORC (2012) guidelines by the independent mining consultants, JP Geoconsulting Services. This MRE results from a combination of three spodumene-bearing pegmatites: the Army Road Pegmatite, North Pegmatite and South Pegmatite (Figs. 2 and 3).

Fig. 3: Three mineralisation domains’ MRE by category (at 0.33% Li2O cutoff grade)

A breakdown of the mineral resource estimate by Li2O% cutoff grade and resource confidence classification from these three pegmatites is shown in Table 1.

Table 1: Breakdown of Mineral Resource Estimate by classification at 0.33% Li2O cutoff grade

The Brazil Lake Lithium Project is comprised of three ore bodies – North Pegmatite, South Pegmatite, and the Army Road Pegmatite, all aligned in parallel, dipping steeply and at a downward plunge of 20° to the SSW. The North Peg and South Peg outcrop at the surface, while the Army Road Pegmatite is covered at the closest point to the surface of five metres of cover.

The combination of 6,500m of historic drilling and the Lithium Springs fully-funded 28,000m of diamond drilling has produced an outstanding maiden JORC resource of 10.01Mt @ 1.20% Li2O at 0.33% Li2O cutoff grade. The Brazil Lake project has real mine development potential located in a Tier 1 mining jurisdiction with significant Canadian federal and Nova Scotian provincial government incentives that match the funds available under the US federal government’s Inflation Reduction Act, and development grants from the US Departments of Defense and Energy. These present further funding opportunities for critical mineral development, especially given Canada’s classification as a US domestic supply source.

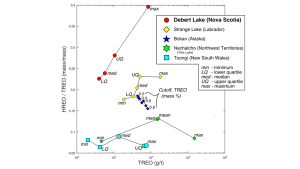

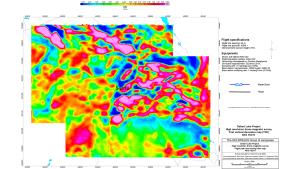

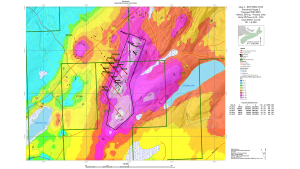

The Debert Lake Heavy Rare Earth deposit

Magnum Resources Inc (a GOLDFIELDS Group company) owns a 100% interest in the property. The property is located in northern Nova Scotia, 25km NW of Truro. It is on forestry land and is serviced by a logging road within eight kilometres of a sealed highway and the power grid.

Assays from 235 samples of outcrop and drill core show that key elements by value (>80%) include: Europium, Erbium, Thulium and Ytterbium.

High-resolution (25m line spacing) magnetic drone surveys have identified new drill targets on the heavy REE deposit at Debert Lake, owned by Magnum Resources Inc. (a GOLDFIELDS Group company). The deposit features the highest ratio (~75%) of heavy to light of any REE deposit in North America. REEs have been designated as a critical mineral by both Nova Scotia and Canada, as well as the EU.

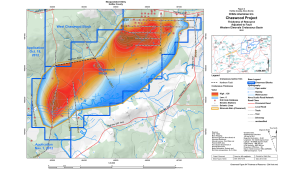

The Frenchvale Flake Graphite deposit

Mt. Cameron Minerals Inc. (a GOLDFIELDS Group company) owns 100% interest in the property. It is under option to Argyle Resources Corp., which is committed to spending $4.4m over four years to earn a 60% interest.

The Frenchvale Flake Graphite deposit is located 25km west of Sydney, Cape Breton Island, Nova Scotia, Canada. The deposit is hosted in Grenville Age marbles and has a strike length of eight kilometres. Sealed highways service it, and it is on the power grid.

Flake Graphite has been designated as a critical mineral by both Nova Scotia and Canada.

Deep drilling is planned on geophysical (TDEM CH13) targets as above.

The Chaswood Aluminium (Kaolin) deposit

AlNova Mining Inc. (a GOLDFIELDS Group company) owns 100% interest in the deposit.

The deposit is hosted in unconsolidated cretaceous secondary deposits of kaolin and high-purity quartz sand lenses. The deposit is found at the surface under glacial till. It is considered one of Canada’s largest aluminium deposits, with >600 million tonnes of kaolin at a grade of >30% Al2O3. It is located in central Nova Scotia, 50km NE of the port of Halifax. It is on forest land within three kilometres of a sealed highway and power grid. It is suitable for mining by dragline with a very low strip ratio and is within eight kilometres of a gas pipeline.

