Just how vital the steel industry is cannot be understated. ResponsibleSteel is working to make sure it fits in with a sustainable future.

The steel industry is vital to all sectors, and yet it remains a heavy carbon-producing industry.

Assistant Editor Matt Brundrett talks with Savannah Hayes, Communications Manager at ResponsibleSteel, to find out more about the work going into changing this.

What is the goal of ResponsibleSteel?

Steel contributes around 10% of the greenhouse gas emissions from the world’s energy system – from the extraction of raw materials to the production of steel products. We urgently need to drive down these emissions if we are to remain in line with the Paris Agreement. But we need to do so in a manner that works for people and the environment, too. That is why ResponsibleSteel’s mission is to be a driving force in the responsible production of net-zero steel across the world.

ResponsibleSteel offers steelmakers a unique and valuable roadmap to improvement and a common language of assessment that their customers, communities, investors, and workforce can all get behind. When a site becomes certified against the ResponsibleSteel International Production Standard, it has undergone a robust assurance process with independent auditors assessing not only how it is working to reduce emissions but also how it is managing its impacts on the local environment and communities, how it treats its workforce, and how it drives improvements in its operations and in its supply chain. We have already certified over 80 sites globally, and we’re just getting started.

What is the current state of the steel industry?

The steel industry is in a state of flux. More and more, the industry is looking to new methods and technologies to enable more sustainable, low-emissions steelmaking. Naturally, steelmakers are looking to scrap to reduce their emissions, and this already contributes to around a third of today’s emissions reductions. But scrap can only take the industry so far. We do not have sufficient scrap supplies to meet demand and will not until the second half of this century. To avoid a commercial ‘race for scrap’ with no net gain for the climate, we need to ensure we are maximising the use of scrap while also incentivising the decarbonisation of primary steel production from iron ore since that is where the lion’s share of emissions are made.

This will require a huge investment in alternative technologies, such as Carbon Capture and Storage and access to green hydrogen, renewable electricity, and potentially biogas, to phase out coal. Steelmakers need the financing to implement these and other high-cost solutions. They are starting to see signals from customers demonstrating that they are prepared to pay the premium on lower-emissions steel. Still, at present, this is being marketed as ‘green’ without a credible, holistic standards framework. That is where ResponsibleSteel comes in.

What does a green steel industry look like?

The first thing I’d say is that the question is misplaced. We want a responsible steel industry, not just a green one. What about the impacts the steel value chain has on biodiversity or water resources? What about the safety and health of the six million people who make up the industry and their families, too? So, what does a responsible steel industry look like? That’s precisely the question ResponsibleSteel set out to answer eight years ago by developing its consensus-driven International Standard with both the industry and civil society. And we have ended up with one that has 13 principles to cover all these aspects.

Most people think of ‘green steel’ as being about climate change. When it comes to carbon emissions, there are different shades of green since the industry won’t get to zero overnight. So how low is good? Everyone has their own thoughts on this, and opinions differ depending on your commercial and geographical perspective, which is why we need a credible, consistent, global approach that really will deliver a green steel industry instead of a few million tonnes of ‘low emissions steel’ here and there. That is what the ResponsibleSteel International Production Standard offers, enabling decision-makers to benchmark the embodied emissions of all steel in the world on a like-for-like basis. Our audit and labelling scheme rewards four different levels of decarbonisation progress towards near zero, and it serves as a global framework against which ‘green steel’ claims can be assessed.

What are the key challenges currently preventing this from happening? What should be done to overcome them? What is ResponsibleSteel doing?

To accelerate the production of near-zero steel, we need financing, policy shifts, and clear demand signals. We run a Finance Working Group to enable the finance sector and the steel industry to come together to discuss how to overcome barriers to capital for decarbonisation. We are also working with our partners to drive demand for near-zero steel through initiatives like SteelZero and the First Movers Coalition’s Near-Zero Steel 2030 Challenge.

Furthermore, amidst an increasing number of emerging initiatives looking for new ways to define near-zero steel, it is imperative that we drive alignment on common definitions and measurement methods to prevent the fragmentation of global trade and to enable effective markets in low-emissions steel. Our work here has led to the launch of the Steel Standards Principles alongside the World Trade Organization at COP28. The principles establish the key foundations of a common framework for climate-related steel standards, including transparent governance, multistakeholder participation, and effectiveness in driving the decarbonisation of the industry globally. Already, over 40 key steel producers, industry associations, standard-setting bodies, international organisations and initiatives have endorsed the principles. And this is only the first step. The true value of the Steel Standards Principles lies in the next ones: co-operation and collaboration between standard setters to smooth out differences in measurement methods and drive consensus on definitions.

What are ResponsibleSteel’s plans for the future? Are there any developments, agreements, etc., that ResponsibleSteel is active in or looking forward to?

ResponsibleSteel is just getting started. We are rolling out our International Production Standard across sites globally – over 80 to date – and following a 12-month test phase of these requirements; we are preparing for the first certified steel. In time, sites will be selling ResponsibleSteel-certified steel that demonstrates progress towards near-zero using an international barometer. We recently updated our requirements for responsible sourcing of input materials and our decarbonisation progress thresholds to ensure our standard incentivises the use of scrap within the bounds of its availability and drives down steel emissions globally.

Later this year, we will launch a new Downstream Chain of Custody Standard, which will be critical in ensuring that users of certified steel make specific, reliable, and, therefore, credible claims in the market.

Please note, this article will also appear in the 18th edition of our quarterly publication.

Arthur Leichthammer, Geoeconomics Policy Fellow at the Jacques Delors Centre, argues that the EU needs a strategic rethink to safeguard its critical raw materials supply as global competition intensifies.

European Commission President von der Leyen assumed office in 2019 with the European Green Deal as her flagship policy, setting out the path for the EU’s clean energy transition.

Within it, she stressed the strategic importance of achieving resilient and diversified supply chains for sustainable raw materials that form the basis of any industrial process.

As the name suggests, critical raw materials (CRMs) – those resources judged to be of high economic importance and exposed to high supply risk – are of special importance. CRMs are key for strategic sectors of clean technologies, digital, space, and defence utilisation and, as such, fundamental to delivering the ambitions of the Green Deal’s net-zero targets.

They make electronics, motors, generators, and batteries. For instance, rare earth elements are essential for the manufacturing of wind turbines, solar panels, and electronic devices.

At the same time, lithium and cobalt are crucial for battery production, powering electric vehicles and energy storage systems.

CRM and the green transition

As the green transition progresses, the demand for CRMs will radically increase. For instance, the EU’s lithium demand is expected to increase twelve-fold by 2030.

As it stands, the EU’s current CRM supply will not suffice to cover this surge. The EU is not alone in its decarbonisation efforts, as economies worldwide have committed to net-zero targets.

The International Energy Agency (IEA) estimates that the global energy sector’s need for critical minerals could quadruple by 2040. To satisfy this increased demand, the IEA estimates that by 2030, 388 new mining sites will have to be opened.

As demand is projected to outgrow supply growth, global competition is becoming increasingly fierce, and reliable CRM supply chains are emerging as cornerstones of the new renewable industrial ecosystem.

The European Union does not produce or refine nearly the volume of CRMs it requires for its industrial production. As such, the EU heavily relies on imports. More problematically, it relies on a handful of countries for key CRMs, both in production and refinement. This exposes it to supply disruptions and price volatility, amplifying vulnerabilities in critical sectors.

First and foremost, the dependency on China has emerged as a key concern for the EU. Not only is China a key producer in a range of CRMs, but perhaps more importantly, it has established itself as the primary centre for the refinement of most key minerals, processing 40% copper, 60% lithium, 70% cobalt, and close to 100% of the graphite used worldwide. The EU, for instance, imports close to 100% of its rare earths.

The great power competition between the US and China and the ensuing trade war is likely to accelerate the politicisation of critical raw materials.

As the West attempts to decrease China’s strategic stranglehold on CRM value chains, China is becoming increasingly assertive in both defending and utilising its strategic position in the CRM value chain.

In 2020, China became the country with the most restrictions on mineral exports.

In 2023 alone, China introduced rare-earth export restrictions for several types of graphite and doubled down with a new trade ban on rare-earth production equipment. Both restrictions were implemented, citing national economic security interests.

This follows the earlier export permit requirement for gallium and germanium, which were required to make chips last August, in a retaliatory move following the Dutch trade restrictions on advanced semiconductor equipment.

