[ad_1]

The importance of critical raw materials is driving increasingly fierce competition between global powers. Olimpia Pilch, Co-founder and Director of the Critical Minerals Association USA, tells us more about one such competition.

Fuelled partially by the pursuit of net zero, and partially by China’s decoupling from the US, critical minerals have become tools of diplomacy in the race to control sensitive sectors. By bolstering domestic security via expanding defence capability, diversifying energy sources, or betting on the cusp of cutting-edge technology, critical minerals play a fundamental role in the geopolitical game of chess.

Monopolised supply: A problem of our own making

China has long had its sights on strategic sectors, and the raw minerals and specialty materials required for many vital technologies. Free markets and the US-backed ascension of China to the World Trade Organization have provided the perfect platform for China to capitalise on the de-industrialisation of the collective West. The global race to offshore and lower costs had chief executives trading the longevity of companies, market share, and propriety information for spectacular and rapid profits. US permanent magnets, semiconductors, and critical minerals industries were all shipped off to China one by one.

China’s lack of compliance with the conditions of its ascent to the WTO went relatively unaddressed for two decades, while quotas and export restrictions became more frequent and targeted at the US market. The industry has long lamented a number of Chinese companies’ methods: Quick and easy credit, loans, and infrastructure deals for raw materials, corporate espionage and IP theft, sabotage of mining operations overseas, market flooding coupled with Chinese share-buying sprees and acquisitions of struggling Western companies, amongst many other accusations of in-country coercion and intimidation of China-based executives.

The golden age of offshoring, however, came crashing down amidst a series of tit-for-tat export restrictions, election meddling, and espionage balloon sagas. By then, the US had drawn, quartered, and sold off its critical minerals midstream industry. Even the infamous Mountain Pass mine, the only rare earth mine in the US, continues to sell offtake to China due to insufficient demand outside of the biggest market, where refining takes place before the US imports ready-made magnets.

Meanwhile, China has banned exports of processing technology to prevent the US or other players from taking its rare earth crown.

Now, the US is facing difficult decisions about protecting its values and interests while managing the effects of short-term vision. However, modern problems require modern solutions, and the US is taking the challenge head-on.

Unlocking domestic resources

The US has since taken a variety of measures to bolster its national, energy, and economic security by incentivising re-industrialisation of the US via the landmark Inflation Reduction Act (IRA), which sent waves across the world. Paired with the Bipartisan Infrastructure Law (BIL), the US critical minerals supply chain has been benefiting from concentrated support from the demand side. The US is taking two approaches, one focusing on energy security, spearheaded by the Department of Energy (DOE), while bolstering national security naturally falls under the U.S. Department of Defense (DOD).

On the defence side, the U.S. DOD has been propping up projects of strategic importance, including the first US nickel refinery hopefuls, Westwin Elements, and Perpetua Resource’s antimony and gold project in Idaho. Through the Defense Production Act Investment (DPAI) programme, the DOD backed Canadian companies Fortune Minerals and Lomiko Metals, focusing on cobalt and graphite, respectively. At the same time, Albemarle and Talon Metals received more than $110m in grants for the domestic production of lithium at Kings Mountain in North Carolina, and nickel at the Tamarack project in Minnesota.

Further, South32’s Hermosa manganese and zinc project in Arizona is the first mining project covered by the FAST-41 programme, for critical infrastructure projects that benefit the nation. FAST-41 was signed into law by President Obama in December 2015, and the FAST Act also created the United States Federal Permitting Improvement Steering Council (FPISC), an independent federal agency composed of 16 members, including 13 federal agencies responsible for environmental reviews and permitting for infrastructure projects. The success of Hermosa has the potential to open the doors for more critical minerals projects to flow through the FAST-41 programme, and cut down the time lag between the discovery of deposits and production.

Several structural issues, however, remain unresolved in unlocking US critical minerals independence. The abolishment of the United States Bureau of Mines in 1996 left US critical minerals affairs unaddressed and floating between several federal agencies and the White House, leading to fragmentation. There is also a visible misalignment between the Federal agenda on critical minerals, particularly concerning China’s monopoly, and individual State approaches to dealing with both the development of critical minerals resources and Chinese investments. States such as Utah and Nevada are leading the charge and have ranked as number one and two, respectively, on the Fraser Institute’s investment attractiveness index for mining.