The estimated resource was calculated from diamond drilling and seismic profile surveys. The kaolin and sand are suitable as additives for the production of cement. Designated as a critical mineral by Canada, the kaolin can be initially refined to SGA alumina or further for electronic applications.

Please note, this article will also appear in the seventeenth edition of our quarterly publication.

The Québec Mining Association, an association with 88 years of experience in Québec’s mining landscape, explores the future production of Québec rare earths and plans to promote sustainable mining practices.

Rare earth elements (REE) are one group of these critical materials, and various countries are stepping up their production of these. The province of Québec is well-known for its quantity of rare earths, meaning they are well positioned to ramp up exploration and production.

The Québec Mining Association (QMA), the association acting as the voice and representative of the mining industry in Québec, attending governmental policy discussions and promoting the interests of their communities and mining companies, tells us more about the future of the region.

Can you provide an overview of the recent projects undertaken by the Québec Mining Association (QMA)? How are these projects aligned with the Québec Mining Association’s long-term objectives?

The QMA is beginning a new strategic cycle with a plan that will run until 2026. The Board of Directors has adopted a new vision to further propel the QMA and the industry. Its new vision is:

‘In 2030, the QMA is recognised by its stakeholders as the catalyser for the mining industry, inspiring its members to follow an ethical approach and enabling them to respect the highest environmental, social and governance standards.’

The new strategic plan has five orientations:

To reposition the industry’s communication strategy to focus on its tangible ESG achievements (leadership through action, lead by example);

To improve the social acceptability and environmental and social performance of mining companies;

To ensure the competitiveness and sustainability of the industry;

To become a key player in the decarbonisation of the economy (positioning the industry as a real solution to certain climate issues); and

To maintain its organisational strength of influence and increase its legitimacy.

Communication, the protection of the environment, and social acceptability will be at the heart of the following Action Plan. The QMA will put forward the know-how and innovations of the mining companies to reduce the environmental footprint and inform the population and stakeholders of the good practices of the mining industry in Québec.

In 2023, the QMA participated in many public consultations and concluded that the population generally does not know the mining industry well. The public is unaware of our industry’s legal and regulatory obligations and of how the mining industry works to reduce its environmental footprint. The QMA hopes that its new strategic plan will help improve that knowledge.

What role does the Québec Mining Association see for rare earths in the global push towards electric vehicles and renewable energy?

Rare earth elements are part of the critical minerals necessary for the transition to a low-carbon economy. It is well known that the global demand for critical minerals, including REE, will rise significantly as the adoption of electric vehicles and renewable energy technologies continues to grow.

Currently, no REE mines are in operation in Québec, but many deposits were identified. The QMA keeps an eye on the two projects that are the most advanced and under development in Northern Québec: Kwyjibo (SOQUEM) and Strange Lake (Torngat Metals).

Québec is rich in critical minerals, which enables us to become a leading player in the global energy transition. In October 2020, the Québec Government adopted a plan to valorise the development and production of critical minerals: Plan Québécois pour la valorisation des minéraux critiques et stratégiques’ (PQVMCS) and later a strategy to develop the battery value chain in Québec.

In doing so, Québec has decided to position its mining sector. It is stimulating the demand for Québec’s critical minerals. Many budget measures were put in place to help the development of mines and processing plants in Québec in that sector.

The province has substantial deposits of rare earths, and the mining industry in Québec has been exploring ways to extract and process these elements. Some key points regarding Québec’s role in the context of rare earths and the push towards electric vehicles and renewable energy include resource potential, supply chain security, economic opportunity, environmental considerations/research, and innovation.

Québec Mining Association greatly advocates for sustainability in the mining sector. Can you discuss how you promote sustainable practices?

The QMA and its members are committed to the Towards Sustainable Mining (TSM) standard. Developed by the Mining Association of Canada (MAC) in 2004, the TSM standard is a globally recognised sustainability programme that supports mining companies in managing key environmental and social risks. Since 2014, the TSM has been a condition of membership for QMA members.

The QMA supports its members in the implementation and monitoring of the protocols. The TSM management team is committed to remaining at the forefront of sustainable management of mining operations.

The initiative applies to all types of mining, including those mining for rare earths and battery metals. It includes nine protocols based on 30 indicators that support transparent and efficient communications with communities of interest and ensure that the main risks associated with mining are managed responsibly. Each year, mining companies must publish performance results for their facilities and state the improvement solutions to be put in place. These protocols are:

Climate Change;

Crisis Management and Communications Planning;

Biodiversity Conservation Management;

Indigenous and Community Relationships;

Prevention of Child and Forced Labour;

Safe, Healthy, and Respectful Workplaces;

Tailings Management;

Water Stewardship; and

Equitable, Diverse, and Inclusive Workplaces.