Fig 1: The concentration of the EU’s critical raw materials imports (Figure adapted from: European Commission (2020) Action Plan on Critical Raw Materials)

The EU’s first stab at reducing its dependencies

While the EU has long tried to secure reliable CRM supplies, adopting its ‘raw materials initiative’ in 2008, the described geopolitical developments, the supply chain disruptions of the Covid pandemic, and Russia’s invasion of Ukraine have propelled the issue of energy and supply chain resilience forward with force.

Aiming to diversify and foster new supply chains and reduce critical chokeholds of CRMs, the EU put forward its Critical Raw Materials Act (CRMA), finalising the legislative process in March 2024. The legislative framework aims to enhance the EU’s CRM supply via increased domestic capacities and international agreements, seeks to improve the EU’s supply chain monitoring, and improve the sustainability of CRM sourcing.

The CRMA sets out three key milestones for the EU’s domestic capacities by 2030:

10% of annual consumption derived from locally extracted materials

40% processed in the EU

25% derived from recycled materials.

Key to enhancing the EU’s domestic production, processing, and recycling capacities is a Strategic Projects framework that grants accelerated permitting procedures and is supposed to ease access to financial support.

Under the framework, firms apply for Strategic Project designation from a Critical Raw Material Board, which is hosted and funded by the Commission.

Once granted, projects receive European public interest status and streamlined planning and development processes. Authorities must decide on resource extraction projects within 24 months and processing or recycling projects within 12 months, with limited contingency time for complex applications.

It further foresees that financial risks are shared between project promoters, member states, and public financial institutions, involving partners like the European Investment Bank Group to provide recommendations on project preparation and financial assistance.

Furthermore, the Act empowers the EU to set environmental standards and screening criteria for raw materials mined, refined, and recycled within the European Union.

The CRMA also posits that a maximum of 65% of a strategic raw material at any relevant stage of processing should originate from a single third country. To enhance such reshoring efforts and reduce overly concentrated dependencies on single states, DG GROW is setting up a panel which, in co-ordination with the member states, will attempt to build on current raw materials partnerships and facilitate infrastructure projects.

Already having exempted the vast majority of CRMs from tariffs via its expansive network of free trade agreements and WTO provisions, strategic partnerships are becoming crucial for the EU to secure additional CRM supplies from trading partners.

Big ambitions – wrong tools

The new legislation provides a much-needed move to up the ante for the EU to address its dependencies.

However, it is likely to fall short of its ambitions for two reasons.

First, the predominant focus on accelerating permitting processes is unlikely to increase the speed of mining investments significantly. The exploration and construction phases of mining projects take several years, with the average mine taking around 15 years from exploration to completion.

So, even if the Act succeeds in chipping off a couple of months in the process by cutting bureaucratic red tape, it will take a long time for European mining projects to reduce European dependencies in a meaningful way.

Second, the Act lacks the financial power of comparable programmes, such as the US Inflation Reduction Act, which allocated over $8.5bn for CRM projects, or the significant financial means available to Chinese state-owned enterprises.

CRM projects are characterised by their need for hefty investments over extended periods and large downside risks regarding permitting and social and environmental risks. On the other hand, CRMs are subject to high price volatility, as seen in the collapse in lithium prices over the last ten months, increasing investment uncertainty.

While the CRMA foresees provisions for firms to lock in prices at which they can sell their resources, it is unclear how this would look in detail and how it would be financed. Without greater financial reassurances, firms are likely to continue their reluctance to make the required investments.

Further, the Act misses out on generating new incentives for additional incentives to crowd in private risk capital, for example, via tax credits.

Amidst the inability to pledge significant funds on a European level, it is left to national capitals to generate investments towards the long-term supply of the needed materials.

Germany, France, and Italy all pledged national financial resources via dedicated funds, Germany and Italy committing one billion each and France two billion euros. In the summer of 2023, they also created a working group to co-ordinate better future possibilities to source critical raw materials collectively. This has the potential to foster projects akin to the Important Projects of Common European Interest (IPCEIs), which allows multiple member states to channel state aid into technology projects of common European interest.

A national approach, however, risks underinvestment for member states with limited fiscal headspace. The production of CRMs is a European public good, supporting the EU’s economy and its resilience.

To achieve the ambitious targets set out in the CRMA and to generate sufficient production capacities, the development of CRM value chains across the EU must be strengthened.

The next Commission needs a strategic rethink on critical raw materials

To turn the ambitious political ambitions of the CRMA into actionable policy, the EU must step up financing. Having made European Investment Bank financing eligible for all steps of the CRM value chain in July 2023 is an important first step. The EU taxonomy, as of now, only includes the recycling of critical raw materials.

Adding mining and refining under the condition of high environmental standards could help generate private investment.

However, without additional public financial support in the form of equity and guarantee support that could underwrite greater investment, it is unlikely to channel greater financial resources to CRM projects.

More importantly, even if significant financial resources could be leveraged to support domestic extraction, it will realistically only make a small contribution to enhanced resilience.

A reliable import strategy from a diversified pool of international partners will continue to be critical in satisfying European demand. As such, the next Commission should focus on four things.

First, it will be essential to pursue strategies according to specific prioritisation according to individual CRMs. What is needed is a detailed analysis of what materials should be domestically sourced, for which CRMs international partnerships can be developed, and for which the EU can build a diversified supply network.

Indiscriminately pursuing the EU’s significant involvement in all parts of the value chain for all CRMs will not be possible due to capacity restrictions, long lead times, and insufficient financial backing.

Second, in the next legislative cycle, EU instruments should be equipped with enough financial prowess to accelerate research and development in processing and recycling facilities with a focus on sustainable practices. To that end, the EU should develop available funding instruments.

Horizon Europe, for example, facilitates early-stage financing to develop sustainable mining and CRM substitution. Leveraging additional financial means should be used to support the development of low-carbon technological efforts beyond those initial investment needs and allow such ventures to scale.

Third, pursuing more diversified CRM partnerships and co-operation agreements will be crucial. The EU has been busy signing agreements with Canada, the DRC, and Zambia and committed to establishing future ones, as last seen in the joint statement with Australia on energy cooperation in early April 2024.

Following up on initial ideas of forming an international ‘Critical Raw Materials Club’, the EU joined the Minerals Security Partnership (MSP), initiated by the US and which includes partners such as South Korea and the UK. In April 2024, the MSP members alongside Kazakhstan, Namibia, Ukraine, and Uzbekistan announced the launch of the MSP Forum, pledging greater co-operation regarding CRMs.

The Forum sets out a project group aimed at supporting the implementation of CRM projects and policy dialogue to enhance the regulatory framework for sustainable sourcing projects.

However, the EU is playing catch-up. China has been developing its CRM network with significant investments for the past two decades, firmly establishing Chinese companies throughout supply and value chains. This has led to substantial control over upstream activities, including mining and primary smelting and refining processes.

The EU can make up for lost time by offering more attractive partnership conditions. Mineral-rich countries have increasingly been affirmative about gaining a larger share of the value chain within their economies.

Since 2022, more than a dozen African countries have imposed export restrictions or bans on CRMs, while over the last decade global export restrictions have quintupled.

The EU should thus convince third states of increased co-operation via expansive co-investment with a focus on increasing upstream activities and supporting third states with advanced mineral processing technologies, developed via concerted R&D efforts, and targeting those CRMs the EU has limited potential to develop domestically.

The extraction and processing of CRMs often entail significant environmental and social impacts. There have been widespread reports of mines across the globe in which both human rights and environmental standards have been disregarded. With the newly agreed Corporate Sustainability Due Diligence Directive (CSDDD) that introduces comprehensive human rights and environmental due diligence obligations throughout value chains or the Carbon Border Adjustment Mechanism (CBAM), facilitating sustainable technology and practices will not only underline the EU’s global climate agenda and offer third states additional incentives to pursue partnerships with the EU.

It will be legally imperative and costly to ignore.

Fourth, the next Commission should attempt to influence corporate supply behaviour, something the CRMA omits. Private European firms currently underinvest in supply chain resilience and do not yet see diversification as a priority. The EU should build on the mechanism introduced in its Net-Zero Industry Act, which incentivised member states to recognise non-price considerations, making subsidies reliant on diversification or placing a larger emphasis on resilience criteria for public procurement scoring for CRM projects.