The outdated Mining Law of 1872 does not reflect the modern realities of critical mineral exploration and extraction, nor does it enable the timely development of projects. It has also faced criticism from activists, non-governmental organisations, and Native American communities for failing to direct mineral exploration towards sites that are perceived as culturally and environmentally appropriate (albeit there is no consensus of where that is), and not promoting early meaningful engagement with communities. Despite mining (collectively and not just for critical minerals) generating a gross output of nearly $702bn in 2023, the industry has been criticised for insufficiently compensating the American taxpayer for extracting on public land.

Strong leadership to undertake the monumental task of updating the mining law to safeguard public interests and remove barriers to responsible and speedy exploitation of America’s critical minerals natural endowment is much needed, especially to unite two opposing sides of the debate under one common goal: a better tomorrow built on American critical minerals for the American people.

Leading the West to critical minerals diversification

The US has taken decisive strides and remains the key driver of supply chain diversification across the globe. Ambitious domestic policy and active investments in critical minerals companies are supplemented by a drive to onshore critical minerals from like-minded jurisdictions. The U.S. International Development Finance Corporation (DFC) has been slow to provide alternative financing options to those typically provided by Chinese companies and state entities such as the Export-Import Bank of China.

However, the DFC now has a growing portfolio of investments in rare earths in South Africa and nickel in Brazil via TechMet. Syrah’s Mozambique graphite project has benefitted from a $150m conditional loan while the Australian company focuses on simultaneously setting up an anode facility in Louisiana. The Export-Import Bank of the United States (US EXIM) has issued a non-binding Letter of Interest to another Australian company, Australian Strategic Materials, to provide a debt funding package of up to $600m (AU$923m) for the construction and execution phase of the rare earths project in New South Wales.

The US-led Minerals Security Partnership (MSP), a collaboration of fourteen countries, has also been providing finance to 15 projects across five continents across lithium, cobalt, nickel, manganese, graphite, rare earth elements, and copper. The announcement of the MSP Forum, aimed at bringing more producer nations to the table, can give the US and its allies another tool to drive diversification and build robust partnerships.

There has also been a concentrated effort to invest in infrastructure that could spur investments and significant development, such as the $2.3bn Lobito Corridor and the Gabon Special Economic Zone, positioning the US as an alternative development and finance partner to China. However, the US has lagged in engaging producer nations across Latin America, Africa, and Central Asia at a political level. Where typically competing interests from China and Russia disadvantage US and Western critical minerals companies. However, the US remains seen as an attractive partner and investor across many producer nations.

Lithium spotlight

Despite electric vehicles being around for over a century, it was a Brit working at American ExxonMobil in the 1970s who propelled lithium-ion batteries forward. Amidst the tribulations of corporate life and soaring oil prices, lithium-ion batteries disappeared into the void before making a strong comeback in the shape of Exxon’s drive to tap into US resources through direct lithium extraction (DLE) in Arkansas. Other notable players include:

• Standard Lithium recently commissioned a commercial-scale DLE plan of significant importance to North America

• Pure Lithium secured significant investment from Saudi Arabia and boasts an all-star cast, from the legendary MIT Professor Donald Sadoway, entrepreneur and inventor Emilie Bodoin, and mining mogul Robert Friedland

• Piedmont Lithium is developing lithium projects across the US, Canada, and Ghana

• Albemarle Corporation is the largest provider of lithium for EV batteries in the world, and

• Piedmont Lithium recently obtained a North Carolina state mining permit and is set to supply Tesla.

There is also a growing junior lithium exploration sector, both home-grown and from neighbouring Canada, propped up by Canadian specialist mining capital, which has witnessed significant erosion over the past decade.