The TSM is, therefore, a powerful tool to encourage and continuously improve sustainable practices in extracting all types of minerals, including rare earths and battery metals. Most important is that the TSM goes beyond legal and regulatory obligations and that all the results are public.

Are there any new technologies or methods being adopted in Québec to improve mining efficiency for rare earths and battery metals?

Several government aid and funding programmes are available to the mining industry, and even more are available for critical minerals. The sector may thereby improve its exploration techniques, extraction methods and processing technologies in terms of efficiency, environmental footprint reduction and enhanced overall sustainability. Research and development initiatives, supported by industry and government partnerships, can stimulate innovation in mining practices.

The Plan d’Action 2023-2025 pour la mise en œuvre du PQVMCS is one such method. It contains four orientations for the valorisation of rare earth minerals, increasing knowledge and expertise on strategic and critical minerals (SCMs), setting up or optimising integrated value chains in partnership with SCM-producing regions, contributing to the transition to a sustainable economy, and raising awareness, support and promotion.

Each orientation is described in terms of objectives, actions, managers, indicators, and targets. This makes the plan an excellent tool for improving the efficiency of mining for critical minerals, including rare earths and battery minerals.

How are you collaborating with other provinces or countries to advance mining in Québec?

In Canada, all the provincial associations and the two Canadian associations (MAC and PDAC) are part of the Canadian Mineral Industry Federation (CMIF). We meet a few times a year and have the opportunity to exchange ideas on issues affecting our industry, share experiences and discuss the provincial and federal framework.

The QMA, as a TSM partner association, also participates in discussions with other TSM partner associations across the globe. We share experiences and issues to improve TSM and its worldwide expansion.

What are the future plans of the Québec Mining Association?

With its new vision and strategic plan, the QMA is working on new communication tactics to reach the public better. According to a QMA survey of the Québec population, 78% of respondents have a poor understanding of the mining industry.

Based on these findings, the QMA has committed to providing more information and highlighting best practices in the industry, as well as the positive impacts of mining activities on Québec as a whole and on host communities in particular.

With our social and environmental practices as well as our legislative and regulatory framework, Québec can produce minerals and metals with the lowest environmental footprint in the world, and the QMA wants to share that with the public.

The QMA wants to gain the population’s confidence and raise awareness that it is better to mine here in Québec than in other, less responsible jurisdictions.

History shows that mining projects can develop with respect for local populations and the environment. Mining companies wish to remain partners of the communities in which they operate, which is why they favour the reconciliation of land uses and actions are taken daily to adhere to it.

The mining companies active in Québec have committed to the population to do things right and be respectful and responsible. Combined with access to the territory, in compliance with the rules and regulations, Québec is on the right track to remain among the best mining jurisdictions in the world.

Please note, this article will also appear in the seventeenth edition of our quarterly publication.