Securing reliable and secure critical raw material supply chains will be a decisive factor in determining Europe’s industrial future. As European capitals increasingly recognise the importance of CRMs, the Critical Raw Materials Act constitutes an important step towards remedying the unfolding supply challenges.

However, as it stands, it is insufficient. Following June’s European election, the newly constituted Commission will have to overcome the member states current reluctance to pool greater financial means on a European level, which is fundamental to achieving greater domestic production and offering attractive and sustainable international partnerships.

Please note, this article will also appear in the 18th edition of our quarterly publication.

OFWAT’s Innovation Fund outlines its innovative approaches to tackle water pollution in the UK.

Good-quality water is essential for humans and their environment. In the UK, every individual uses about 140L of water every day. While our need for water remains steady, our other activities are seriously affecting the quality of this essential resource.

In the UK, the main causes of water pollution include industrial activities (releasing harmful chemicals and pollutants into water bodies), agricultural practices (carrying pesticides, fertilisers, and animal waste), and urban runoff (including sewage). This increased contamination poses a serious threat to essential natural water sources.

Water pollution has wide-ranging impacts on the environment and human health. Ecosystems suffer from decreased biodiversity and habitat destruction due to pollutants and disrupted food chains. Polluted water sources pose risks to people using the water for leisure, causing gastrointestinal illnesses and other health issues.

Over the past two decades, we’ve seen some improvement in the quality of water in our rivers¹ and coastal areas – and in the biodiversity of some of the wildlife they support.² There are, however, also too many incidents of pollution. And a strong desire from customers and other water users that more is done to protect our rivers, inland and coastal waters. So, there is still significant work ahead of us to address these challenges and ensure further improvements in water quality.

It is, therefore, critical that we work towards a more sustainable water sector and take advantage of technological and innovation advances to do this.

Innovative approaches to tackling sludge

Across the UK and Europe, there is a growing realisation that sludge – a treated combination of solid matter and dead bacteria left over from the treatment process of sewage – poses environmental challenges. It contains microplastics, metals and PFAS (indestructible chemical compounds, also known as ‘forever chemicals’), which can enter the soil and waterways.

The Ofwat Innovation Fund’s most recent innovation competition, Water Breakthrough Challenge 4, was a £40m competition that recognised 17 winners with the potential to deliver wide-scale, transformational change benefitting customers, society and the environment. Among these winners were a number of innovations seeking to better manage and prevent treated sludge as a possible pollutant.

This included the Sewage Sludge Gasification project from Yorkshire Water, which looks to offer an alternative to recycling sludge to land.

The project will use the Advanced Thermal Conversion gasification process to convert treated sewage sludge into usable products such as biochar, vitrified ash ‘stones’, and a hydrogen-rich synthesis gas (syngas). By operating at a high temperature, the process aims to destroy other contaminants, including forever chemicals, including PFAS and microplastics, and ultimately reduce the risk of water pollution.

An added bonus is that everything produced by the gasification can be reused. The biochar, which resembles small pieces of charcoal, will be tested to treat wastewater as an additive in brick manufacturing and as a soil improver to increase water and nutrient retention. As it doesn’t readily decompose, it’s also a vehicle for sequestering carbon in soil — though it must be properly managed to ensure soil ph levels are not negatively impacted.

The vitrified ash ‘stones’ could be used as aggregate in the construction industry to reduce the embodied carbon footprint of concrete. The syngas – a blend of hydrogen, carbon monoxide, carbon dioxide and methane – can be used to produce green electricity, along with other high-value products.

It is clear that as well as helping reduce pollution, innovative approaches to sludge management can benefit a circular economy and encourage a more sustainable society through the provision of outputs such as green electricity.

Another winner from the competition has been funded to explore a similar but different treated sludge transformation process, in this case via pyrolysis. This high-temperature process doesn’t use oxygen but seeks to recycle treated sludge for similar uses – ultimately reducing the need for treated sludge to be spread.

A third project will look into further uses for the biochar that can be produced from this process.

Tech-led approaches to public awareness and education

Although much of the responsibility for pollution management sits with organisations and governing bodies – including the agricultural industry, urban planning as well as water companies themselves — public awareness and education can play a crucial role in reducing water pollution.

The Ofwat Innovation Fund has supported a number of water companies in their ambitions to achieve better customer education around water pollution.

In the latest competition, Severn Trent was awarded £1.8m to pilot an exciting scheme, in partnership with Nectar and behaviour experts, that aims to incentivise customers to reduce their energy consumption through smart meter gamification. The initiative will work by awarding points for water-efficient behaviour, ultimately driving lower water use and reduced energy bills for the customer.

Similarly, Ofwat had previously awarded the citizen science initiative, The Big River Watch, £7m as part of an earlier round of the competition. The project, from a consortium of water companies and partners, including United Utilities, Severn Trent and The Rivers Trust, has led to the creation of an app-based survey that encourages individuals to monitor the local health of their rivers and comment on visible pollution levels, wildlife (indicating health) and their experience of the river.

Innovative educational initiatives, such as citizen science, will be critical in getting the public to engage in monitoring and improving water quality, including awareness of pollution and its impact.

Green infrastructure to reduce and counter water pollution

Some issues related to water pollution can be improved through customer education. Still, much of it needs national-level processes to drive change, which is why Ofwat works so closely with innovation teams at water companies. Through initiatives to address the factors behind pollution, we can begin to instigate the structural changes needed to achieve healthier bodies of water.

Some of these are literally structure-based changes. Over time, built-up areas have become increasingly water-resistant, with paved, non-permeable surfaces leading to increased run-off. This, combined with a changing climate and increased risk of extreme weather such as storms and flooding, can lead to the overuse of sewage overflows.

Introducing green infrastructure to urban environments, such as green roofs and permeable pavements, can absorb and slow down rainwater runoff, mitigating flooding.

Sustainable Drainage Systems (suds) replicate natural drainage processes through features such as ponds and infiltration basins. These systems manage surface water runoff, diminishing flood risk and enhancing water quality while fostering biodiversity.

Suds iq, a national suds collaboration and evaluation platform led by Southern Water and awarded funding as a winner of Water Breakthrough 4, seeks to create a nationwide online platform for Sustainable Drainage Systems (suds) collaboration aimed at enhancing collective understanding of suds functionality and benefits.

This platform will streamline partnership efforts and promote the adoption of environmentally friendly drainage solutions, expediting efficiency and implementation.

Another innovative project that has been awarded funding is developing a market-based approach to deliver suds. For example, the risk of flooding in London due to heavy rain is on the rise. This winning initiative encourages utility companies to fill some of the 165,000 holes they dig in London annually with ‘sustainable drainage systems,’ such as rain gardens, helping to alleviate pressure on drains caused by rainwater and contribute to making the city greener.

A pollutant-free future

It’s exciting to see our Innovation Fund driving so many of the crucial changes needed to reduce pollution and limit the effects of unavoidable pollutants.

Although there is still work to be done, we hope that these projects can pave the way for a cleaner, greener water sector of the future, powered by innovations that benefit society, the environment and customers.

While lithium-ion batteries hold great potential for the future of sustainable energy, a few issues still need to be addressed. Xerion Advanced Battery Corp. is at the forefront of developing solutions to these problems.

As the world races toward decarbonisation goals aimed at mitigating the impacts of climate change, batteries have taken a central role in the shift away from fossil fuel reliance. Lithium-ion batteries specifically have emerged as a key innovation in the clean energy transition since their inception over 30 years ago. From electric vehicles (EVs) to renewable energy storage systems, these advanced batteries are the enabling technology driving the shift away from fossil fuels. However, while current lithium-ion battery technologies offer many benefits, there remains a long way to go in addressing the shortcomings of these technologies.

Lithium-ion batteries have become the technology of choice for a wide range of applications due to their exceptional energy density, long cycle life, and low self-discharge rate. These advantages have made them the go-to power source for consumer electronics, power tools, and, most importantly, EVs and stationary energy storage systems.

The transportation sector, responsible for a significant portion of global greenhouse gas emissions, is undergoing a seismic shift towards electrification. Major automakers have announced ambitious plans to phase out internal combustion engines in favour of EVs, driven by increasingly stringent emissions regulations and consumer demand for more sustainable transportation options.