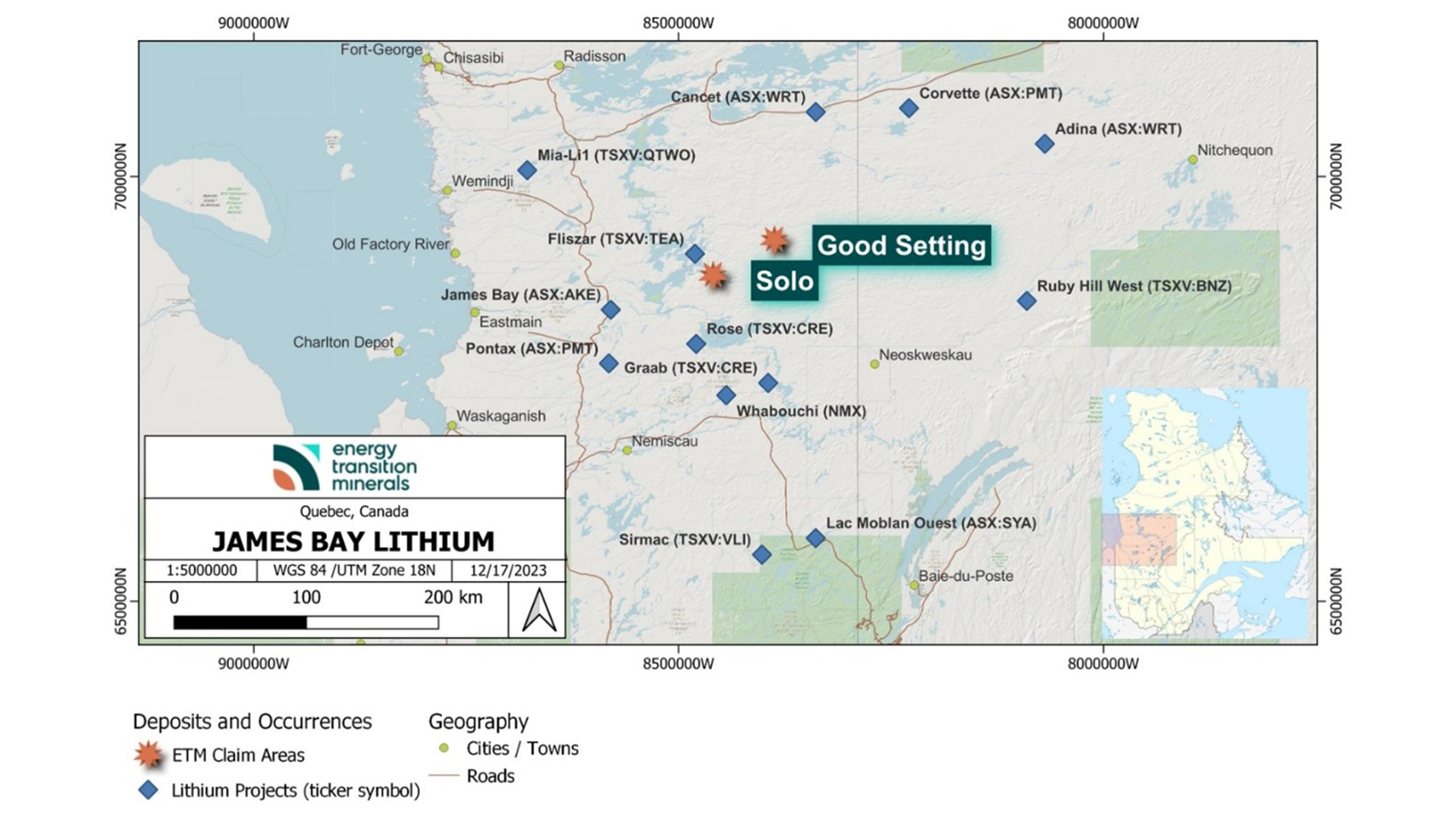

With a bipartisan push to diversify America’s supply chains, the US is truly the land of lithium opportunity. According to the USGS, America has 14 million metric tons of lithium resources, ranking third worldwide after Bolivia. Recent studies place the US as a frontrunner in creating an ex-China lithium supply chain. The McDermitt Caldera, located on the Nevada-Oregon border, could prove to be one of the largest known lithium reserves in the world – the area already hosts the Thacker Pass Lithium Mine, the largest lithium mine in the US. The Australian company, Jindalee Lithium, is anticipating the results of its Pre-Feasibility Study later this year for its signature McDermitt Lithium Project. Meanwhile, Lithium America’s Thacker Pass has received a conditional loan of $2.26bn from the U.S. Department of Energy (DOE) to build an on-site refining facility. Ioneer, who is developing the Rhyolite Ridge lithium project, has also benefitted from DOE backing in the form of a $700m conditional loan to ensure on-site processing of lithium-carbonate.

Researchers have also pinpointed California’s Salton Sea as a lithium hotspot. Controlled Thermal Resources began the construction of their lithium extraction plant and geothermal plant earlier this year at their Hell’s Kitchen lithium brine project located within the Salton Sea geothermal field in Imperial Valley. Whereas, the Tonopah Flats in Nevada have a potential mine life of over 400 years with an average lithium carbonate equivalent production of 30,000 metric tons per annum. Arkansas, Arizona, and California also have significant lithium potential.