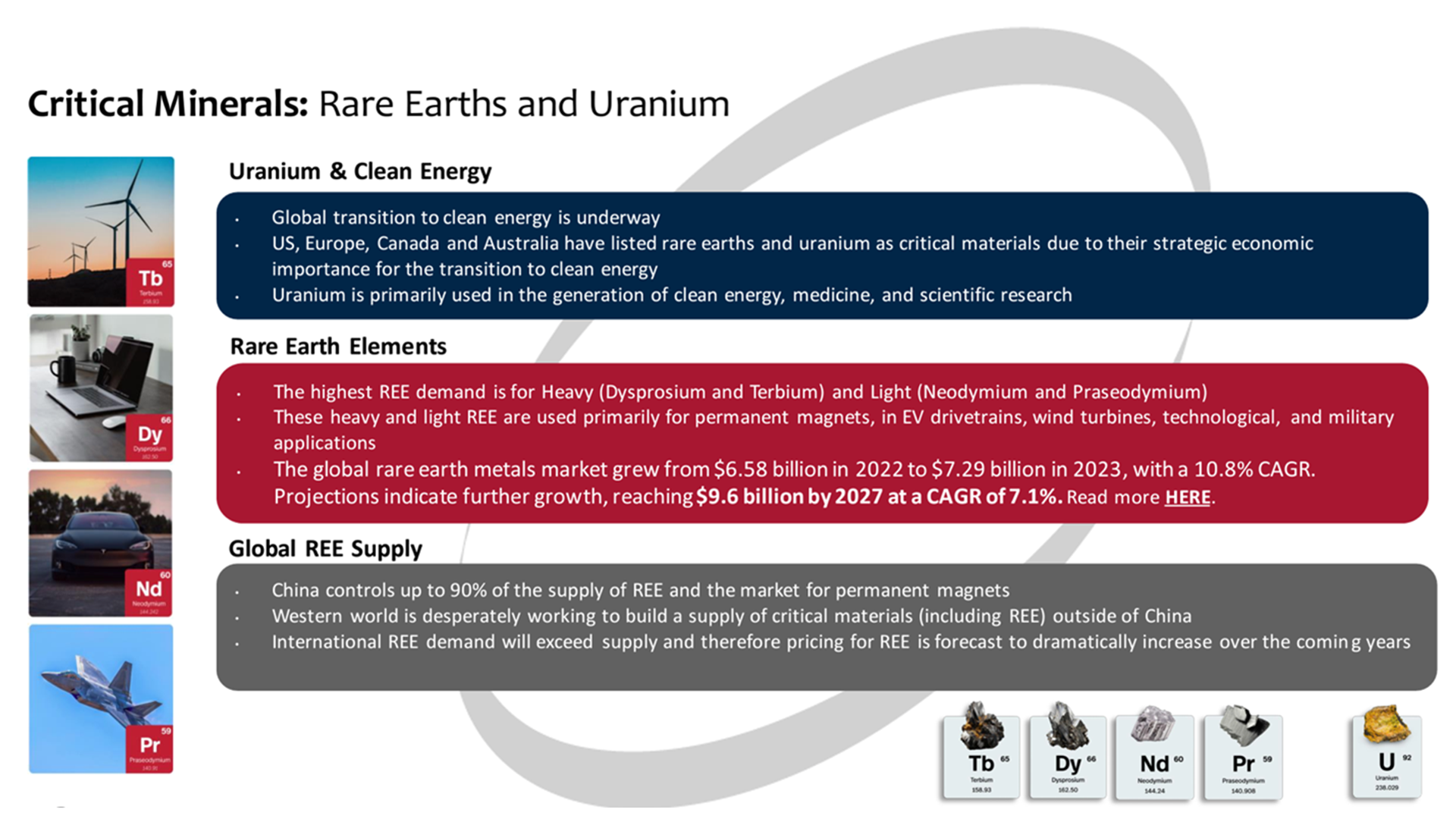

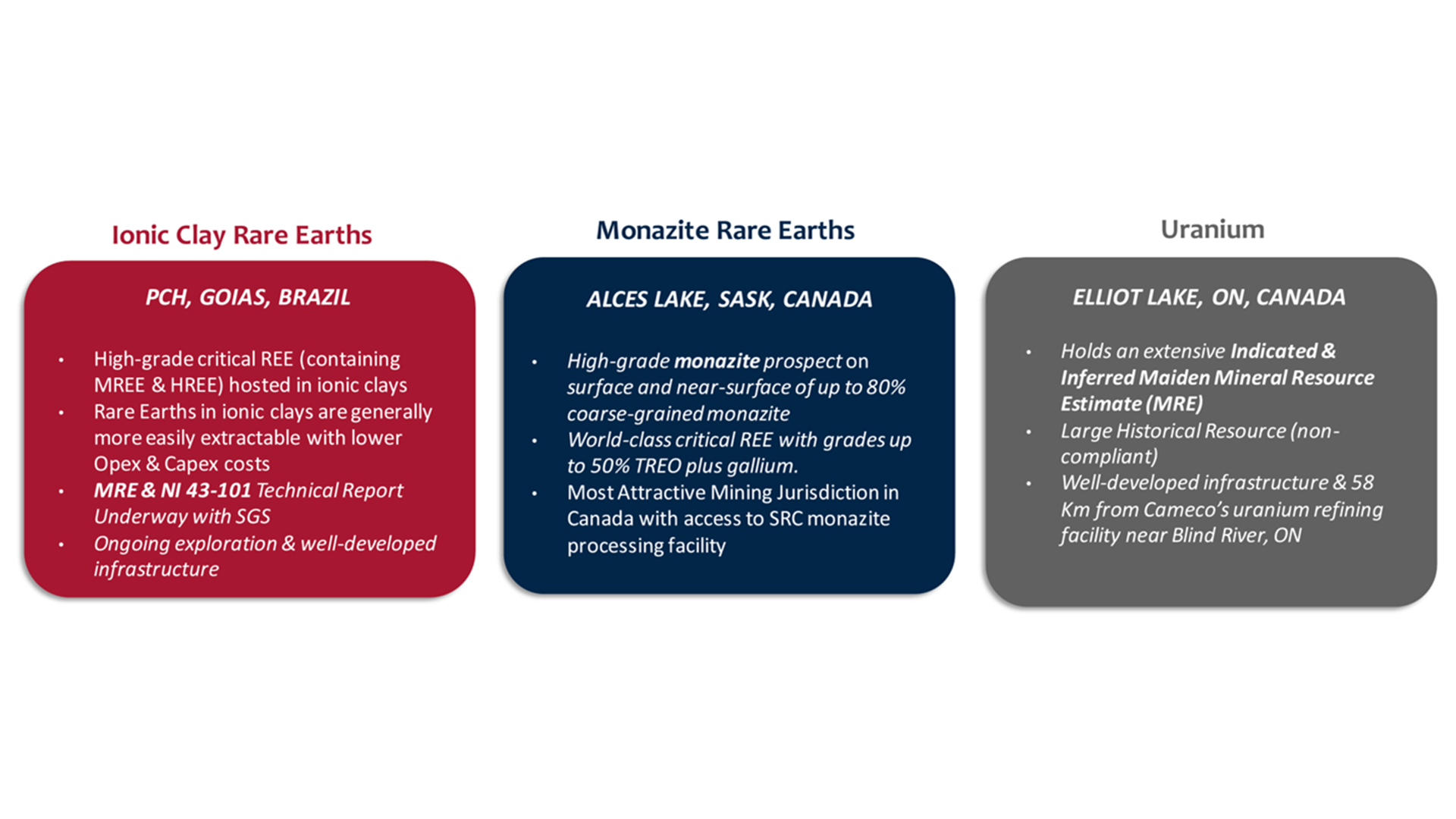

Appia’s portfolio, spanning regions in Canada rich in both REE and uranium, along with the promising PCH Ionic Adsorption Clay REE project in Brazil, has great potential for our clean energy future.

Rare earth elements (REE) remain largely unnoticed in our daily lives. Yet these seventeen minerals, including the priority magnet REE neodymium, praseodymium, dysprosium and terbium, will play a vital role in powering the 21st-century technologies we find in all aspects of our day-to-day lives.

Rare earth bearing minerals are rarely found in the Earth’s crust in significant concentrations, hence their name. REEs possess unique properties that are indispensable in various modern applications, ranging from smartphones and electric vehicles to wind turbines and advanced medical equipment.

Certain rare earth metals, such as terbium and dysprosium, are prized for their heat-adsorbing properties. These magnet REEs play a crucial role in manufacturing powerful magnets vital for electric vehicle motors and wind turbines.

Indeed, these minerals are equally indispensable in our digital world, serving as key components in display screens, compact batteries, and fibre optic cables, driving the technological advancements we benefit from today.

Beyond fuelling technological marvels, rare earth metals are pivotal for achieving a future with renewable energy technologies like solar panels and wind turbines. Their electronic properties optimise the efficiency of these green energy solutions.

The significance of rare earth metals extends beyond practical applications and reaches geopolitical discussions.

With China dominating rare earth metal production, concerns about supply security have arisen globally. Diversifying sources, exploring alternative extraction methods, and fostering international collaboration have become crucial to ensuring a stable and sustainable supply chain.

Uranium’s role in the energy transition

Uranium, often overlooked despite its strategic importance, plays a pivotal role in our world. This is particularly true due to the global renaissance in the nuclear power industry. The IAEA is on record as saying that a ‘doubling’ of nuclear capacity is required by 2050 to achieve climate change goals.

Uranium, derived from uranium oxide (U3O8), is a potent source of clean and efficient energy through controlled nuclear fission, where uranium atoms are split, releasing substantial heat converted into electricity.

Uranium’s significance in achieving climate goals lies in its unparalleled energy density, with a small volume capable of generating millions of times more energy than equivalent amounts of coal or oil. This makes uranium the most efficient fuel for producing massive amounts of electricity, with near-zero CO2 emissions.

In pursuing a clean energy future, uranium will play a crucial role as nations transition away from fossil fuels. As a stable and continuous source of electricity, nuclear power offers an important advantage over weather-dependent solar and wind energy.