Similarly, integrating renewable energy sources, such as solar and wind, into the electricity grid has created an urgent need for large-scale energy storage solutions. Lithium-ion batteries store excess renewable energy when production exceeds demand and release it back into the grid when needed, ensuring a reliable and sustainable electricity supply.

Unfortunately, despite the great promise that lithium-ion batteries offer for advancing the transition to clean, renewable energy, technologies on the market today possess significant drawbacks. Namely, the technologies and configurations dominating today’s market are expensive and reliant on unstable supply chains. Beyond the costs, there are opportunities for improvement in both the performance and safety of Li-ion batteries.

Xerion – Building a better lithium-ion battery

Further innovations are required to harness the true potential of lithium-ion batteries as a driver of the energy transition. At Xerion, we are doing just that. Xerion has spent more than a decade flying under the radar, quietly developing a high-performance, low-cost lithium-ion battery technology platform that now promises to not only revolutionise the battery and short-term energy storage sector landscape but also to propel the electrification of the global economy forward. Xerion’s revolutionary manufacturing platform is founded upon two patented core technologies – DirectPlate™, an innovative refining and deposition technique, and StructurePore™, a novel battery electrode architecture.

Xerion’s DirectPlate™ manufacturing process leverages a molten salt electroplating process to eliminate many of the steps and materials required in traditional lithium-ion battery manufacturing processes. The company’s novel StructurePore™ nanostructured metal foam electrode architecture dramatically reduces resistance, allowing lithium ions to move rapidly through the battery. This architecture also minimises the potential for thermal runway by reducing heat generated by the battery during failure events, granting significant safety advantages over traditional lithium-ion batteries.

Combined, these core technologies deliver a dramatically lower-cost lithium-ion battery with higher energy density, more power, faster charge, longer life, improved safety, and 40% lower carbon emissions than conventional battery manufacturing.

Optimising battery manufacturing sustainability

An under-discussed element of the ever-growing demand for lithium-ion batteries is ensuring that procuring critical battery materials, such as lithium and cobalt, remains sustainable. Demand for these materials is far outstripping supply, as the International Energy Agency (IEA) reported that the global demand for lithium tripled between 2017 and 2022, and it is projected to double again by 2030. With that increased demand comes increasing importance to optimise sustainability.

Xerion’s cutting-edge technology is elevating sustainability to new frontiers. The company’s DirectPlate™ manufacturing process has yielded a critical innovation as it pertains to the environmental impact of battery supply chains. This revolutionary process extracts lithium directly from geothermal brines, which exist in abundance in regions such as California’s Salton Sea and South America’s Lithium Triangle. This novel ceramic redox membrane technology allows for low-cost, highly efficient extraction of lithium from geothermal brines with minimal impact on the surrounding environment. While the concept of extracting lithium from geothermal brines, in a process called direct lithium extraction (DLE), is currently utilised, existing methods have been plagued by poor lithium selectivity, material instability, and high cost.

In contrast, Xerion’s technology is exceptionally resistant to the temperature and chemistry of geothermal brines, providing the required lithium selectivity and durability for practical application. The company has demonstrated this technology is capable of efficiently extracting lithium from raw geothermal brines with low lithium concentrations to produce high-quality lithium hydroxide. This lithium hydroxide can be used directly as a battery feedstock to synthesise cathodes in a single step using Xerion’s DirectPlate™ molten salt electroplating process, converted to a lithium metal anode for use in solid-state batteries, or as feedstock for the current conventional slurry cast cathode production process.

Notably, Xerion’s DirectPlate™ process can also use less pure, 100% domestically sourced battery precursors and can be adapted to recycle end-of-life batteries, allowing for increased circularity and waste reduction within the battery supply chain.

Strengthening domestic supply chains

As the demand for lithium-ion batteries continues to surge, another critical challenge emerges: Establishing a robust and secure domestic battery supply chain. The production of lithium-ion batteries involves a complex global supply chain, and the United States is currently heavily dependent on international markets for the sourcing of lithium, resulting in high costs, supply chain challenges, and national security concerns. Today, Australia, Chile, China, and Argentina produce over 90% of the world’s lithium, while the vast majority of lithium-ion batteries – roughly 77% of global supply – are produced in China.

To address these challenges, the United States must prioritise the development of a domestic battery supply chain, from raw material sourcing to advanced manufacturing capabilities. Xerion is deeply committed to leading the charge on this front and passionately believes that its technology offers a significant opportunity to make strides toward that goal.

In sum, lithium-ion batteries are a valuable tool for electrifying global economies as we transition to renewable energy, but we cannot remain satisfied with the status quo of today’s technologies. Continued innovation is an absolute requirement moving forward, and those innovations must be focused on improving performance and cost, securing supply chains, and reducing environmental impact. Xerion is committed to these ideals.

Please note, this article will also appear in the 18th edition of our quarterly publication.

Making agricultural trade policies more sustainable calls for an integrated, systemic, multi-method approach covering multiple dimensions of sustainability.

Having played a key role in providing food security and diversifying diets, global agricultural trade has also generated negative impacts on environmental sustainability, social well-being, and economic viability in global agri-food value chains.

The EU Horizon2020 project Making Agricultural Trade Sustainable (MATS) identifies some of these impacts and showcases an innovative approach to identify leverage points for sustainable transformation.

The MATS project responds to the need for agricultural trade policy analysis that manages complex interrelations between natural, social, and economic systems from local to global level.

In so doing, the project outputs include an integrated multi-method approach for policy analysis, including 15 case studies, leading to a set of policy recommendations and transition pathways towards more sustainable agricultural trade policies.

Focusing on governance, design, and implementation improvements at EU, African, and global levels, this approach transcends sustainable agricultural trade and is applicable to other sectors and contexts.

Furthermore, integrating environmental and social externalities into economic analysis, this approach holds transformative potential for policy evaluation and impact assessments in the fields of agricultural trade and sustainable development.

Finally, MATS analysis identifies and strengthens the links between trade policies and sustainable investments to unlock the transformative potential in global agri-food value chains. Building upon these links, MATS hopes to contribute to drafting future policies that foster the positive and mitigate the negative impacts of trade on sustainable development.

The MATS project runs until the end of 2024. Here, we present the key project features and discuss the lessons learned so far towards enhanced tools for policy evaluation and for making agricultural trade more sustainable.