Speciality materials and battery manufacturers have also benefitted from DOE’s investments administered by the Office of Manufacturing and Energy Supply Chains, including the likes of American Battery Technology, ICL Specialty Products, Fluor, Solvay, and others, in a bid to create strong mine-to-battery supply chains.

Policy incentives, including the IRA and safeguards such as 25% tariffs on imports of Chinese critical minerals and the Foreign Entity of Concern Rules (FEOC), favourably position US lithium miners to develop projects and for supply chain integration from mine to battery to start taking place. They do, however, have a counter effect of keeping advanced Chinese technology inaccessible to the US in areas such as processing and refining where expertise and scalability know-how have been lost.

If, however, history has taught us anything, it is that necessity is the biggest driver of innovation. The US must innovate, commercialise, and scale up to become globally competitive without the need for government guardrails and safety nets in the future. The US needs to tap into its world-renowned entrepreneurial spirit, take big risks, and reap the rewards in a truly American fashion.

Please note, this article will also appear in the 18th edition of our quarterly publication.

[ad_2]

Source link

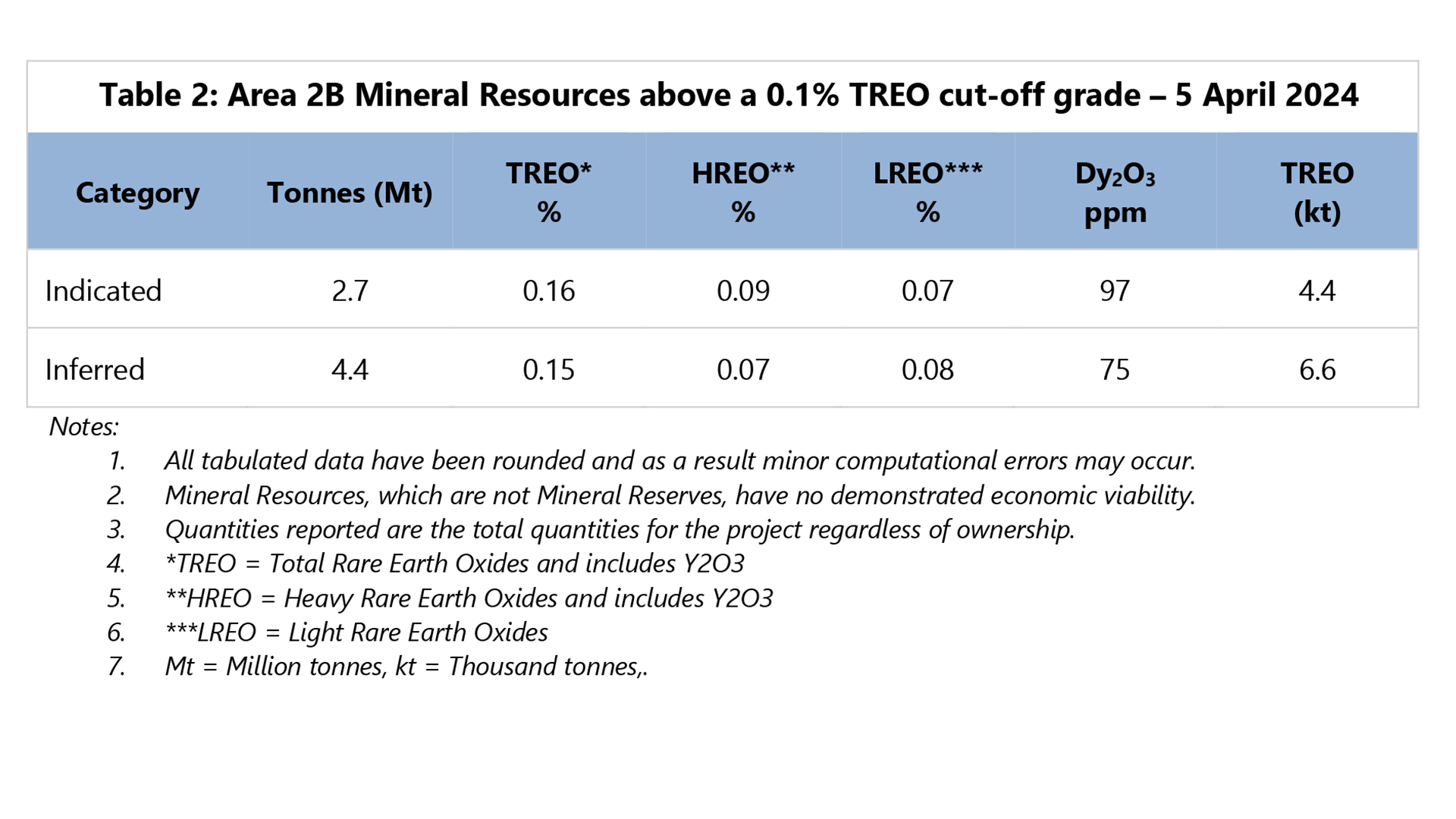

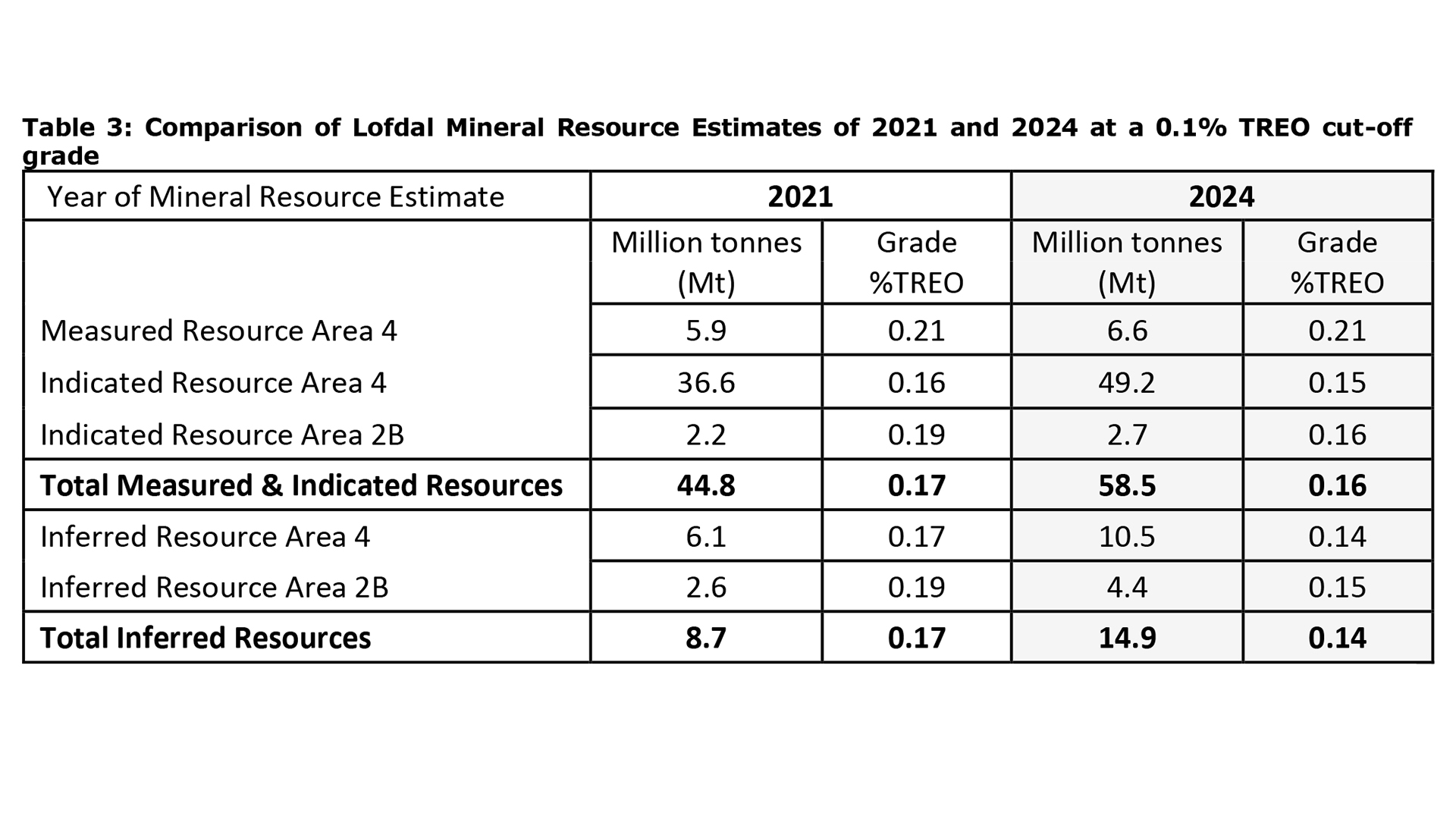

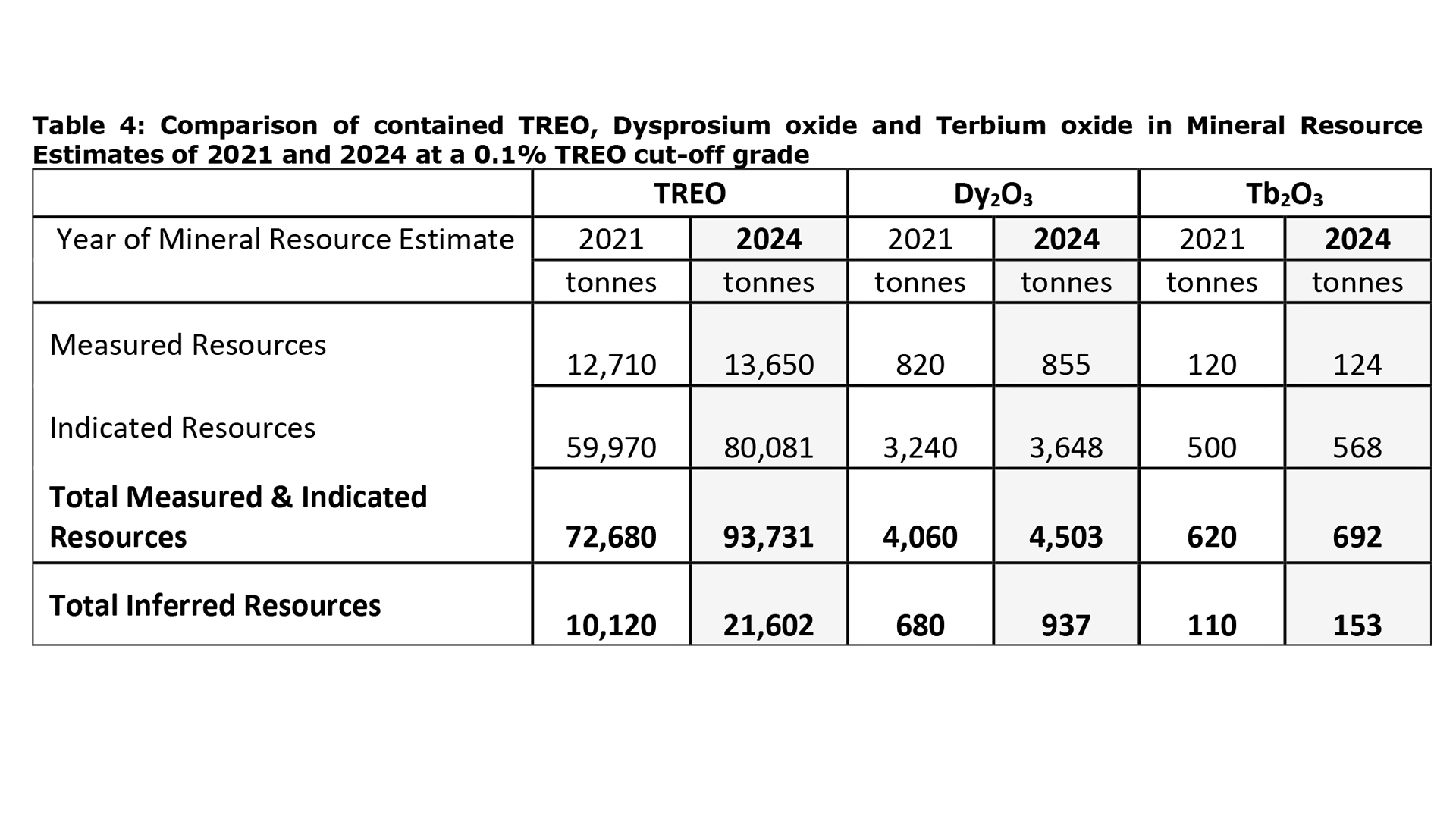

This updated MRE reaffirms the substantial potential of the Lofdal project, positioning it as a key player in the global supply of critical heavy rare earth elements.

This updated MRE reaffirms the substantial potential of the Lofdal project, positioning it as a key player in the global supply of critical heavy rare earth elements.