The surge in uranium demand and spot pricing reflects the growing acknowledgement of nuclear energy as an essential element in the clean energy mix.

Additionally, the rising demand for nuclear energy, particularly in emerging economies like Asia, is driven by rapid industrialisation and urbanisation, where nuclear power stands out as a reliable and environmentally friendly solution to meet surging energy needs.

Uranium’s remarkable energy properties are key to a cleaner and more sustainable energy future. With the recent upswing in demand and spot pricing reaching a 15-year high in Q4 of 2023, nuclear power is unmistakably gaining traction as a crucial component of our global energy future. View Fig. 2 here.

Company overview

Appia Rare Earths & Uranium Corp. (CSE: API / OTCQX: APAAF / FSE: A010) is a publicly traded mining exploration company that is strategically positioning itself to capitalise on the growing demand for critical minerals, including REE and uranium. In advancing this resource development, Appia can play a significant role in helping to meet the increasing input needs for electric vehicles, wind turbines, and advanced electronics.

Appia’s focus on advancing multiple REE and uranium projects is centred around prolific international mining-friendly regions. These mining districts include Goiás State, Brazil, the Athabasca Basin in Saskatchewan and Northern Ontario, Canada. By targeting these strategic locations, Appia aims to maximise the efficiency and success of its exploration efforts.

Demand for critical minerals will continue to rise. With its focus on strategic projects in leading mining jurisdictions, Appia seeks to unlock shareholder value by developing new REE and uranium resources.

Canadian REE and uranium projects

The Athabasca Basin district in Northern Saskatchewan is globally renowned for its rich uranium deposits, making it one of Canada’s most desirable exploration and mining regions. At the heart of Appia’s Canadian operations are five projects strategically positioned in Saskatchewan’s prolific Athabasca Basin:

Alces Lake, one of the company’s flagship projects, is located in northern Saskatchewan. However, its focus is not on uranium but on high-grade REE hosted in monazite.

In addition to Alces Lake, Appia holds four other prospective properties in Northern Saskatchewan. These other projects (Loranger, Eastside, Otherside, and North Wollaston) focus on early-stage uranium exploration.

Beyond the Athabasca Basin, Appia has diversified its Canadian footprint with its Elliot Lake Uranium Project in Ontario, an area globally known for significant historic uranium mining and milling.

Supporting the project’s development, a major Canadian uranium refinery is situated approximately 60km away, near Blind River. This proximity enhances the project’s potential and opens opportunities for synergies with established mining operations.

Elliot Lake, Ontario

Situated in the Algoma District, Ontario, Canada, Appia holds 100% ownership over the Elliot Lake project. This is a substantial land parcel spanning 13,008 hectares (32,143 acres) and strategically positioned between the prominent cities of Sudbury and Sault Ste. Marie.

The geological strength of this expansive property is underscored by the presence of five known mineralisation zones featuring well-established mineralisation of both REE and uranium.

With substantial mineralised zones and defined NI 43-101 resources for both REE and uranium, Elliot Lake is emerging as a promising long-term source for these critical metals. Appia’s CEO, Tom Drivas, framed the potential of Appia’s uranium assets for investors.

He said: “Appia’s uranium portfolio of both past producing and earlier-stage projects positions the company well to participate in the long-term uranium market appreciation. The company holds a large ground position in Elliot Lake with a historical resource (non-NI 43-101 compliant) totalling approximately 199.2 million lbs. of uranium at a grade of 0.76 lbs. U3O8/ton.”

The NI 43-101 Indicated Mineral Resource for the Teasdale Lake Zone stands at 14,435,000 tons with a grade of 0.554 lbs U3O8/ton and 3.30 lbs TREE/ton, resulting in a total of 7,995,000 lbs U3O8 and 47,689,000 lbs TREE. In the Inferred Mineral Resource category, the Teasdale Lake Zone comprises 42,447,000 tons, grading 0.474 lbs U3O8/ton and 3.14 lbs TREE/ton, totaling 20,115,000 lbs U3O8 and 133,175,000 lbs TREE. Additionally, the Inferred Mineral Resource for the Banana Lake Zone is 30,315,000 tons, with a grade of 0.912 lbs U3O8/ton, resulting in a total of 27,638,000 lbs U3O8. The resources are largely unconstrained along strike and down dip. Refer to the NI 43-101 Mineral Resource Estimate page for qualifying notes regarding the Mineral Resource estimates, and individual element grades supporting the reported TREE results.