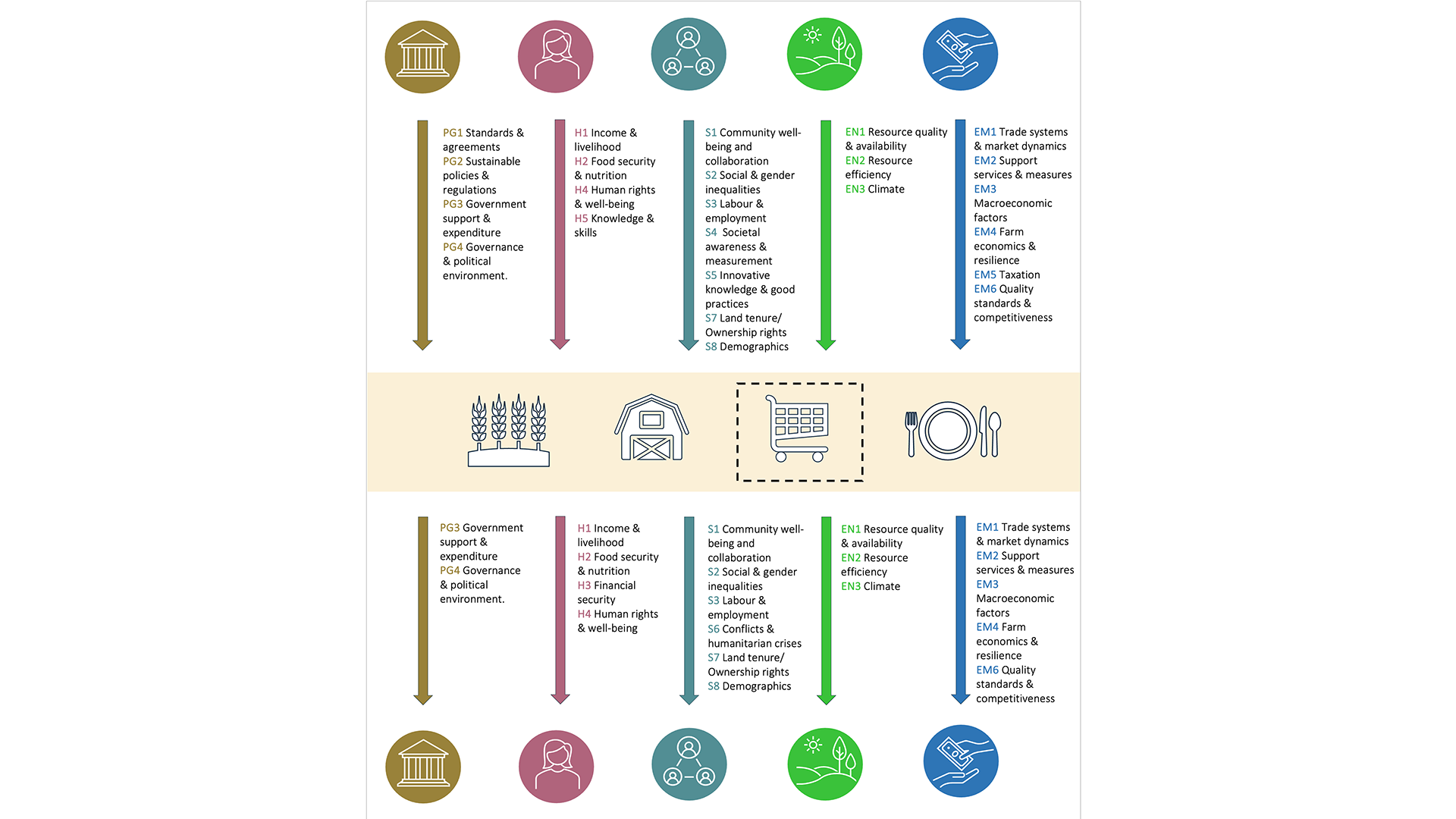

A core part of the MATS integrated multi-methods approach was to conduct 15 in-depth country, regional, and product (commodity) specific case studies. The aim was to provide local-level evidence and shed light on the intricate linkages between key elements in the food system, mainly focusing on African countries, but also covering Europe and Latin-America.

The MATS Agricultural Trade Systems Conceptual Framework (Fig. 2) illustrates these linkages and identifies how elements across political, human, social, environmental, and economic dimensions interrelate with agricultural trade regimes and policies.

Understanding this complex structure is pivotal for identifying leverage points to effectively address the key positive and negative impacts of trade on environmental sustainability and human well-being.

For example, a case study that examined linkages between Tunisian olive oil exports and water use showed that export trend has a high hidden economic, social, and environmental cost. Export and import oriented firms accumulate economic gains while traditional farmers and local consumers lose.

Furthermore, government policies favouring export-oriented large olive oil plantations have led to monoculture (that accounts for 80% of olive oil plantations), over-irrigation, and deterioration of soil, to mention a few drawbacks.

Another case study that concentrated on the alleviation of poverty among smallholder coffee farmers in Tanzania, found that unstable government policies on agriculture and co-operatives has decreased the effectiveness of the coffee value chain and the institutions governing the sector.

Fig. 1: MATS Agricultural Trade Systems Conceptual Framework

Small-scale farmers are the least privileged in the value chain, not competitive enough, have poor access to financial instruments, and are often excluded from the decision making. To uplift smallholder farmers, agricultural marketing co-operatives should be strengthened through capacity building in governance and market intelligence, their participation in the decision making should be fostered, and access to financial instruments guaranteed.

The importance of identifying leverage points

The joint analysis of the 15 case studies unveils key leverage points in three dimensions: Policy and regulatory frameworks, economy and markets, and social capital.

Regarding policy and regulatory frameworks, the findings suggest that participatory governance should be fostered by facilitating more collaborative and community-based work along the value chain, creating spaces for diverse stakeholders to engage in understanding issues (such as externalities or market power asymmetries), and collectively identifying potential solutions to inform policies and influence decision-making.

Additionally, policymakers should establish robust facilitation and resolution mechanisms between public and private institutions involved in global agri-food value chains for greater policy coherence and more effective implementation of policy interventions. To further improve policy coherence, it would be essential to ensure regulatory consistency across different sectors, aligning them with evolving political and socioeconomic context, and recognising the specificities of local context.

Transparency and accountability are foundational leverage points for enforcing regulations and promoting the adoption of voluntary sustainability standards and certifications. Without a clear understanding and support from local and global stakeholders, policies and projects may fail to contribute to establishing a system rooted in fair trade, socioeconomic justice, and ecological resilience.

The case studies underscore the delicate balance between prioritising competitiveness to meet the demands of global markets, and the need for strengthening resilience of domestic agrifood systems in terms of working towards food self-sufficiency through enhanced local markets. This balance is particularly vital in regions where a significant portion of the population faces food security challenges.

Within the dimension of economy and markets, access to finance for small- and medium-scale farmers was identified as essential for adopting sustainable production practices and enhancing competitiveness. Investments in infrastructure and technology were found to be key leverage points for adding value to farming products and reducing transportation and operational costs derived from a strong dependence on imported inputs.

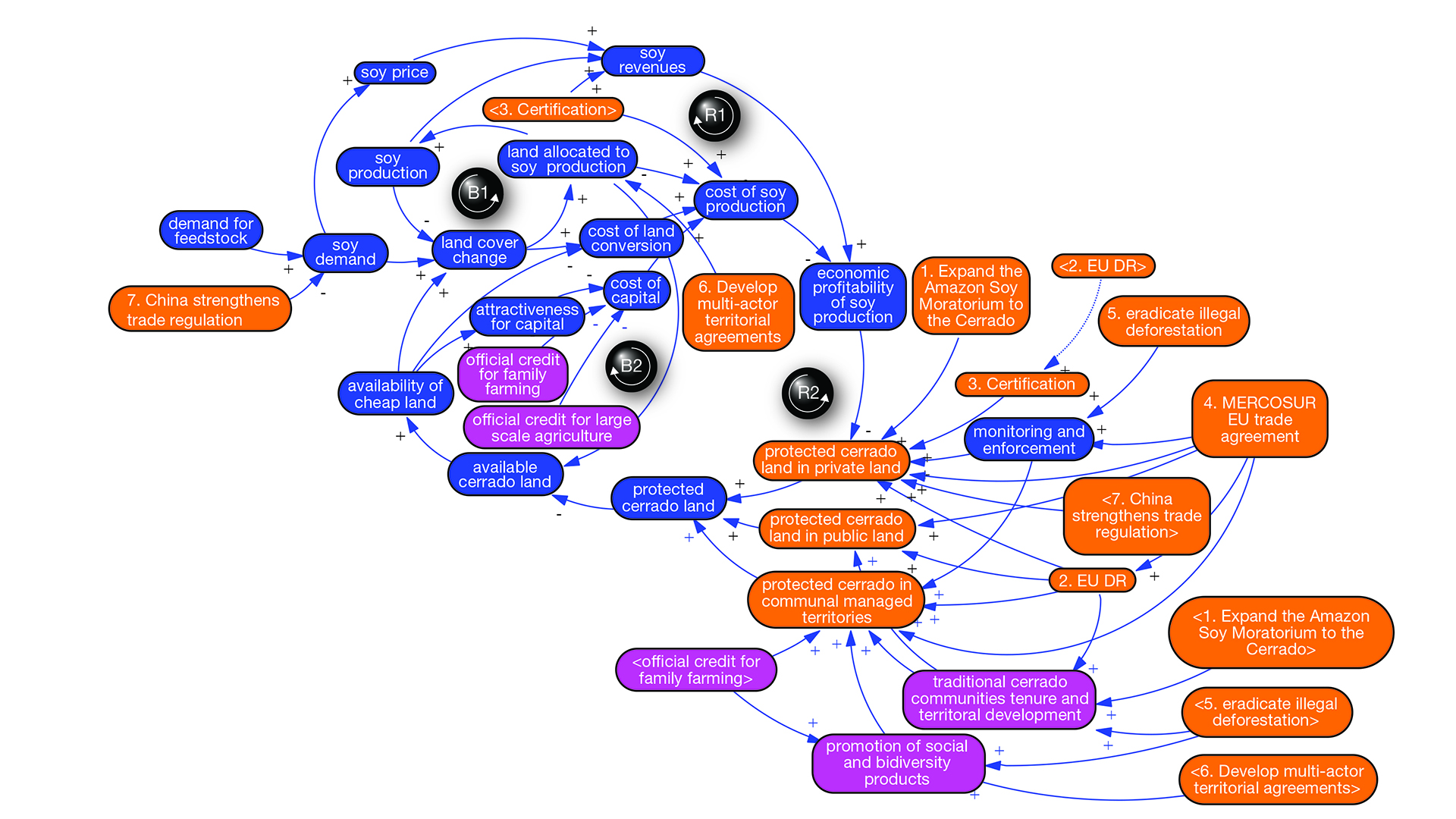

Fig. 2: Causal Loop Diagram developed in the case study on the Cerrado region in Brazil

Improving access to technology, especially for smallholder farmers, to enhance pricing transparency was identified as a potentially powerful lever to ensure fairer prices and address power imbalances.

Finally, within social capital, supporting associational membership, local partnerships, and collaborations along the global agri-food value chain were identified as key leverage points for strengthening inclusive decision-making and traditionally marginalised actors such as smallholder farmers.

Addressing the complexity of the global agri-food value chains

The second key part of the MATS multi-methods approach consisted of a modelling framework that combined three modelling approaches: A participatory qualitative systems approach (including the creation of system maps, or Causal Loop Diagrams (CLD), customised quantitative systems models (using System Dynamics coupled with spatially explicit models), and a global Computable General Equilibrium (CGE) model. To capture the complexity of global agri-food value chains, system dynamics were introduced into the framework as a method to fully integrate social, economic, and environmental indicators.

At its core, the food system embodies a dynamic web of relationships among various actors and elements such as environmental indicators, socioeconomic factors, and market dynamics. System dynamics provide a holistic framework to analyse how changes in one of these elements ripple through and affect others, thereby supporting the integration of detailed knowledge across each of the dimensions mentioned above.

The modelling framework was applied to seven of the 15 case studies. The impact of unsustainable production and case-study specific trade policies, as well as multidimensional gains emerging from improved sustainability were identified and quantified individually for each case study.

For example, Fig. 2 presents a Causal Loop Diagram (CLD) showing trade-related interrelations for a case study concentrating on the soy-meat complex in the Cerrado region in Brazil. It shows there are two key leverage points for improving social and environmental sustainability, first by supporting traditional communities and second by endorsing soy production that upholds social and environmental production standards.

The case study found that politically viable options to actualise these leverage points would be for example multi-actor territorial agreements and eradication of illegal deforestation through trade-related standards proposed by Chinese partners.

Another case study assessed social, economic, and environmental outcomes of milk production to illustrate the level playing field for trade across various countries. Several intervention options were identified to improve simultaneously the three sustainability dimensions. In terms of economic outcomes, the impact of farm size, milk productivity, and labour costs on the profitability of farm operations was considered. The environmental constraints covered, for example, manure management and GHG emissions.

The study found several solutions to achieve multi-dimensional sustainability and improved trade dynamics. For example, efforts to improve labour conditions turned out to level the playing field across regions on the social dimension, while reforestation, land restoration and the introduction of renewable energy for farm operations would help to reduce GHG emissions. To increase dairy farm revenues, offset higher labour costs, and decrease land use and expansion requirements, improved milk productivity turned out an important factor.

The power of economic valuation of externalities

The MATS modelling assessment confirmed that seamless integration of economic valuation into policy analysis that assigns a value to externalities, becomes a powerful tool for creating domestic incentives that encourage the adoption of sustainable practices with global impacts.

Economic incentives serve to motivate farmers and other value-chain businesses to transition towards sustainable practices, aligning environmental and social considerations with economic interests.

Similarly, the impacts of trade policies on domestic production should be assessed using such economic valuation of externalities, since the power of economic valuation of social and environmental impacts lies in its ability to uncover the hidden costs associated with unsustainable agriculture practices. Hence, it would be of high importance to integrate economic evaluation of environmental and social externalities in sustainability impact assessments of trade policies.

Regulatory frameworks need to connect local and global levels

To connect local level to global level, MATS addressed the interplay of domestic and international legal and regulatory frameworks and their connections to the above leverage points, focusing on labour and environmental standards, pricing mechanisms, and intellectual property.

Global agri-food value chain actors understand the need for transparency throughout the chain in a heterogenous manner, despite their awareness of binding formal rules.

Therefore, institutional frameworks that enable change throughout the value chain ought to promote both formal and informal collaboration and coherence in trade policies. Principles like risk-based regulations and revising outdated laws to streamline value chain processes were identified as part of valuable revisions of legal frameworks for supporting environmental and social sustainability.

Transition pathways towards more sustainable trade

The MATS project culminates in the creation of transition pathways towards more sustainable agricultural trade regimes based on the evidence gained from the 15 case studies and the modelling assessment.

At the heart of this process, a MATS vision for sustainable agricultural trade was created to arrive at a common understanding of the aims, timelines and activities needed for making agricultural trade more sustainable. A participatory visioning process helped to identify desirable future directions that was followed by the identification of concrete actions, leading to the accomplishment of different vision statements for the time horizon extending beyond 2035.

The formulation of transition pathways is still ongoing. However, the process so far reveals that both existing and new policies are needed for addressing all three dimensions of sustainability. Decentralisation of decision-making and reduced bureaucracy were identified as critical leverage points for guaranteeing smallholder farmers’ access to markets and fair prices.

Evaluating the impacts of agricultural trade policies

Up to date, the MATS project has revealed the importance of integrated evidence-based analysis. It extends beyond economic indicators, enabling the evaluation of the impacts of agricultural trade policies across a range of social, economic, and environmental sustainability indicators.

Furthermore, it confirms that the heterogeneity of location-context-product specific cases must be addressed when evaluating sustainability impacts of trade policy interventions, or the lack thereof.

The integrated multi-methods approach can help to identify the most effective interventions in global agri-food value chains to promote environmental and social stewardship while maintaining productivity and resilience.

Furthermore, researchers and policymakers can simulate different scenarios to anticipate potential outcomes and devise strategies to mitigate risks and harness opportunities, ensuring a more sustainable and resilient food system.

This article has presented an overview of the project’s work, yet research is still ongoing. The project is currently wrapping up the findings that will be processed into transition pathways, policy recommendations, scientific articles, and much more. As the MATS project will run until the end of the 2024, more outputs can be expected towards the end of the year. The project will organise a Sustainable Trade Policy Forum in Brussels (19-20 November, 2024) to showcase the final project outputs.

Please note, this article will also appear in the 18th edition of our quarterly publication.

Retein’s bioinspired filters improve resource extraction yields and cost-efficiency in battery recycling and mining.

The demand for lithium, critical for energy storage systems such as lithium-ion batteries, is projected to exceed supply by 2025.

Currently, lithium mining is predominantly conducted outside of Europe, in regions such as Chile, Australia, and China, intensifying Europe’s dependence on external sources.

Moreover, this reliance also constitutes geopolitical concerns for Europe since recycling the lithium already found in spent lithium-ion batteries is the only way to become somewhat lithium self-sufficient.

To address these challenges, the European Union has introduced stringent regulations under its new battery directive, mandating substantial recycling targets.

By 2025, 65% of lithium in batteries must be recycled within the EU, escalating to 80% by 2031. This regulation aims to decrease dependency on imported lithium and mitigate the environmental impacts of lithium mining by fostering circular resource handling.

Nature-inspired resource recovery filters

The push towards sustainability has spurred the development of advanced recycling technologies.

Traditional recycling methods often excel in recovering high-value materials like cobalt or copper from spent lithium-ion batteries while missing out on recovering satisfactory amounts of increasingly in-demand materials like lithium.

This increasing demand is driving the development of novel technologies to enable more efficient and selective recovery of lithium.

Moreover, novel technologies can also give more economically viable recycling methods than the ones currently on the market.

Retein develops industrial-grade filters that leverage nature’s outstanding precision and efficiency in recovering water-borne resources for reuse.

Inspired by cellular processes, these filters employ specific proteins capable of transporting targeted resources like lithium and water with high precision using minimal energy.

This method allows for both the selective recovery of lithium from spent batteries and the purification of water from industrial wastewater and process streams, significantly enhancing recycling efficiency and reducing environmental impact.

Retein’s technology works by incorporating proteins that transport the desired resource in a cell-like environment. Depending on the resource targeted, different proteins can be used to transport that resource specifically.