The historical resource was not estimated in accordance with definitions and practices established for the estimation of Mineral Resources and Mineral Reserves by the Canadian Institute of Mining and Metallurgy (CIM), is not compliant with Canada’s security rule National Instrument 43-101 (NI 43-101), and unreliable for investment decisions;

Neither Appia nor its Qualified Persons have done sufficient work to classify the historical resource as a current mineral resource under current mineral resource terminology and are not treating the historical resources as current mineral resources; and

Most historical resources were estimated by mining companies active in the Elliot Lake camp using assumptions, methods and practices accepted at the time and based on corroborative mining experience.

Alces Lake, Saskatchewan

With a vast property covering 38,522 hectares (approximately 95,191 acres), the Alces Lake project offers robust exploration opportunities. Situated where the expansive Canadian Shield extends into northern Saskatchewan, Alces Lake offers both scale potential and high grades of REE.

A total of 34,248.29m has been drilled to date, spread across 316 drill holes. This extensive exploration has uncovered new zones of REE mineralisation, including Jesse and Hinge.

To date, exploration results align with the project’s original geological modelling, indicating substantial potential for expansion of mineralisation and resource development. Appia announced the completion of a NI 43-101 technical report in May 2023 to support further exploration.

Besides Alces Lake, the company already holds four high-potential early-stage uranium projects in the prolific Athabasca Basin area: Loranger, North Wollaston, Eastside and Otherside.