The cell-like structure is then stabilised into capsules to be more robust to external factors such as pressure and high concentrations. The stabilised capsules are incorporated into a polymer matrix to create a highly efficient filtering membrane. The incorporation of capsules into the polymer matrix provides a shortcut for the targeted resource through the otherwise densely packed membrane material.

How the filter works

The unique nature-inspired filter material is packaged into filtration modules of the standardised dimensions that are used across industries today. Retein’s filters are, therefore, well suited for use in existing installations without requiring major infrastructural changes while also catering to the needs of greenfield projects related to electrification.

The modular design of Retein’s solution allows for easy scaling to meet growing demand and adaptability to different operational sizes or lithium source types.

The enhanced flexibility with respect to source types allows for streamlined metal extraction and refining with minimal adaption to fluctuations in process water composition. This is due to the unique capabilities provided by nature’s finest resource recovery.

In comparison to commercially available filters, Retein offers filters that unlock new possibilities in recovering valuable water and resources from water mixtures.

The highly specific separation will allow for circular processing for economic and environmental benefits. The current state-of-the-art separation process uses one or, at best, two molecular characteristics to separate through.

In contrast, channel proteins have been tuned by nature to separate on no fewer than four characteristics: size, charge, hydrophobicity, and specific intermolecular interactions.

Retein’s filters, therefore, have the potential to provide outstanding performance when it comes to molecular precision recovery of lithium and other water-borne resources at minimum energy usage.

Minimising operational risks in battery recycling

Efforts toward efficient resource use are aligned with the targets within the United Nations’ Sustainable Development Goals (SDGs). Responsible water and energy management is increasingly viewed as a social and environmental license-to-operate issue, and increasingly stringent environmental regulations are being put in place.

Retein’s efforts in metal and water recovery are particularly geared towards improvements in SDG 6 (Clean Water and Sanitation) and SDG 7 (Affordable and Clean Energy).

By improving resource recovery yields and quality while reducing waste, Retein helps clients to increase their profits while simultaneously decreasing their risks through a solution that maximises yield while minimising negative impact, just like nature does.

This utilisation of resources that are already present inside the process also allow for battery recyclers and miners to capitalise on improved margins and a more cost-competitive offering towards their customers.

Retein is demonstrating improvements in lithium and water recovery yield and purity, as well as lowered operational cost and risks through pilot testing in multiple settings.

If you are an actor in battery recycling or mining who would like to know more about Retein’s offering and what synergies a partnership could present for you, do not hesitate to get in touch.

Please note, this article will also appear in the 18th edition of our quarterly publication.

Ocean Energy Europe aims to foster growth in the ocean energy sector through its annual conference and exhibition, which has been running for over ten years.

Ocean energy europe’s (OEE) mission is to create a supportive environment for the ocean energy industry to grow and thrive. Over 120 organisations, including Europe’s leading utilities, industrialists and research institutes, trust us to represent the interests of Europe’s ocean energy sector, making it the largest network of ocean energy professionals in the world.

We are working closely with our members and partners to support technological innovation, improve access to funding, and build a strong and resilient community. One of our main tools to achieve this goal is our annual Ocean Energy Europe Conference & Exhibition, which has been running for over ten years and is one of the most important events for the ocean energy sector.

Ocean Energy Europe Conference & Exhibition 2023: A successful ten-year celebration

The 2023 edition of the OEE annual event took place in the Hague on 25 and 26 October. It marked the ten year anniversary of the Ocean Energy Europe Conference & Exhibition and became one of the most successful OEE events to date.

The packed conference programme brought together high-level speakers from across the world and covered topics ranging from the latest developments of ocean energy’s flagship projects and innovative technologies to economic opportunities and funding. Anyone involved in the ocean energy sector could learn something new and gain insight into the direction the sector was taking.

On the exhibition side, we introduced new and improved fully branded stands made from reusable and recyclable materials. This gave the entire event a fresh and modern look, guaranteeing that our exhibitors look their best while staying true to our sustainability values. Our exhibition is the place to meet, connect, raise your profile and do business, and the 2023 edition was no exception.

Over a third of our attendees are C-suite executives, being visible on the OEE exhibition floor means being visible to the people who are building the ocean energy sector. In 2023, ocean energy attracted an unprecedented level of attention from big industrial and energy players, and it was reflected at our event with a lot of new faces and new deals being signed.

To facilitate this process, the OEE2023 Conference & Exhibition also included a new online networking platform. Attendees were prompted to set up an online profile, find potential partners, clients and investors, and book meetings with them in advance. Over 100 B2B meetings between leaders of the ocean energy industry took place thanks to this new feature.

Finally, and for the first time ever, the 2023 OEE Conference & Exhibition included free activities for the general public. Our members brought their ocean energy devices, real machines which have been tested in real sea conditions, to a public square in the Hague next to the conference venue. In addition, we organised an ocean energy photo exhibition in a public part of the venue to show ocean energy devices in the water and explain how the different technologies work.

Ocean Energy Europe Conference & Exhibition 2024: Back to the home of ocean energy

This year’s edition, dubbed OEE2024, will take place on 5 and 6 November in Aviemore, Scotland. The choice of venue is never arbitrary: This year, the conference returns to Scotland, going to the Scottish Highlands. Scotland and its Highlands & Islands have long been at the forefront of ocean energy. Home to some of the world’s most important ocean energy resources and some of the most successful ocean energy technologies, it is the perfect location for the sector to come together for OEE2024.

We are delighted to be able to host such a large international event in the heart of Scotland. The OEE annual conference boasts attendees from all over the world, with 30 countries from 6 continents represented at the 2023 edition. The 2024 conference programme will capitalise on Scotland’s ocean energy leadership and the sector’s quick growth towards large-scale array deployments to focus on industrialisation and how we can build strong supply chains.

Speakers have previously included national Ministers and European Commissioners, as well as CEOs, CFOs, decision-makers, and stakeholders from all corners of the ocean energy sector: developers, supply chain, investors and national and regional governments, to name a few.

This year’s exhibition already promises to be memorable. Stand sales opened in late April, and several of the lead ocean energy technology developers have already booked their spots. In addition to our high-level exhibitors, OEE members will once again bring their devices to the exhibition as part of our ocean energy Tech Trail. To date, four full-scale pieces of ocean energy technology have been confirmed, with more to come in the next few months.

The official programme of the conference will be published in May, along with the registration opening. Registrants will be able to access the online event platform, start networking and book meetings with other attendees. We will also announce several side activities that will take place before, during and after the event itself. We’re keeping the surprise for now, but these will let attendees go more in depth into specific topics, meet their peers in a more relaxed setting or discover the Highlands and make the most of their time in Scotland.

Please note, this article will also appear in the 18th edition of our quarterly publication.

An old cryolite mine and an untapped rare earth endowment hold unique importance for greater powers than its junior Australian owner.

A chasm of an open pit resting on the banks of the fjords of the Labrador Sea looked more the part of a biblical disaster than a mine.

However, the Greenlanders of the twin settlements of ‘Green Valley’ Kangilínguit and Grønnedal didn’t build their townships around a cataclysm, but Ivigtût, a massive and singular known naturally occurring source of cryolite.

Greenland’s historical mining importance

Ivigtût was mined for a century and a half before the shutters came down in 1987, and the pit was drowned with water. The story of what is now Ivittuut is not over, as there, within eyesight amid the melting snow, lies a mineral endowment holding strategic importance for greater powers than its Australian owner.

The semi-autonomous nation of Greenland has long had a unique global value. Long before the ambitious Donald Trump announced intentions for the US to buy Greenland off Denmark in 2019, then-US president Harry Truman proposed its purchase as a geographical defence against Soviet bombers. During Truman’s 1945-53 leadership, the area now known as Kangilinnguit had been in US hands, with the US military protecting its prized cryolite quarry area during World War II. Later, the US handed back the area dubbed Green Valley to the Danish in 1951.

Greenland is of different importance in modern times. As the ice melts and lucrative sailing routes open, untapped resources have again captured the attention of major geopolitical powers. China views Greenland as an entry point into the Arctic, the United States as its northernmost military presence, and both as potentially massive sources of rare earth elements.

Eclipse Metals views a slice of Greenland as its own after looking north in 2021 and seeing a well-studied but neglected pair of assets at Ivittuut and the company’s Grønnedal Rare Earth Project.