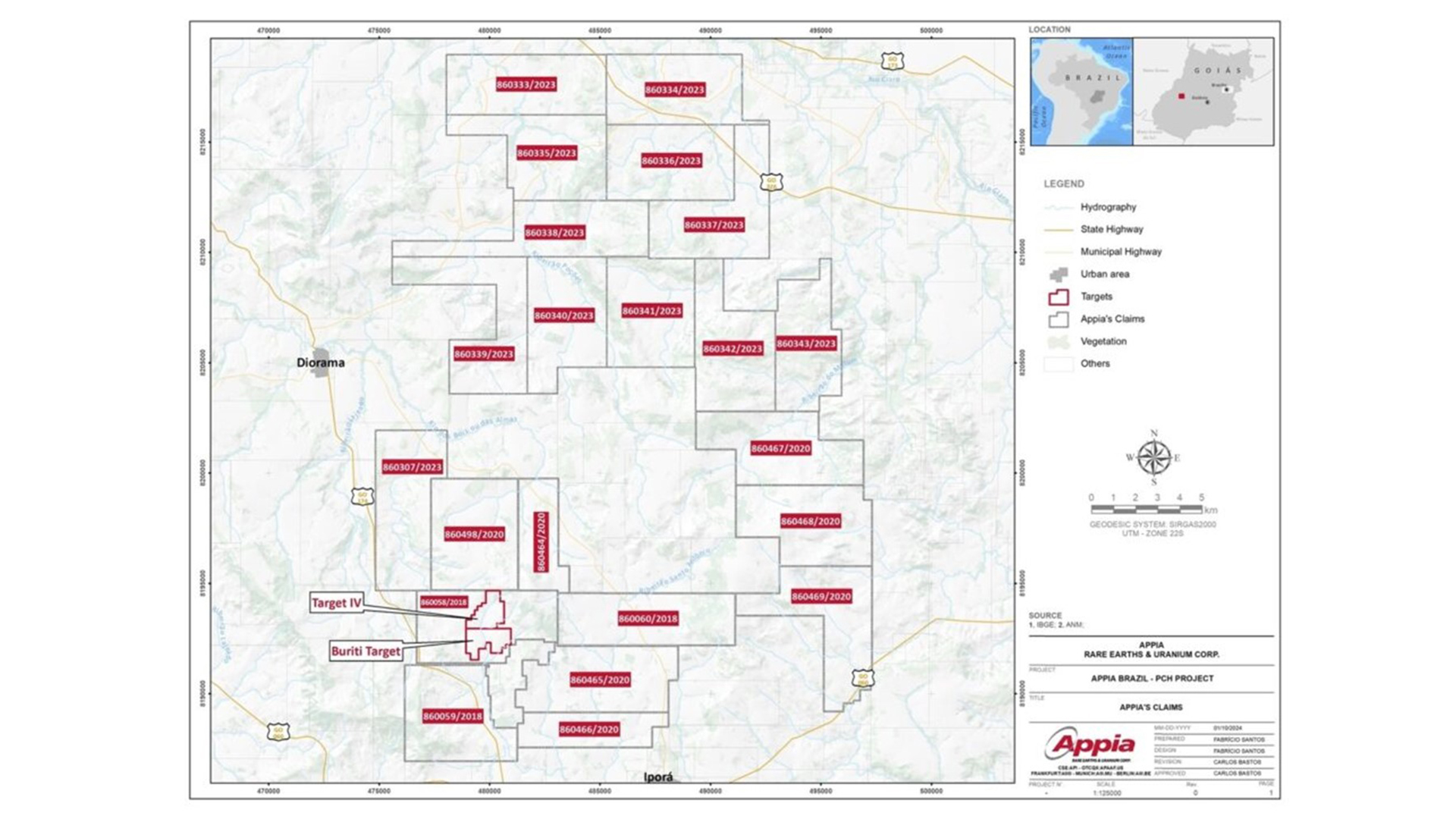

Stephen Burega, President, said: “The expansion of our exploration rights to 40,963.18 hectares (101,222.22 acres) marks a pivotal moment for Appia in Brazil as we build on the momentum achieved through our initial drilling programme at the Target IV and Buriti zones. Our dedicated Brazilian team is eager to explore the untapped potential of the northern corridor, where similar geological and geophysical features have been identified.”

Burega added: “There is huge potential in these new claim blocks as we can draw clear parallels to the favourable geology that hosts the critical rare earth minerals that initially convinced us to enter our agreement on the PCH project. Doubling the size of our overall land package within the prolific alkali province not only reflects our commitment but also strengthens the company’s strategic plans. We aim to develop a series of potential target zones, extending the project focus for the benefit of our valued shareholders.

The headline assay result from this 300-hole drilling programme is a remarkable 24-metre mineralisation zone starting from the surface on drill hole PCH-RC-063, averaging 38,655 ppm or 3.87% Total Rare Earth Oxides (TREO). This includes a higher-grade interval from 10–12m depth, registering an exceptional 92,758 ppm or 9.28% TREO. Click HERE.

PCH Project mineralisation includes significant concentrations of Magnet Rare Earth Oxides, Heavy Rare Earth Oxides, and Light Rare Earth Oxides. This unique discovery extends from the surface and remains open at depth.

These results indicate substantial potential for further expansion of mineralisation at depth, and Appia is currently working with SGS to develop the maiden Mineral Resource Estimate (MRE) on Target IV and Buriti zones of the PCH Project, which will be a crucial part of the NI 43-101 technical report on the PCH project as a whole.

Fig. 3: Appia is committed to advancing multiple rare earths and uranium projects in mining-friendly regions, including Goiás State, Brazil, the Athabasca Basin area in Saskatchewan, Canada and Elliot Lake, Ontario, CanadaFig. 4: Target IV covers 193.28 hectares, and Buriti covers 210.39 hectares of claim 860058/2018, which spans a total area of 1,874.6 hectares

For investors new to REE, Appia’s PCH project discovery is important because mining REE from ionic adsorption clays offers significant benefits, starting with much more efficient exploration.

Unlike traditional REE extraction methods, ionic adsorption clays require less complex and costly processing techniques. This offers additional efficiencies that include streamlined operational procedures, reduced capital costs, and a potentially quicker path to production.

Brazil is a leading mining jurisdiction with a government that has demonstrated a solid commitment to resource development. Government investment and regulatory support play pivotal roles in developing the industry. National strategic initiatives aim to enhance exploration, extraction, and processing capabilities.

Brazil’s national commitment to mining development also extends to many of its state governments. This combined support for project and industry development and its immense resource wealth has made Brazil an increasingly attractive destination for the global mining industry.

With an impressive portfolio spanning regions in Canada rich in both REE and uranium, along with the promising PCH Ionic Adsorption Clay REE project in Brazil, Appia is positioning itself to generate substantial shareholder value in developing meaningful and strategic global assets to help meet the demand for clean energy solutions.

Appia’s future exploration plans run in parallel with what most world experts call for in developing uranium resources as fundamental and crucial in meeting global climate change objectives. Also, seeing the Western world’s need for non-Chinese controlled REE resource development, it has now finally assumed a priority position of strategic importance across all boardrooms and government discussions.

For investors looking to add exposure to these sectors in their portfolio, Appia Rare Earths & Uranium Corp. offers a compelling value proposition.

Please note, this article will also appear in the seventeenth edition of our quarterly publication.