The Executive Chairman of Eclipse, Carl Popal, discussed the importance of the project and Greenland’s potential in the critical minerals market. He said: “The project was a good deal, with a lot of untapped potential, which needed to come to the surface and be rejuvenated. These historical facts and figures warrant exploration. While this pursuit is scientific in nature, it does not preclude the discovery of geological veins of prosperity.”

A scratch through the surface of the Grønnedal project, which became Eclipse’s maiden resource, proved its acquisition had more than the benefit of location.

A 1.18 million tonne resource grading 6859 parts per million (ppm) total rare earth oxide came from the surface of Grønnedal to a shoveler’s depth of 9.5m. All mineralised holes ended in high-grade rare earth, and the resource remains open wherever you look while representing a small fraction of what is a largely untested carbonatite intrusive.

Popal notes it has all the signatures of being among, if not the largest, rare earth deposit in Europe. He said: “The geophysical results suggest the potential depth of up to 500m, yet we haven’t drilled to such an extent. The resource within the single lens is about 80,000 tonnes per vertical metre, there are more lenses within the carbonatite footprint which we haven’t even touched yet.”

The raw size has yet to be fully encapsulated by the JORC code mineral resource estimate, and while rare earth deposits can be complicated, multiply the 2200 tonnes of contained neodymium in the current resource alone by its selling price to see a value roughly five times Eclipse’s current market cap on the Australian stock market.

Eclipse’s helmsman tips they could pump those numbers up pretty easily if they wanted to. Popal noted: “People are actually considering drill results of 500-600 to 1000 ppm to be promising. Here at Grønnedal Hills, we are calculating our resource with a cutoff of 2000 ppm in just the small area we have explored within the carbonatite footprint!”

It’s even more exciting, considering this is just the Grønnedal project. An old cryolite mine and its unique geology give a sense of how incredible this area’s scale and potential are.

Describing this cryolite mine, Popal explained: “It was formed like a big cannon firing from the centre of the earth, in a pipe-like structure, and it shot out a whole pile of minerals like a club sandwich. The mine, with over 130 years of history, was active from the late 1800s to the late 1980s. It was first mined for lead and silver, then for the rare mineral cryolite. Some cryolite still exists there within the pit environment. Below that was silica, zinc, and quartz, not what they were after historically, and so it was just left behind without even assaying the core!”

With the company now having access to the 19,000m of cores, Eclipse has this resource to tap and is planning to soon take a proper look at the partially mined marvel at Ivittuut. On the subject, Popal says: “We’re assessing the core further, and throughout the summer, we’ll be having an extensive programme trying to understand below within the pit to see what’s going on.”

There is a lot of value within the pit environment, with the real prize likely to be high-purity silica, a presumably common but strikingly finite resource whose demand for high-purity products is soaring due to modern technology.

Lower-end products are ubiquitous in the glass and concrete that are used to build our cities. Despite the market shortage of high-purity silica quartz, Popal highlights the challenges in identifying suitable end-use products for chip manufacturing, solar and other applications. He said: “If we really look at the tech industry, high-purity silica is as critical as anything, and demand is growing massively for semi-conductors and silica wafers.”

China is conducting extensive sea dredging in search of high-purity silica quartz but it is encountering challenges. The pit first needs to be dewatered for Eclipse to take its own look at depth, but the company won’t be delving into the bottom without a plan in place. As Popal said: “Following a process is part and parcel of developing a big project. The plan is to make sure all our permits are in place to have access to the bottom and open for offtake.”

Seizing the opportunity

Because of all the fascination with geopolitics surrounding Greenland and its untouched trove of commodities, Eclipse has a job to do in finding them.

Popal concludes: “We’re putting our hands together to develop this, but we’re a small company and understand that there’s an opportunity here. We will act in the best interests of our shareholders, and per the saying ‘first in, best dressed’, better quality will be available to those who seize this opportunity first. The potential in Greenland is massive, and the world knows that, but if people are going to procrastinate, it will be their loss.”

Written by Jack Baker, Market Open

Please note, this article will also appear in the 18th edition of our quarterly publication.

Nadim Chaudhry, CEO of World Hydrogen Leaders, examines the opportunities for CCUS-enabled low-carbon hydrogen and how US policy is accelerating the advancement of this vital fuel of the future.

While its relevance in helping to reach climate goals has long been recognised, deployment of carbon capture, utilisation and storage (CCUS) has been slow and consistently accounting for less than 0.5% of global investment in clean energy technologies.

Although CCUS is not a new technology, and there are currently around 41 operational facilities globally, it has typically been deployed at a small scale – mainly for R&D projects and for enhanced oil recovery.¹ In order for CCUS to meaningfully contribute to climate change goals, the amount of CO2 captured would need to grow four-fold from current levels by 2030.² However, stronger climate targets and investment incentives are now starting to drive increased momentum into CCUS – and one of the key strategies to provide a boost to the technology is the efficient production of hydrogen.

The role of CCUS in low-carbon hydrogen production

Hydrogen is a versatile energy carrier that can help support the decarbonisation of a range of hard-to-abate sectors where electrification from renewable sources cannot deliver the level of energy output required. These include iron, steel, chemicals and cement production, as well as hydrogen-based fuels for aviation, shipping, and long-distance haulage.

CCUS can facilitate the production of low-carbon hydrogen (sometimes referred to as ‘blue’ hydrogen) from natural gas and provide an opportunity to bring it into new markets in the near term – and at a reasonable cost.

It can help alleviate pressure on already constrained electricity grids, allowing renewable electricity generation and electrolytic hydrogen production to scale at a more manageable pace. This benefit of CCUS-enabled hydrogen over the next decade has been recognised in the Committee on Climate Change’s recently published 2023 Progress Report to Parliament.

Today, the cost of CCUS-enabled hydrogen production is likely to be around 50% of hydrogen production via electrolysis powered by renewables-based electricity. While the cost of electrolytic hydrogen is anticipated to reduce over time with the onset of increasingly cheaper electrolysers and renewable electricity, CCUS-equipped hydrogen will most likely remain a competitive option across regions typically associated with low-cost fossil fuels.

Recently there has been a significant increase in the appetite to develop CCUS projects, with a 50% increase in CO2 capture in the 12 months between 2022 to 2023.³ This has been driven by governments internationally coming under increasing pressure to meet global climate targets, implementing robust legislation and providing clear pricing signals in order to make CCUS commercially viable.

Despite this positive news, there remain three significant issues. Of the many announced CCUS projects, only around 5% have taken firm investment decisions due to the uncertainty of demand, a lack of clarity around certification and regulation – and, critically – the lack of infrastructure available to actually deliver the hydrogen to customer sites. And according to the IEA, to help deliver a majorly decarbonised heavy industry by 2030, a third of all hydrogen production will need to be dedicated to those hard-to-abate sectors. Currently, these applications only account for around 0.1% today, meaning there is considerably more work to do.

Challenges with deploying CCUS at scale

Because CCUS is far from a mature industry, a single stakeholder is typically unable to take on all the expertise, risk and capital expenditure needed across the whole value chain. As such, the most significant challenges with deploying CCUS at scale are the multiple different, distinct stakeholders that need to be co-ordinated, including the industrial plants that are the CO2 emitters themselves, the various CCUS technology suppliers which separate and capture the CO2, providers of processing, compression solutions, transportation solutions and, finally, experienced storage providers who can inject and store the CO2 underground.

It is evident that urgent policy action is needed to create demand for low-carbon hydrogen and unlock the necessary investment to accelerate the scale-up of production and the building of delivery infrastructure.

The US leading the way

Currently, different policy approaches are being undertaken by governments to encourage the deployment of CCUS at scale. In particular, the United States has provided a much-needed shot in the arm for the infrastructure required to scale up technologies. Incentives under the Inflation Reduction Act (IRA) provide project developers with a $50 per metric tonne of CO2 tax reduction where CO2 is stored in dedicated storage sites. The Infrastructure Investment and Jobs Act passed in November 2021 also provided a combined $15bn to support CCUS and low-carbon hydrogen production.

The IRA has had a considerable positive impact on hydrogen production, enabling the US to have the largest hydrogen project pipeline of any country. It currently accounts for 18% of the total announced capacity, putting Australia in second place at 14%. And while the percentage of hydrogen projects in the EU surpasses both of those (at 29%), it should be remembered that this figure accounts for the whole of the EU (consisting of 27 countries) and the UK, which ultimately results in relatively minor pipelines per country.